Deduction May Impact Some Advisory Businesses and Create New Planning Strategies for Business Owners

The Tax Cuts and Jobs Act of 2017 introduced a new 20% tax deduction focused on pass-through businesses. As tax accountants pore through the Internal Revenue Service’s recently released 184-plus pages of guidance on the so-called Section 199A deduction for “qualified business income” (QBI), many business owners are wondering whether they will qualify. The QBI deduction has implications for both advisors and their clients.

First, a little background. Qualified business income is a shareholder’s portion of pass-through income. Certain items, such as capital gains, are excluded. Pass-through businesses are those that don’t pay tax at the corporate level and rather “pass-through” the tax onto the owner or owners who report that income on their own individual returns. The structures, including sole proprietorships, partnerships, S Corporations, and limited-liability companies, prevent double taxation at both the corporate and individual level. Specified-service businesses, which have special qualification rules for the deduction, are those in which the reputation of a specified individual is a principal asset to the company (more on these in a minute).

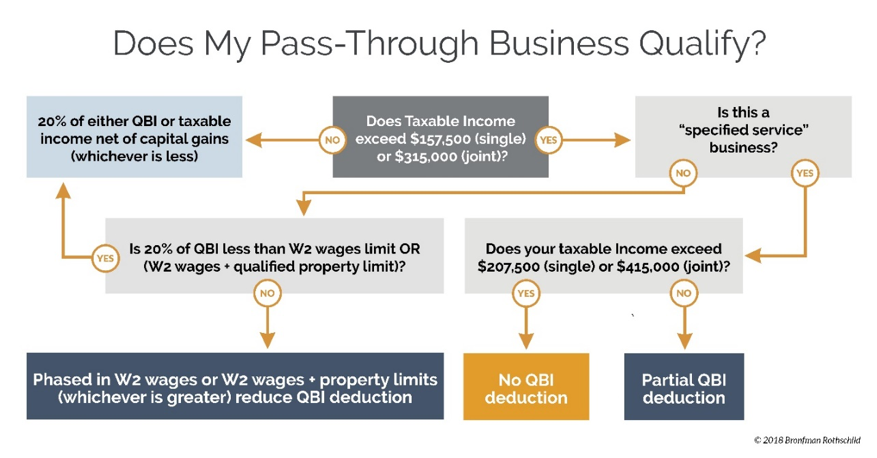

As determining whether you or your clients qualify for the deduction can be confusing, we’ve created the chart shown here, including details such as phaseouts. And as always, we recommend consulting with a tax accountant for more guidance:

As far as specified-service businesses, a bit of bad news for many professionals: Per the IRS, specified service trade or business (SSTB) includes a trade or business involving the performance of services in the field of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, investing and investment management, trading, dealing in certain assets or any trade business where the principal asset is the reputation or skill of one or more of its employees. It is important to note that these sorts of businesses are subject to QBI phaseouts based on taxable income.

What are the implications for advisors and their own businesses?

For many advisors, the law could affect their businesses, and perhaps not in a good way. As noted in the above conversation about specified service professionals, high income professionals—like financial advisors who rely on their personal labor—may not be eligible. The law carves out “any trade or business which involves the performance of services that consist of investing and investment management, trading or dealing in securities.”

To complicate this further, insurance advisors are not part of the SSTB carve out. However, insurance advisors with a financial services division may need to strategically consider the future of their financial services practice, especially if that income could threaten the QBI deduction on a more significant insurance practice. While it is beyond the scope of this article, Michael Kitces outlines considerations specifically for hybrid insurance producers.

W2 or contractor?

The QBI deduction is only applicable in cases where someone is receiving a portion of pass-through income. If all of your compensation as an advisor is in the form of W2 wages, there is no QBI deduction; however, if you’re an independent contractor, thoughtful QBI planning will be important. For instance, the make-up of your service offering may prove essential. As always, utilize the flow chart above and seek tax counsel to determine the impact of the various limits and phaseouts.

A new paradigm for compensation?

The new tax law may usher in significant changes to advisor compensation models. Those few with the autonomy (and justification) to determine their status as a W2 employee or an independent contractor may wonder which is preferable. On one hand, contractor income may qualify for the QBI deduction (it is important to note that moving from a W2 employee to an independent contractor, with few other changes, might not be sufficient for a QBI deduction). On the other, contractor income is “more expensive” relative to W2 earnings, as the worker is now responsible for all payroll taxes. Each case is unique and will require thoughtful planning and consultation with tax professionals.

The IRS is still addressing questions about the QBI regulations related to specified service businesses. In October, the IRS hosted a public hearing calling witnesses to clarify and interpret aspects of these rules, and it is expected they will further refine their guidance. In any case, advisors and advisory businesses should work closely with a tax professional to navigate this new and complex rule.

