Asset allocation proposals--helping an investor visualize how a particular asset allocation can best help them meet their goals--are a mainstay of winning new clients. But proposals can also be used to generate new business from existing clients. One way is through introducing the concept of asset location: allocating assets across the various accounts within a household to be more tax-efficient.

Many clients invest with multiple advisors or on multiple brokerage platforms, and may have assets spread across taxable, tax-deferred and tax-exempt accounts. Those assets may not all be under your purview. A discussion of asset location provides you an opportunity to gain insight into those holdings, with the potential of transitioning them to your book.

What exactly is asset location?

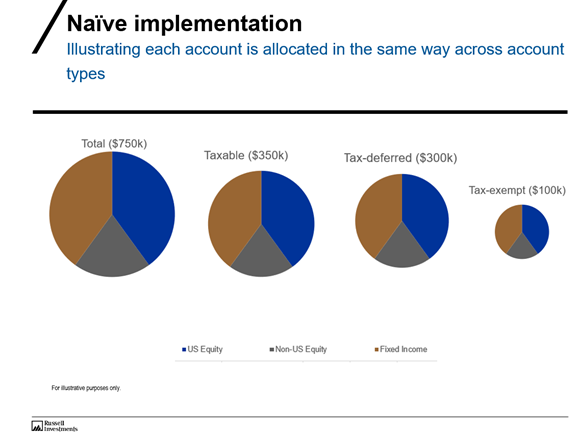

At the most basic level, it is allocating assets across a household in the most tax-efficient way possible. For example, let's say you have identified that a balanced allocation will best help your client meet their goals. Now, that client, like most investors, has money spread across taxable, tax-deferred and possibly tax-exempt accounts. A naive implementation of that balanced allocation across the whole household would allocate each different account--taxable, tax-deferred and tax-exempt--in the same way, each with the same asset allocation.

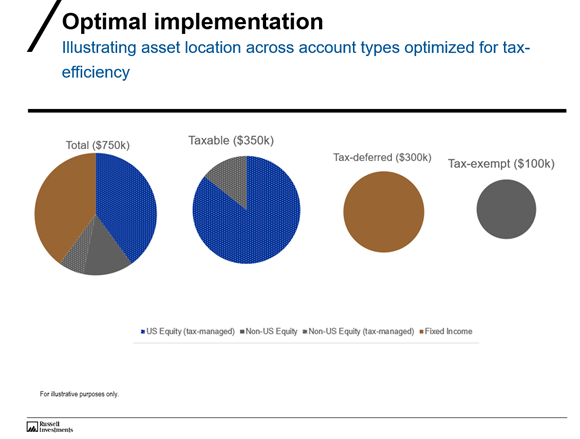

But some asset classes are more tax-efficient than others. Income-generating asset classes (like fixed income and real estate) may or will generally generate higher tax bills than asset classes with a focus on capital growth, or asset classes managed for taxes (like tax-managed funds). So, wouldn't it make more sense to optimally locate the asset allocation across the various account types, so that when viewed in aggregate, the total portfolio (household) rolls up to the balanced allocation AND is optimized for tax-efficiency? That, in a nutshell, is asset location. In our view, asset location is becoming one of the most under-appreciated traits of top wealth managers and a competitive advantage.

So how to do it?

Generally speaking:

- Assets that tend to be more tax-efficient and/or can be managed to help minimize tax costs (think municipal bonds or mutual funds specifically managed for taxes) should be used in non-qualified accounts.

- Assets that aren't typically tax-efficient or that could lose a meaningful amount of value to taxes (think commodities, real estate investment trusts, taxable bonds, non-U.S. equities) should be used primarily in qualified accounts.

For example, when looking at a fixed income portfolio, both tax-exempt bonds (municipal bonds) and corporate and high-yield debt can be valuable in a client's portfolio. But if they are in the wrong type of accounts, their effectiveness may be reduced.

Here's the business building part: to implement asset location correctly, you need to see and understand all of the client's assets and whether they are currently located in qualified or non-qualified accounts. The following may be a helpful way to jump-start this dialogue with a client: In order to make a better total portfolio allocation, efficiently locating your assets across your multiple accounts, I need to see how those accounts are allocated. Can you provide current statements of all your accounts?

The bottom line

The potential benefits to clients of such hands-on oversight and tailored solutions that take into account their total investment portfolio are clear. These clients are likely to recognize and appreciate the care you put into developing a deep understanding of their entire financial picture, in addition to formulating a financial plan and solution set designed to meet their unique goals. Bear in mind that when adopting an asset location strategy for your clients, you will need to set appropriate performance expectations for the individual accounts, as they will vary greatly. Clients must remember to mentally combine the accounts together and consider performance as a whole (and you can help by providing a performance report at the household level).

As for you? This approach can help uncover hidden assets--those assets your client may have declined to disclose to you--and potentially increase your key clients' loyalty to you, helping you grow your business in the areas where you can add the most value. Don't shy away from these client situations--relish them for the challenge and growth opportunity they can represent.

© Russell Investments Group, LLC. 1995-2019. All rights reserved.