WTI Crude Oil Price Plunge

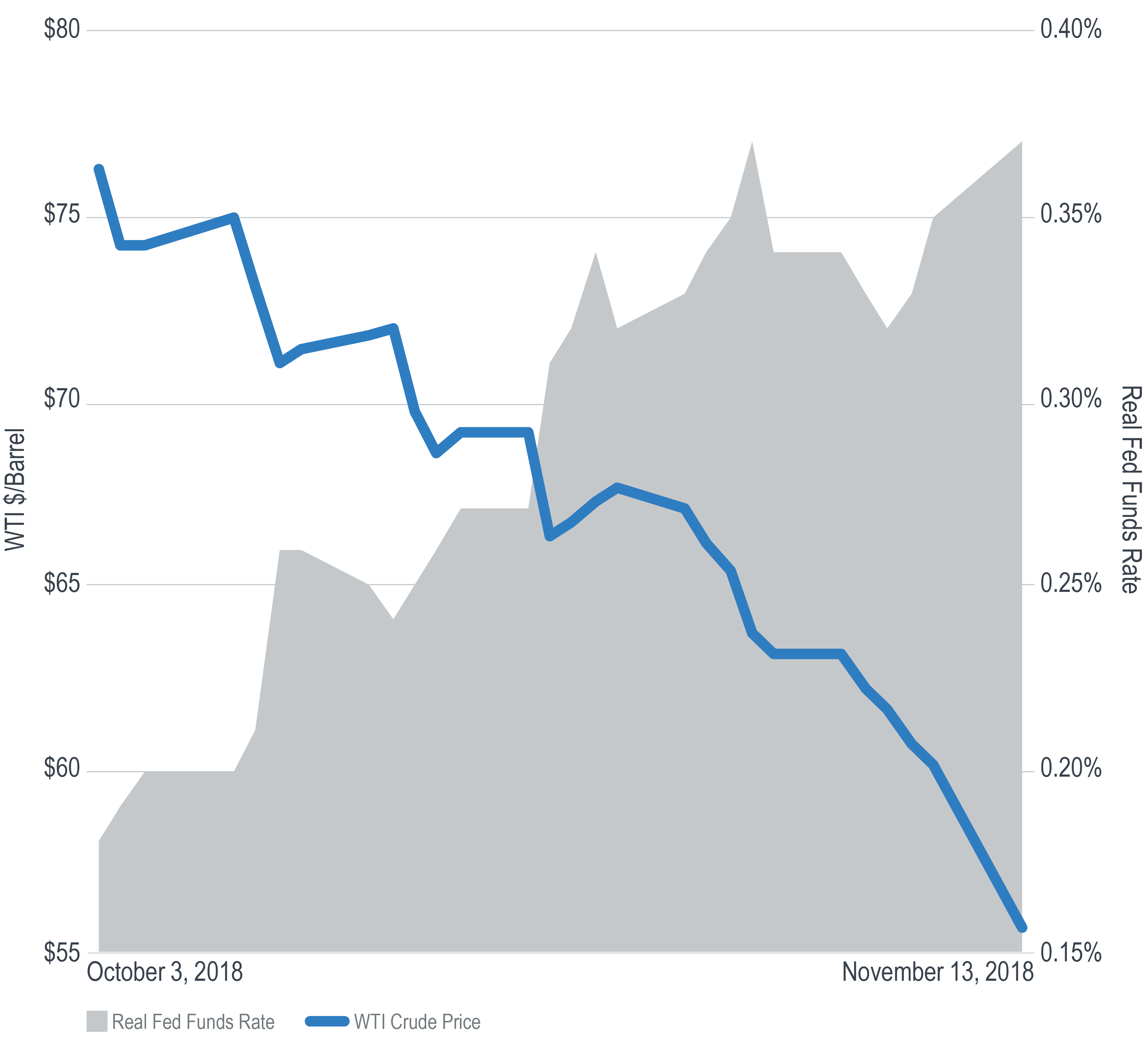

From its 2018 peak on October 3 to November 13, the price of a barrel of West Texas Intermediate crude oil fell by 27%. In the later stage of its decline, it closed at a lower price for 12 consecutive days, something it’s not done in at least 35 years.

This of course has significant first order implications for the energy industry and for the economy at large. Perhaps less intuitive, however, is the effect that a falling oil price may have on Fed policy.

As the price of oil has fallen, so too have inflation expectations. Over last six weeks, the 5-year breakeven inflation rate has fallen from 2.07% to 1.88%. Regressing the breakeven rate against the price of oil from the beginning of 2009 through November 13 generates this relationship:

5yr BE = 0.932+0.01*WTI, with an R square of nearly 40%.

This has had the effect of pushing one measure of the real fed funds rate (fed funds rate minus 5-year breakeven rate) up to its highest level since January 2009.

While the market’s expectation of a December rate hike remains largely unchanged, its outlook on subsequent hikes in 2019 has become less clear. If oil continues to fall, and inflation expectations with it, the Fed’s efforts to normalize policy may involve an earlier-than-expected intermission.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.

© Milliman FRM