Executive Summary

Ten years into a bull market, the conventional wisdom is that U.S. stocks are richly valued based on most well-cited metrics. Fortunately, solid investment opportunities remain in places that some value investors may find surprising. This is why the GMO Quality Strategy remains fully invested in equities. We invest globally, yet the portfolio holds primarily U.S. domiciled companies. Nearly half of the portfolio is invested in technology stocks. And rather than invest in beaten up value stocks, the portfolio trades at an aggregate P/E in line with the S&P 500. But price is not value. We believe these securities, selected through a fundamental bottom-up process that focuses on quality companies, are valued to deliver solid returns with below market levels of risk.

Introduction

GMO’s reputation in the investment world is as a value investor that identifies and avoids asset bubbles. Given the current environment, we asked ourselves: what do most of our clients and other investors assume that GMO thinks about markets? That list would likely look something like this:

■ Equities are bad

■ U.S. equities are the worst

■ FAANG stocks are in a bubble

■ “Value” is the virtuous way to invest

■ The best investment approach is quantitative and top-down

If this is your perception of GMO then our Quality Strategy may surprise you. This is a benchmark agnostic equity strategy that invests globally, but holds more than 80% of assets in U.S.-domiciled companies. From a sector perspective, nearly half (45%) of the portfolio is in technology names,1 including positions in three of the five FAANG stocks. While we are very careful to not overpay for a stock, we do not manage according to traditional “value” metrics and our portfolio trades at a premium, albeit a modest one, of a P/E of 18.2 relative to 17.2 times for the S&P 500. This positioning is a result of our security selection process, which is decidedly bottom-up and fundamental.

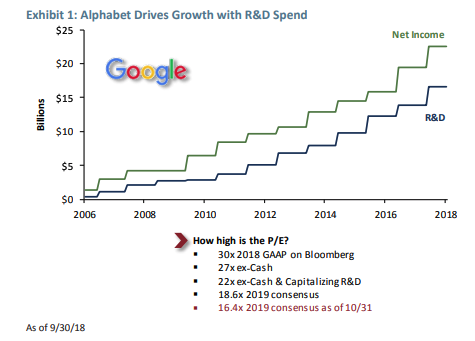

An Illustrative Example: Alphabet

Let’s consider the U.S. FAANG stock Alphabet, which is the largest holding in our portfolio. While Alphabet may trade at a superficially high P/E, we believe its valuation is justified based on a more appropriate analysis of its fundamentals. Specifically, we looked at how Alphabet invests in R&D and how that translates into higher future revenues, thereby growing market share and continued relevance. From an accounting point of view, however, today’s R&D is taken out of today’s earnings as an immediate expense, whereas in reality current earnings are driven by the R&D of several years ago. Taking an alternate accounting approach of capitalizing R&D and amortizing the expense over time (as is standard with tangible assets) paints a more accurate picture of Alphabet’s true valuation, in which current earnings power is significantly higher. Taken in combination with the company’s high cash level and strong growth prospects, we find that the market is affording the opportunity to invest in a high quality growth stock trading at attractive multiples. These multiples are made even more attractive after recent market turbulence. Exhibit 1 shows the magnitude of the R&D effect and the series of adjustments we made in thinking about Alphabet’s P/E ratio.

Our Return Forecast for Quality Equities

As of 11/30/18, the S&P 500 was trading at 20.9 times trailing earnings, compared to an average multiple of 15.7 dating back to 1880.2 In an expensive market, quality companies typically trade at higher P/E’s than most “value” investors would like. The key, however, is to choose companies with resilient margins and strong business results that justify their current valuations.

At today’s prices, we believe that our buy-and-hold portfolio of quality equities can generate a return in the order of 5% above inflation based on our discounted cash flow analysis. Additional return opportunities will present themselves when market volatility allows us to rebalance into the most attractive names at cheaper prices. While return expectations are driven from the bottom up, we hold a portfolio that we believe in aggregate provides the following:

■ Forward earnings yield of 5.5%

■ 3.3% projected real revenue growth through 2023

■ High return on marginal invested capital

■ Stable margins

At 3.3%, our revenue growth projections are conservative and well below consensus expectations. Because our investments focus on companies with high return on capital, there is minimal required reinvestment. Hence, we see a high conversion of the earnings to free cash flow augmented by that growth. While all companies experience some degree of profitability erosion over time, we believe these quality companies are well positioned to withstand this erosion given that their margins are sustainable further into the future than the rest of the market.