What advisors need to know about QBI to serve their clients

Beyond implications for their businesses, advisors must get their arms around what the new law means for clients. For many business owners with income “in the middle,” there is significant need for planning help. The design of the threshold invites planning strategies that may help business owners realize the full benefit of the deduction. These methods use strategic tax deductions, targeted income reduction and generation, and other important tactical items incorporated within an overall financial plan.

Charitable Giving

For those just above the income threshold who are likely to lose most (if not all) of the deduction, making a charitable gift could create significant tax savings. As QBI eligibility is based on taxable income, increasing below-the-line deductions through charitable gifts could potentially lower taxable income enough to qualify for the full deduction. Gifting securities with large long-term imbedded capital gains can add further tax savings. Also, using a donor-advised fund, which allows charitable contributions to be made for an immediate tax benefit and then be granted to charity over time, can allow this strategy to be implemented into a client’s long-term charitable legacy.

Consider the example of a family that owns a specified service business structured as an S Corporation. The couple has wage income of $225,000 and lists $300,000 in profits on the K1 statement for the S corporation. Let’s assume their expected Schedule A deductions are $10,000 for state and local tax (SALT) and $100,000 of charitable donations. Their taxable income of $415,000 exceeds the income limit so they will not be eligible for the QBI deduction.

But what if the family were to accelerate their next year of charitable gifts into this year? If the couple makes a charitable gift of $100,000 to a donor advised fund, they would reduce their taxable income to below the threshold and be able to collect the full QBI deduction of $60,000.

Retirement Planning

For those who have not already maxed out pre-tax contributions to their IRAs or qualified retirement plans, increasing deferrals could allow taxable income to qualify for the 199A deduction. If the business owner has not yet done so, establishing a profit sharing 401(k) or defined benefit plan can be an effective way to reduce income while supporting their retirement saving goals.

Roth Conversion Strategy

For some, the issue may be ensuring they have enough taxable income to avoid being limited by the overall limit of 20% of taxable income (net of capital gains). If already considering converting from a traditional IRA to a Roth for other financial planning purposes, this strategy could raise taxable income enough to help you realize the full QBI deduction (thus reducing the effective tax rate on the conversion). While this approach may present an opportunity to claim the full deduction, this will need to be weighed against the additional taxes incurred on the conversion.

Avoidance of Capital Gains

Long-term capital gains are generally taxed at a lower rate than ordinary taxable income. It is important to note, however, that capital gains can be detrimental to QBI as they increase taxable income. For a specified service business owner with taxable income directly on the income cusp of qualifying for the deduction, realizing capital gains could be the difference between qualifying for the full QBI deduction and receiving no QBI deduction. For example, say a joint household has $315,000 of taxable income and then adds $100,000 of capital gains to bring total taxable income to $415,000. Without the capital gains, the household would have been able to take a deduction of up to $63,000 (20% of $315,000); now they must pay capital gains tax on the $100,000 and no longer qualify for the QBI deduction.

While capital gains contribute to taxable income relative to the income thresholds mentioned above, they do not increase taxable income for the 20% of taxable income limit on the deduction. For this reason, the couple in the Roth conversion strategy was not able to accomplish their taxable income needs through realizing capital gains.

Conclusion

The above are just a few examples of the many different strategies that should be considered when navigating this complex tax law. It is important to ensure that a detailed examination is completed with your tax professional and implemented into your overall financial plan accordingly. Every individual situation contains its own unique aspects which may or may not warrant a revised planning strategy. But smart planning can open doors to take advantage of this important new deduction for business owners.

Bronfman E.L. Rothschild, LP is a registered investment advisor (dba Bronfman Rothschild and Bronfman Rothschild Wealth Advisors). Securities, when offered, are offered through an affiliate, Bronfman E.L. Rothschild Capital, LLC (dba BELR Capital, LLC), member FINRA/SIPC.

Certified Financial Planner Board of Standards, Inc. owns the certification marks CFP®, Certified Financial Planner™ and federally registered CFP (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

This information should not be construed as a recommendation, offer to sell, or solicitation of an offer to buy a particular security or investment strategy. The commentary provided is for informational purposes only and should not be relied upon for accounting, legal, or tax advice. While the information is deemed reliable, Bronfman E.L. Rothschild, LP cannot guarantee its accuracy, completeness, or suitability for any purpose, and makes no warranties with regard to the results to be obtained from its use. Past performance does not guarantee future results.

© 2018 Bronfman Rothschild

Read more commentaries by Bronfman E.L. Rothschild