Key Points

■ A new model suggests that from early 2017 through much of 2018, the U.S. stock market was a bubble.

■ Driven by negative changes in sentiment, the bubble started to deflate in the fourth quarter of 2018, in spite of strong fundamentals.

■ Our advice, consistent with our portfolio positions established in Q1 2018 – as usual, we were early – is to own as little U.S. equity as your career risk allows.

Introduction

In the fourth quarter of 2018, the S&P 500 fell almost 14%. This large price drop occurred in spite of a strong fundamental backdrop. Earnings per share (EPS) for 2018, much of it already locked in, is expected to be about $140, a 28% increase over 2017. And expectations for 2019 are for EPS of about $156, a 12% annual increase. With fundamentals so good, what explains the recent price action?

A new model – the Bubble Model1 – explains this dichotomy between price action and fundamentals by suggesting that a bubble in the U.S. stock market started inflating in early 2017, and continued to inflate through the third quarter of 2018.2 In the fourth quarter, however, indications were that the bubble had started to deflate. And when bubbles deflate, they generally do so with a volatility bang.

In this new model, bubbles are prone to form when times are good and expected to get even better. Good times today and even better times ahead are reflected in high valuations and solid fundamentals that continue to improve. Improving fundamentals lead to positive changes in sentiment, and these positive changes in sentiment fuel the bubble. However, sentiment cannot increase forever. When change in sentiment – not level – inevitably turns negative as hopes of even better times ahead are dashed, there is nothing left to fuel the bubble.

In the context of market action over the past quarter, expectations of decelerating earnings growth – albeit still positive – reflect a negative change in sentiment. Furthermore, between August and December of 2018, estimated EPS for 2019 fell from $163.51 to $156.28, a decline of more than 4%. These earnings changes could reflect negative changes in sentiment. But other concerns, such as tightening by the Federal Reserve and trade tensions with China, can also cause negative changes in sentiment. And it is negative changes in sentiment – defined broadly – that can catalyze the pop.

While there are indications that the bubble started to deflate in the fourth quarter of 2018, and the magnitude of both price action and the change in the quantitative measure of euphoria that defines the Bubble Model suggest that the odds are now tilted in favor of the view that this is the beginning of the end of the bubble, we would be well-advised to remember Yogi Berra’s counsel that “It ain’t over till it’s over.” Past bubbles do exhibit “head fakes” in which bubble deflation is interrupted by a secondary growth event. For example, in the third quarter of 1998, the time of the LTCM crisis, the Bubble Model suggested the bursting of the bubble that had started inflating in early 1997.3 However, the 1998 reading was a head fake, and the bubble continued to grow for another 18 months before finally popping in early 2000.

To adopt the view that the price action over the last quarter is that of a bursting bubble, one first needs to believe that the market was a bubble in the first place. The claim that a stock market bubble inflated over the past few years is controversial (even here at GMO). I build the case by first introducing a quantitative definition of euphoria, and then view both the long history of U.S. stock market valuation and the events of the past few years through this lens

The challenge of defining a stock market bubble

A quantitative measure of euphoria: mean aversion driven by speculators

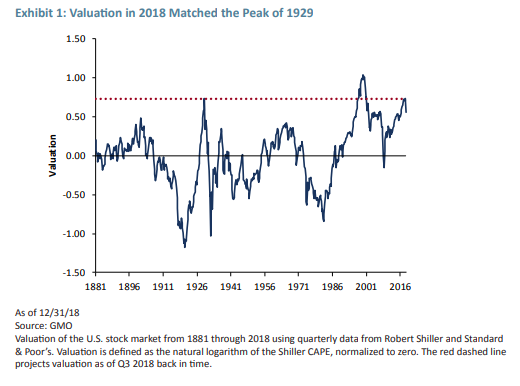

To appreciate the challenge of defining a bubble, we don’t have to go far. In spite of the fact that recent valuations, as shown in Exhibit 1, match the peak of 1929 and are only surpassed by the dizzying heights of the dot-com era of the late 1990s, keen market observers were hesitant to call the market of 2017-18 a bubble. The reason: a distinct lack of euphoria. While there were some signs of highly speculative behavior in the form of the stunning rise in the price of Bitcoin, or activity around Big Data and Artificial Intelligence, newspapers were not filled with stories of barbers or shoe shiners turned stockbrokers. So while one condition for a bubble was satisfied, high valuation, the other condition, euphoria, was arguably absent.