Those familiar with the GMO 7-Year Asset Class Forecasts will notice that our return expectations for quality companies are significantly more bullish than is our Asset Allocation perspective on broader groups of U.S. equities. We see no contradiction that a carefully constructed subset of 40 stocks can have a better outlook than the overall market. We believe that 5% real is a fair return for high quality stocks (so no multiple compression needs be forecast over the long run) and that profit margins are sustainable for the companies that we own. Those are both counter to the seven-year forecast for the broad market.

Why the Portfolio is Mostly U.S. Domiciled

Our allocation to U.S. stocks is driven by fundamental analysis. While at the aggregate index level the S&P 500 may be richly valued relative to non-U.S. stocks, this comparison breaks down when one looks at individual high quality names in similar businesses. United Technologies, Honeywell and 3M, for example, are all U.S. industrial companies in our Quality portfolio, and they all trade at a P/E discount to high quality European peers like Assa Abloy, Atlas Copco, Schindler and Kone. McDonald’s Japan trades at a material premium to McDonalds, and Walmart de Mexico is trading at more than twice the multiple of Walmart. This is consistent with our intuition that, perhaps due to scarcity value, quality companies are a more crowded trade outside the U.S. than within.

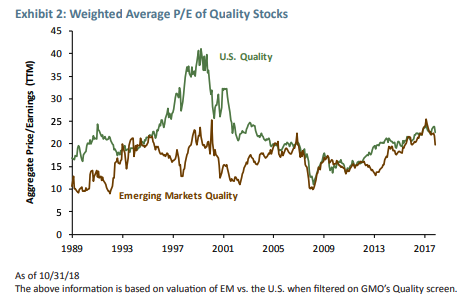

While GMO generally sees opportunity in emerging markets, we find that valuations in the U.S. and emerging markets stocks have converged when we filter the indices through our quality screen. Exhibit 2 shows that while in the past emerging markets quality stocks have been discounted, this has not been the case over recent years.

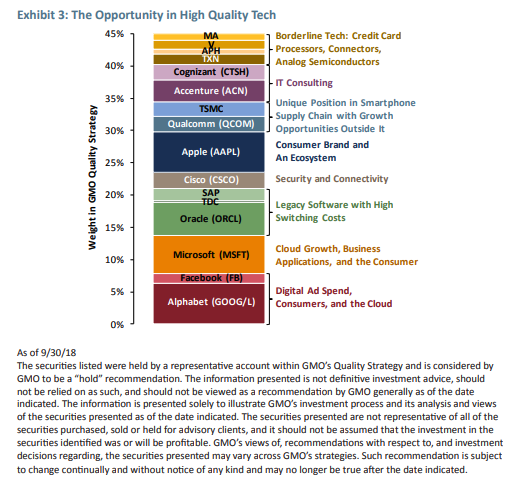

A Large Technology Position We continue to see the best individual stock opportunities in the broader technology sector. Technology boasts a disproportionate representation of businesses with the widest moats and best ability to grow at a high return on investment. Meanwhile, valuations for the technology companies where we are invested remain reasonable.

Our technology allocation is driven by bottom up stock selection. This begs the question of whether that aggregate exposure is too concentrated. We believe not! These are a very diverse set of businesses. Analysis of our positioning (see exhibit 3) shows allocations across fundamentally unrelated subsectors of technology, including: digital advertising, enterprise software, the smart phone supply chain, IT consulting, and stocks that straddle the border with other sectors (e.g., credit card processors, connectors and analog semiconductors). This point is also supported by the recent S&P industry reclassification of Alphabet and Facebook into the Communications Sector (although one suspects they will trade more like Microsoft than like AT&T and Verizon).

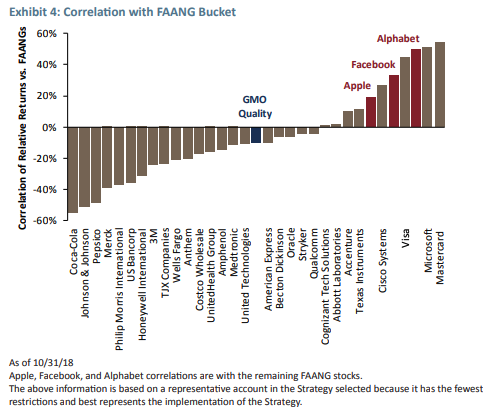

Of further importance is that a technology-heavy portfolio can still be defensive if it is comprised of the right companies that meet our quality standards and trade at reasonable valuations. Even during the FAANG stock correction, the GMO Quality basket was able to perform well and exhibit negative correlation to the performance of the FAANG stocks (see exhibit 4). Defensive names in the portfolio provide a conservative ballast. But it is equally important that many Quality Tech names are fundamentally different from, and less volatile than, the FAANGs.

