Credit investors faced many headwinds in 2018 as financial conditions tightened, foreign demand faded, and spreads widened. Despite tailwinds from a booming economy and strong earnings growth, most credit sectors saw negative total returns. Today, many challenges remain, and the growth tailwind may be fading. But there is a certain type of fixed income strategy that can help mitigate the effects of market noise and may help investors pinpoint more attractive opportunities — defined maturity bond funds.

2018: A difficult year for credit investors

A flatter yield curve. As expected, the Federal Reserve continued to push rates higher and shrink its balance sheet in 2018. Rates on 1-year and 2-year Treasuries rose about 50% and 30% respectively, rates on 5-year and 10-year Treasuries rose about 13%, and rates on 30-year Treasuries rose about 10%.1 As shown in the chart below, this had a flattening effect on the yield curve, pushing the spread between 2-year and 10-year Treasuries to just 20 basis points to close the year — about 84% below the historical average.

What does a flatter yield curve mean to credit investors? With a flatter yield curve, there is less compensation for taking on duration risk. This has also made the short end of the curve (reflecting durations of one to three years) more attractive.

Source: Bloomberg L.P. as of Dec 31, 2018. Data from March 31, 1977, to Dec 31, 2018, from Market Matrix. US Sell 2 Year Buy 10 Year Bond Yield Spread

On the other hand, the investment grade credit curve steepened, as non-US demand for corporate bonds dropped, concerns over a global growth slowdown rose, and perceived credit risk increased. Strong US pension demand, however, did help tether the longer end as corporations capitalized on higher tax rates in 2018. Pension buying of corporates in the first half of 2018 alone accounted for four times the inflows seen in all of 2017.2

Source: Bloomberg, L.P., as of Dec. 31, 2018. The points represent the BulletShares Corporate Bond ETFs with maturity dates of 2019 through 2026

Widening spreads. In February 2018, the spread between investment grade bonds and Treasuries hit their tightest level for this cycle, and the spread between high yield bonds and Treasuries followed suit in October. However, both spreads widened with the December uptick in volatility. Investment grade spreads now sit 12% above their historical median while high yield spreads sit 6% below historical median levels (dating back to 2010).1Despite the aforementioned concerns heading into 2019, end-of-2018 spread widening has potentially made both investment grade corporate and high yield corporate bonds more attractive for investors.

What may be in store during 2019?

Given that the Fed softened its rhetoric around rate hikes and balance sheet normalization earlier in the month, investor fear of rising rates has been reduced. However, even if the Fed decides to pause its rate increases, challenges may remain as deteriorating economic conditions would be the likely cause for a pause.

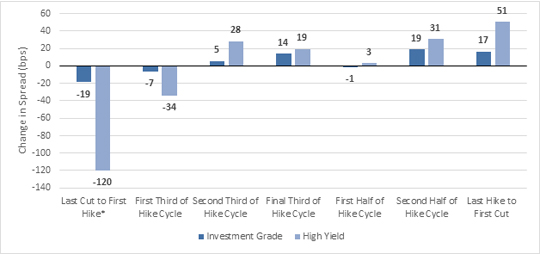

The chart below illustrates the spreads between high yield (HY) and Treasuries, and investment grade (IG) and Treasuries, at different points during past Fed hiking cycles. The period following the final Fed hike (“last hike to first cut”) has been a difficult one for investors as these spreads have softened.

IG and HY spreads during different points of past Fed hiking cycles

Source: Bloomberg L.P. as of Oct. 31, 2018. Data for periods Feb 1994 – Feb 1995, June 1999 – May 2000, and June 2004 – June 2006. *HY option-adjusted spread not available for first period as of September 1992, so this average only has two periods.

How defined-maturity bond funds may help

With uncertainty around rates, credit spreads and growth, investors may be inclined to look to defined-maturity bond funds. Unlike traditional fixed income funds that tend to sell bonds before their maturity date, defined-maturity funds seek to hold securities through final maturity—at that time, investors can take the proceeds from the maturing bonds, or reinvest the proceeds in a different ETF with a new maturity date.

By rotating into a defined maturity vehicle, such as Invesco’s BulletShares exchange-traded funds, investors may be able to help mitigate market noise. If rates go up and spreads widen, investors have the option to hold until final maturity. If the opposite occurs, investors have exposure to credit markets and may have the ability to capture any potential rally in credit.

As BulletShares defined-maturity ETFs are available across the yield curve, investors can efficiently ladder a portfolio. A ladder is a portfolio of bonds that mature at staggered intervals across a range of maturities. Assuming rates rise, proceeds from each maturing rung of defined maturity ETFs can be reinvested in longer-dated funds at higher rates. If market interest rates fall or remain flat, fund holders can stay invested and take the proceeds when the funds mature.

Learn more about Invesco’s BulletShares ETFs.