Bubbles have both quantitative and anecdotal characteristics. Jeremy Grantham’s preferred quantitative measure, which he has written about for decades, defines a bubble as a market trading at two standard deviations above trend. But bubbles are not only about high prices, they are also about animal spirits, captured in stories of euphoria. Economic historians have extensively documented these behavioral anecdotes for many bubbles over centuries. Speculators, imbued with animal spirits and driven by fear of missing out and dreams of getting rich, follow the herd and bid up prices with increasing fervor.

The quantitative and anecdotal elements of a bubble are, by their nature, very different. It can be challenging to get a clear-eyed view, especially in real time and without the benefit of 20/20 hindsight. Anecdotal elements are inherently subjective, and the challenge is further compounded by the fact that prices can stay high for extended periods of time, breeding confusion and uncertainty.

The Bubble Model, which focuses on the dynamics of valuation, captures both the quantitative and anecdotal euphoric elements of a bubble. Euphoria manifests as explosive dynamics, expressed quantitatively as a negative mean reversion speed. Because the model is quantitative, it does not suffer from the subjective uncertainties inherent in anecdotal stories. While most of the time valuation is mean reverting, on rare occasions valuation is temporarily explosive, or mean averting. This mean aversion goes hand in hand with expensive valuation and is the defining characteristic of a bubble.

Mean aversion, or explosive dynamics, arises when speculators dominate the market.4 Speculators are subject to fads and fashion and have a tendency to follow the herd. Their demand for stocks is ephemeral. Fundamental investors, on the other hand, assess value based on fundamentals and expected return considerations. Their demand for stocks is relatively stable. To the extent that fundamental investors dominate the market, fundamental value provides an anchor around which market prices vary.

This is standard mean reversion. However, when speculators dominate, i.e., the percentage change in speculative value exceeds that of fundamental value, then price tends to move away from fundamental value because deviations of price from fundamental value get relatively bigger. This is mean aversion.

Historical evidence of mean aversion

The question of whether or not the stock market displays mean averting behavior is a statistical one. A positive mean reversion speed means that price reverts to fundamental value, i.e., mean reversion holds. However, a negative mean reversion speed means that price moves away from fundamental value and mean aversion, not mean reversion, holds.

We can measure the mean reversion speed using standard econometric techniques.5 If the mean reversion speed is in fact constant, the estimate would show little to no variation, apart from measurement error. We find empirically that the mean reversion speed does indeed vary over time. And not only does the mean reversion speed change through time, but there are times, though rare, when the mean reversion speed becomes negative. These negative mean reversion speeds are a quantitative measure of euphoria and represent periods of explosive dynamics, or mean aversion.

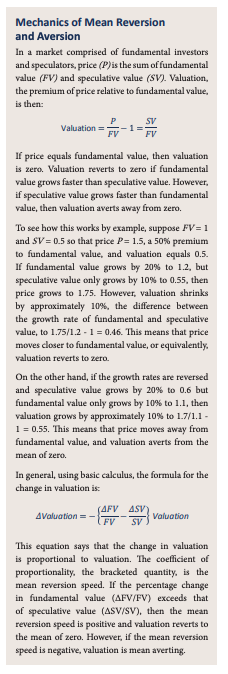

Exhibit 2 plots the empirical estimate of the mean reversion speed for the U.S. stock market from 1881- 2018. Because the vertical axis is flipped, points below the zero line correspond to positive mean reversion speeds. These are periods of mean reversion. We see that, on average, the mean reversion speed is positive (horizontal dashed line) so that most of the time mean reversion holds.