Bottom-Up and Fundamental

A high conviction Quality strategy requires forward-looking, bottom-up, fundamental analysis to drive security selection. We maintain a laser focus on finding companies with durable, resilient business models and high return on capital. Our portfolio companies offer long-term secular growth, and we believe they will maintain relevance in the economy, no matter what unforeseeable changes emerge.

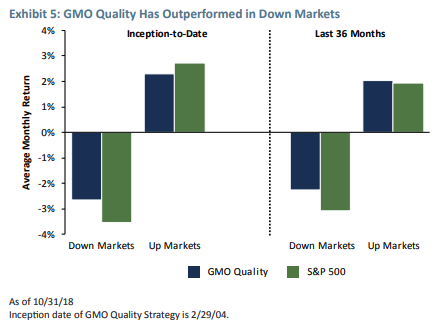

We manage risk by investing in a diverse set of high quality businesses. While shorter term performance is never certain nor is it our focus, we do expect to experience a lower level of volatility than the overall market. The strategy has outperformed during bear months, not just over its entire history, but also over the more recent period where we have invested more in growth stocks including the technology sector. That latter point, shown in Exhibit 5, is consistent with our view that quality characteristics at the right price are defensive wherever one may find them.

Conclusion

Even when markets appear expensive – as many do now – it is possible to invest responsibly in equities if you have a strong stock selection process. Active stock picking, declared dead over and over during the formative years of the bull market, can make its virtues known in times like these. In particular, we believe the Quality style is the most prudent approach for investing in U.S. equities. It presents the opportunity to generate fair equity returns while providing the confidence to sleep well at night and to hold on during those inevitable periods where markets decline and greed turns to fear.

Tom Hancock. Dr. Hancock is the head of GMO’s Focused Equity team and the portfolio manager for the Quality Strategy. Previously at GMO, he was co-head of the Global Equity team. He is a partner of the firm. Prior to joining GMO in 1995, he was a research scientist at Siemens and a software engineer at IBM. Dr. Hancock holds a Ph.D. in Computer Science from Harvard University and B.S. and M.S. degrees from Rensselaer Polytechnic Institute.

All data is as of 11/30/18, unless indicated otherwise. Disclaimer: As of September 30, 2018, with the exception of Assa Abloy, Atlas Copco, Schindler and Kone, McDonald’s Japan and Wal-mart de Mexico the securities discussed herein were held in the GMO Quality Strategy and are considered by GMO to be a “hold” recommendation. The information presented is not definitive investment advice, should not be relied on as such, and should not be viewed as a recommendation by GMO generally as of the date indicated. The securities are being discussed solely to illustrate GMO’s investment process and its analysis and views of the securities presented as of the date indicated. The securities presented are not representative of all of the securities purchased, sold or held for advisory clients, and it should not be assumed that an investment in the securities identified was or will be profitable. GMO’s views of, recommendations with respect to, and investment decisions regarding, the securities presented may vary across GMO’s strategies. Such recommendation is subject to change continually and without notice of any kind and may no longer be true after the date indicated.

Performance data quoted represents past performance and is not predictive of future performance. Returns are presented after the deduction of a model advisory fee and a model incentive fee if applicable. Net returns include transaction costs, commissions and withholding taxes on foreign income and capital gains and include the reinvestment of dividends and other income, as applicable. A GIPS compliant presentation of composite performance has preceded this presentation in the past 12 months or accompanies this presentation, and is also available at www.gmo.com. Actual fees are disclosed in Part 2 of GMO’s Form ADV and are also available in each strategy’s compliant presentation. Fees paid by accounts within the composite may be higher or lower than the model fees used. The above information is based on a representative account within the strategy selected because it has the fewest restrictions and best represents the implementation of the strategy. The information contained herein is supplemental to the GIPS compliant presentation that was made available on GMO’s website in September of 2018.

The views expressed are the views of Tom Hancock through the period ending December 2018, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. Forward‐looking statements based upon the reasonable beliefs of the author and are not a guarantee of future performance. Forward‐looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward‐looking statements. Forward‐looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated.

Copyright © 2018 by GMO LLC. All rights reserved.

1 Prior to the reclassification of Alphabet and Facebook to be in the “Communications Services” sector.

2 Source: www.multpl.com

© GMO

Read more commentaries by GMO