Summary: Disruption from trade disputes, rising interest rates, uneven signals from housing and automotive markets, nascent inflation from a tight labor market, concerns about “peak” employment and lapping tax reform (at some point) next year have all served to create fear that the U.S. economic growth will slow and possibly enter recession perhaps in late 2019 or early 2020. Considered an infallible signal of impending recession, the yield curve (explained below) partially inverted last week as well. On the other hand, current conditions couldn’t be better and many company management teams, economists and investors see little reason for worry. Our view is that investments in high quality companies with resilient business models and trading at attractive valuations can be done at any point in the economic cycle, assuming a sufficiently long investment time horizon. We discuss an investment in CarMax (KMX) in this month’s newsletter.

What the Heck is an “Inverted Yield Curve”: An Explanation in Plain Language

In case you need to sound like you know what this means at your next cocktail party: (May we also suggest that if you are discussing yield curves at cocktail parties you should perhaps consider a different group of friends). Anyway, in the simplest possible terms, these are the three points you need to know: First: An inverted yield curve has correctly forecasted (preceded) every recession over the past 60 years, only once issuing a false warning (after which it was followed by an economic slowdown rather than an official recession). This explains why people care and pay attention. Second: An inverted yield curve is a sentiment indicator not an economic measurement. In other words, it reflects how investors feel about the future rather than actual economic activity, e.g. industrial production or consumer spending. For this reason, I will suggest Third: an inverted yield curve could still be wrong about the future, despite its strong track record.

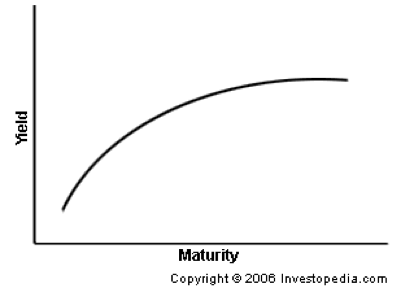

A yield curve is just a graph: It’s a plot of U.S. government obligation (called bills, notes and bonds) yields (interest payments plus discount to maturity) on the Y axis against the duration of the bonds on the X axis. If you have a mortgage or a loan of any kind you can understand this. Basically, the longer the borrowing period, the higher the interest rate and normally the total yield. You will earn less investing in 2-year Treasury bills (normally) than a 30-year Treasury bond just like you pay a higher interest rate for a 30-year mortgage than a 10-year loan on your fancy vacation house. When we graph this relationship (yield against duration) we get this nice curve as seen in the below figure:

An “inverted” yield curve is – you got it – when the graph is going the wrong way and shorter-term U.S. obligations are generating a higher yield than long-dated bonds. How does this happen? It is a function of supply and demand in the bond market. When investors get scared about the near-term future (the next few years), they sell equities (making the stock market go down) and short-term U.S. Treasury bills (because they are worried about near-term interest rates and reinvesting the proceeds of bills as they mature) and buy long-term bonds. This makes long-term bond prices rise while short term bonds fall (with equities). Consequently, the yields get all confuzzled (as my 16-year old daughter would say, if she were to start talking about bond yields) and short-term debt yields more than the longer-term Treasuries and bonds, i.e. inversion. (I won’t include a neat graph of the inverted yield curve, I think you can imagine it yourself.)

The bottom-line: when the yield curve inverts (as it did briefly last week), you should understand that a lot of institutionally-managed money is being positioning for less attractive financial conditions (or a recession) in the coming few years. This signal was the primary factory behind the market tanking 800 points on Tuesday.

How We are Managing Our and Client Money:

Our assumption is that our ability to forecast the overall market and macroeconomic conditions is highly limited. Accordingly, while we try to understand current conditions and trends, we try to make investment selections based on a long-term view and look for companies we can own throughout the economic cycle.

Selection from our model portfolio: Our approach is to own high-quality companies, bought opportunistically, and hold them long-term with the intention to minimize trading costs and taxes. Our portfolio is concentrated (~20 positions) and generally we are favorably inclined towards companies we know or at least find easy to understand.

CarMax (KMX): CarMax is the largest retailer of used cars in the United States and currently operates about 200 large-format used car Superstores. We have followed KMX’s growth for more than 15 years and consider ourselves very familiar with the company. If you know don’t KMX, its core guiding principal is to legitimize the used car business by building transparency into all parts of the used car trade-in, buying and financing process.