Between 1881 and today there are only five periods of explosive dynamics: 1) the late 1910s; 2) 1929; 3) the early 1980s; 4) the late 1990s; and 5) 2017-18. The first four periods are well known to market historians, while the fifth period, which begins in 2017, is still playing out. The late 1910s is the period of the Forgotten Depression, an era of deflationary pressures and a depression economy. The 1929 bubble marks the end of the Roaring Twenties and the beginning of the depression era of the 1930s. The early 1980s mark the end of the stagflation of the 1970s and the beginning of the almost 20-year bull market that culminated with the bubble of the late 1990s.

The five periods of explosive dynamics are highlighted by the solid red circles in Exhibit 2. Also highlighted in the dashed red circles are the periods of stronger than average mean reversion that follow each period of mean aversion. Note, in particular, the dramatic move from the third quarter to the fourth quarter of 2018.

While the conditions in 1929 and the late 1990s are consistent with a bubble – high valuation and mean aversion, or explosive dynamics – the late 1910s and the early 1980s are characterized by low valuation and explosive dynamics. In these periods, mean aversion means that prices are low relative to fundamental value, and expected to go even lower. Rather than a bubble, these periods define an antibubble (sometimes referred to as a negative bubble). In an anti-bubble, the psychology is dysphoric rather than euphoric.

The anatomy of 2017-18

A bubble…and initial stages of a pop

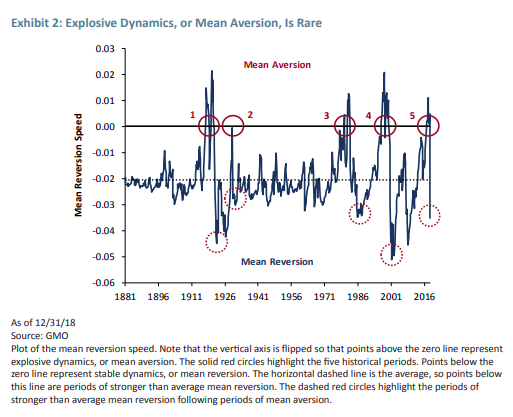

The fifth period of explosive dynamics, shown as a close-up in Exhibit 3, begins in 2017 and extends into late 2018. The mean aversion from early 2017 through the third quarter of 2018 is a quantitative measure of euphoria and suggests that during this period a bubble is inflating in the U.S. stock market, even though this period lacks the conventional anecdotes of euphoria, such as barbers and shoe shiners turned stockbrokers. And while such anecdotes appear lacking, the optimism and enthusiasm surrounding Big Data, Artificial Intelligence, and Bitcoin, among other technological advances, are typical of bubble-like animal spirits.

The data point for the fourth quarter of 2018 shows a dramatic change in the mean reversion speed, from an explosive, mean averting phase to a strongly mean reverting phase. The scale and duration of this move is consistent with the moves associated with the bursting of the 1929 and 1999 bubbles, and the reflation of the anti-bubbles of the late 1910s and the early 1980s.

One reason to take the Bubble Model seriously is that bubbles, and anti-bubbles, are rare. Since the late 1800s, we count only five episodes, including today’s. And four of these five are well known to market historians. It is likely that future market historians will learn to know the current episode as well.

Another reason to take this model seriously is that it is consistent with two recent market observations made by Jeremy Grantham, independent of the model. First, Jeremy writes in the Q3 2016 GMO Quarterly Letter about slowing mean reversion. The declining mean reversion speed in 2016, as shown in Exhibit 3, is consistent with this view. Second, in early 2018 Jeremy writes about a market melt up and the evolution of his thinking with respect to the importance of price acceleration. Both the market melt up and the importance of price acceleration are consistent with the mean reversion speed turning negative in 2017.

What can we expect when a bubble bursts?

Mean reversion comes back with a vengeance, and volatility rises

When a bubble bursts (or an anti-bubble reflates), mean reversion comes back with a vengeance. We can see this effect in Exhibit 2 where, as highlighted in the dashed red circles, following periods of mean aversion, mean reversion is stronger than average. Understanding this effect relies on insight from the model about a mechanism for the creation and destruction of bubbles (and anti-bubbles). The insight comes from analysis of the time series in Exhibit 2 and it reveals that periods of negative mean reversion are driven by the combination of positive change in sentiment and high valuation.6 This dependence on the combination of valuation and change in sentiment means that when valuation is extreme, relatively small changes in sentiment are amplified by the extended valuation and can produce large changes in price.

Simply put, bubbles are prone to form when times are good (high valuation) and expected to get even better (positive expected change in sentiment). Bubbles burst when hopes of even better times ahead are dashed. When these hopes are dashed, the positive change in sentiment turns negative. It is this flipping of the change in sentiment – not the level of sentiment – that drives the system back to a strongly meanreverting phase. And because the change in sentiment will at some point flip sign (after all, sentiment cannot keep growing forever), the bubble is guaranteed to pop.

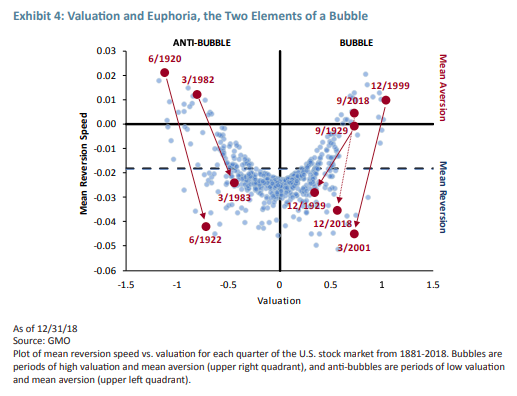

Another way to visualize stronger than average mean reversion following periods of explosive dynamics is to plot the time series of valuation and mean reversion speed on the same graph. Exhibit 4 plots the mean reversion speed from Exhibit 2 on the vertical axis and valuation from Exhibit 1 on the horizontal axis. Bubbles are points in the upper right hand corner and anti-bubbles are points in the upper left hand corner. Various bubble and anti-bubble dates are labeled, together with arrows that connect these dates with various points in the future. From this correspondence we see that the mean reversion speed changes by a large magnitude over a short period of time, and these changes correspond to a rapid transition from mean aversion back to stronger than average mean reversion.

Prior to the fourth quarter of 2018, the most extreme change in the mean reversion speed is the one from the third to the fourth quarters of 1929. Here, the mean reversion speed goes from slightly negative to strongly positive over the period of three months. However, the change in the mean reversion speed from the third to the fourth quarters of 2018 eclipses that of 1929, highlighting just how dramatic the last few months have been. The magnitude of this move also tilts the odds in favor of the view that we may currently be experiencing the initial stages of the bursting of the bubble of 2017-18.

Finally, a direct consequence of stronger than average mean reversion is that volatility in the post bubble period is higher than average. This is simply because stronger than average mean reversion means, by definition, that the magnitude of valuation changes, and therefore returns, are larger than average.

So, what do we learn?

Own as little U.S. equity today as your career risk allows

The Bubble Model teaches us that bubbles form when times are good – high valuation – and expected to get even better – changes in sentiment are positive. Bubbles burst when changes in sentiment – not level – turn negative. This dynamic helps us understand how it is that during the fourth quarter of 2018 the market fell dramatically, even though fundamentals, both past and expected, looked solid. While as of December, 2018 expected EPS growth for 2019 is 12%, this is substantially below the 28% growth of 2018. Furthermore, since August, 2018 estimated EPS for 2019 has been revised downward by more than 4%. These changes, together with concerns about Federal Reserve tightening and trade tensions with China, point to negative changes in sentiment, a catalyst for popping a bubble.