Used cars are a huge market but also a very challenging asset class to manage. Consider that every vehicle is unique as each has a different combination of age, miles driven, and maintenance records. Further, used cars lose value just by sitting around on the lot, sometimes at an alarming rate. Lastly, there is no vendor for used cars. Inventory can’t simply be ordered up on a schedule or returned if it doesn’t sell. To address these challenges, KMX has developed sophisticated systems to understand the value of each car it acquires (either from people just driving up and selling their cars to the company at its stores or purchased at a used-car auction, I bet you want to attend one of those), how to compose its assortment on the lot (into a balance of brands, price, and other factors), and when to reduce prices to sell inventory more quickly. At the store level, KMX turns its inventory ~10x per year, which means that it sells through its entire stock roughly every two months, which is amazing, in my opinion. For this reason, we like to think of KMX as a technology company masquerading as a used car retailer. Recently, the market has become concerned about two potential existential threats to KMX: 1) a world of self-driving cars where theoretically no one will own vehicles anymore and 2) a few start-up companies that “deliver” cars to your driveway (I won’t say “door”) potentially disrupting the model of shopping in a store.

Last week, KMX announced its response to (2) by launching its own delivery service, which will first be tested in the Atlanta market and then rolled out nationwide. This initiative will allow consumers to do all or some of the used car purchasing process at home or in the office (cause that’s what you’re doing at work) depending on the consumer’s comfort level. In some ways, this represents KMX disrupting its own retail model. It is utilizing technology to bring a different and possibly better experience to the consumer in the used-car category. Simulateously, KMX is outflanking both the start-ups with similar but less attractive offers (the existing delivery-model start-ups currently require a car to be fully purchased before it is delivered while KMX will bring it around to your place simply for a test spin) as well as smaller dealers which we believe will find it very difficult to develop similar capabilities.

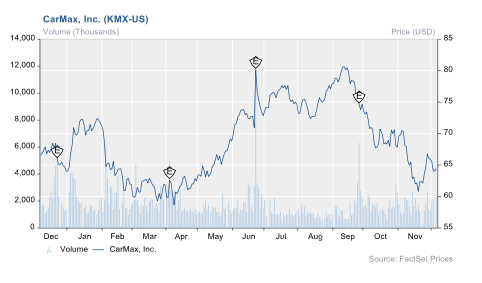

KMX is scheduled to report earnings for its November quarter shortly. We’re not expecting a great quarter but we believe that over time, KMX will continue to take share in what is a massive market (used car sales) and create tremendous value for shareholders. See 1-year price chart below.

Yours,

John Zolidis

President & Founder

Quo Vadis Capital, Inc.

© Quo Vadis Capital

General Disclosures:

Quo Vadis Capital, Inc. (“Quo Vadis”) is an independent research provider offering research and consulting services. The research products are for institutional investors only.

The price target, if any, contained in this report represents the analyst’s application of a formula to certain metrics derived from actual and estimated future performance of the company. Analysts may use various formulas tailored to the facts and circumstances surrounding a specific company to arrive at the price target. Various risk factors may impede the company’s securities from achieving the analyst’s price target, such as an unfavorable macroeconomic environment, a failure of the company to perform as expected, the departure of key personnel or other events or circumstances that cannot be reasonably anticipated at the time the price target is calculated. Quo Vadis may change the price target on this company without notice. Additional information on the securities mentioned in this report is available upon request. This report is based on data obtained from sources Quo Vadis believes to be reliable; however, Quo Vadis does not guarantee its accuracy and does not purport to be complete. Opinion is as of the date of the report unless labeled otherwise and is subject to change without notice. Updates may be provided based on developments and events and as otherwise appropriate. Updates may be restricted based on regulatory requirements or other considerations. Consequently, there should be no assumption that updates will be made. Quo Vadis disclaims any warranty of any kind, whether express or implied, as to any matter whatsoever relating to this research report and any analysis, discussion or trade ideas contained herein. This research report is provided on an "as is" basis for use at your own risk, and neither Quo Vadis nor its affiliates are liable for any damages or injury resulting from use of this information. This report should not be construed as advice designed to meet the particular investment needs of any investor or as an offer or solicitation to buy or sell the securities or financial instruments mentioned herein. This report is provided for information purposes only and does not represent an offer or solicitation in any jurisdiction where such offer would be prohibited. Commentary regarding the future direction of financial markets is illustrative and is not intended to predict actual results, which may differ substantially from the opinions expressed herein. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur.

The analyst who is the author of this report has a long position in CarMax (KMX). Quo Vadis prohibits analysts from trading in a way that is inconsistent with opinions expressed in reports [subject to exceptions for unanticipated significant changes in the personal financial circumstances of the analyst].

This report may not be reproduced in part or in whole. Please do not redistribute this report.

SEC Reg AC Certification:

All of the views expressed in this research report accurately reflect the research analyst's personal views about any and all of the subject securities or issuers. No part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by the research analyst in the subject company of this research report.

Read more commentaries by Quo Vadis Capital