The key role played by changes in sentiment also highlights why it is so difficult to time a bubble. While the benefit of successfully riding a bubble and getting out in time is obvious, there are two reasons why this is a challenge. First, when the bubble pops, the reversal tends to be wicked, which is to say that mean reversion comes back with a vengeance. Mistiming can therefore be costly. Second, the odds of mistiming are high because the catalyst for the pop is a change in sentiment. It is not the level of sentiment that we need to predict, but rather the change, which is much more difficult. There is another subtle, but important point. I have been deliberately vague about what sentiment means. In Tarlie et al. (2018) the catalyst for both bubble formation and destruction is expected change in profitability. But more broadly we expect that change in sentiment is the catalyst, which is to say that there are myriad factors that can ignite animal spirits as the bubble forms, and then snuff them out as hopes for even better times ahead are dashed. Effectively, this vague definition reflects model risk. So even though we have a model that helps us understand how bubbles are created and destroyed, unfortunately it does not help us predict the timing of their demise. It does, however, give us insight into why timing is so challenging.

Our advice when the bubble is inflating is to avoid the siren song of buying into rising prices, thus avoiding the bubble altogether. While career risk can make this course of action difficult (hence giving further life to the bubble, of course), we believe the challenge of successfully timing the exit is such that bearing the career risk is the wiser and more prudent course for those with a sufficiently long time horizon.

Currently, we are faced with a volatile market that, through the end of 2018 at least, is down double digits from the September, 2018 peak. The volatility is consistent with a bubble bursting, though we caution that it is possible that the fourth quarter move in the mean reversion speed could be a head fake. While the dramatic nature of the move in the mean reversion speed to such strong mean reversion suggests that the odds are tilted toward this being the beginning of the end of the bubble of 2017-18, we cannot rule out reflation of the bubble, analogous to the event of late 1998-2000. Given that valuation is still high, our advice, consistent with our portfolio positions, is to continue to own as little U.S. equity as career risk allows.

Martin Tarlie. Dr. Tarlie is a member of GMO’s Asset Allocation team. Prior to re-joining GMO in 2018, he was a managing director at QMA. He previously worked on GMO’s Global Equity team from 2007 to 2014. Prior to that he worked at Breakwater Trading and at Marlin Capital Corp as a fundamental equity analyst and the director of research. Dr. Tarlie earned his B.S. in Physics from the University of Michigan, his Ph.D. in Theoretical Condensed Matter Physics from the University of Illinois at Urbana-Champaign, and his MBA from the University of Chicago. He was also a Postdoctoral Research Fellow at the James Franck Institute at the University of Chicago and is a CFA charterholde.

Disclaimer: The views expressed are the views of Martin Tarlie through the period ending January 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

1 This model appears in Martin B. Tarlie, Georgios Sakoulis, Roy Henriksson, “Stock market bubbles and anti-bubbles,” International Review of Financial Analysis, July 27, 2018. https://doi.org/10.1016/j.irfa.2018.07.012. A working paper is available at https://ssrn.com/abstract=2859795.

2 I presented evidence of a possible bubble in the U.S. stock market at the Paris Financial Management Conference in December, 2017 and at the Bernstein Quantitative Finance Conference in New York in October, 2018. My colleague, Catherine LeGraw, presented this same evidence at the GMO Client Conferences in Boston in November, 2018.

3 According to the Bubble Model, the bubble of the late 1990s began to inflate in the fourth quarter of 1996. Alan Greenspan delivered his infamous “irrational exuberance” testimony on December 6, 1996.

4 One of the original papers that explicitly models this phenomenon is Robert Shiller, “Stock Prices and Social Dynamics,” Brookings Papers on Economic Activity, 1984, pages 457-498.

5 The econometric problem is formulated as estimation of a time-varying regression coefficient. If the left hand variable is the future quarterly change in valuation, and the right hand variable is the current level of valuation, then the timevarying mean reversion speed is the time-varying regression coefficient relating the change in valuation to current valuation.

6 Tarlie et al. (2018) show that a key factor in explaining negative mean reversion speeds is the product of expected change in profitability (i.e., the ratio of earnings to fundamental value) and the level of valuation. But I expect that more generally it is change in sentiment (positively correlated with change in profitability) that combines with level of valuation to produce negative mean reversion speeds.

Copyright © 2019 by GMO LLC. All rights reserved.

© GMO

Read more commentaries by GMO