1 Source: Bloomberg L.P. as of Dec. 31, 2018

2 Source: Sources: Federal Reserve, Wells Fargo Credit Strategy and Bloomberg L.P. as of Sept. 28, 2018.

Important information

Blog header image: AshDesign/Shutterstock.com

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Yield spread is the difference between yields on differing debt instruments, calculated by deducting the yield of one instrument from another.

The yield curve plots interest rates, at a set point in time, of bonds having equal credit quality but differing maturity dates to project future interest rate changes and economic activity. The “short end” of the curve refers to bonds with shorter maturity dates.

A flat yield curve is one in which there is little difference in the yields for short-term and long-term bonds of the same credit quality. In a normal yield curve, longer-term bonds have a higher yield.

Duration is a measure of the sensitivity of the price (the value of principal) of a fixed income investment to a change in interest rates. Duration is expressed as a number of years.

The risk-free rate represents the interest an investor would expect from an absolutely risk-free investment over a specified period of time.

Maturity is the date on which a debt security becomes due and payable.

There are risks involved with investing in ETFs, including possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The funds’ return may not match the return of the underlying index. The funds are subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the funds.

Investments focused in a particular sector are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

The funds are non-diversified and may experience greater volatility than a more diversified investment.

Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

During the final year of the funds’ operations, as the bonds mature and the portfolio transitions to cash and cash equivalents, the funds’ yield will generally tend to move toward the yield of cash and cash equivalents and thus may be lower than the yields of the bonds previously held by the funds and/or bonds in the market.

An issuer may be unable or unwilling to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Income generated from the funds is based primarily on prevailing interest rates, which can vary widely over the short- and long-term. If interest rates drop, the funds’ income may drop as well. During periods of rising interest rates, an issuer may exercise its right to pay principal on an obligation later than expected, resulting in a decrease in the value of the obligation and in a decline in the funds’ income.

An issuer’s ability to prepay principal prior to maturity can limit the funds’ potential gains. Prepayments may require the funds to replace the loan or debt security with a lower yielding security, adversely affecting the funds’ yield.

The funds currently intend to effect creations and redemptions principally for cash, rather than principally in-kind because of the nature of the funds’ investments. As such, investments in the funds may be less tax efficient than investments in ETFs that create and redeem in-kind.

Unlike a direct investment in bonds, the funds’ income distributions will vary over time and the breakdown of returns between fund distributions and liquidation proceeds are not predictable at the time of investment. For example, at times the funds may make distributions at a greater (or lesser) rate than the coupon payments received, which will result in the funds returning a lesser (or greater) amount on liquidation than would otherwise be the case. The rate of fund distribution payments may affect the tax characterization of returns, and the amount received as liquidation proceeds upon fund termination may result in a gain or loss for tax purposes.

During periods of reduced market liquidity or in the absence of readily available market quotations for the holdings of the fund, the ability of the fund to value its holdings becomes more difficult and the judgment of the sub-adviser may play a greater role in the valuation of the fund’s holdings due to reduced availability of reliable objective pricing data.

The funds’ use of a representative sampling approach will result in its holding a smaller number of securities than are in the underlying Index, and may be subject to greater volatility.

BulletShares High Yield ETFs

The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

BulletShares Emerging Markets ETFs

Non-investment grade securities may be subject to greater price volatility due to specific corporate developments, interest-rate sensitivity, negative perceptions of the market, adverse economic and competitive industry conditions and decreased market liquidity.

The funds may invest in privately issued securities, including 144A securities which are restricted (i.e. not publicly traded). The liquidity market for Rule 144A securities may vary, as a result, delay or difficulty in selling such securities may result in a loss to the fund.

The funds may hold illiquid securities that it may be unable to sell at the preferred time or price and could lose its entire investment in such securities.

Government obligors in emerging market countries are among the world’s largest debtors to commercial banks, other governments, international financial organizations and other financial instruments. Issuers of sovereign debt or the governmental authorities that control repayment may be unable or unwilling to repay principal or interest when due, and the fund may have limited recourse in the event of default. Without debt holder approval, some governmental debtors may be able to reschedule or restructure their debt payments or declare moratoria on payments.

Shares are not individually redeemable and owners of the Shares may acquire those Shares from the Fund and tender those Shares for redemption to the Fund in Creation Unit aggregations only, typically consisting of 10,000, 50,000, 75,000, 80,000, 100,000, 150,000 or 200,000 Shares.

Timothy Urbanowicz, CFA®

Senior Fixed Income ETF Strategist

Tim Urbanowicz currently serves as the Senior Fixed Income ETF Strategist for Invesco’s exchange-traded funds (ETFs). In his role, he works on researching and developing product-specific strategies, as well as creating thought leadership to position and promote the fixed income ETF lineup.

Previously, Mr. Urbanowicz served as the head strategist for the ETF capital markets group, working with investment banks, trade desks and other institutions that are instrumental in providing liquidity in the global ETF market. He joined Invesco in 2011.

Prior to joining Invesco, Mr. Urbanowicz was an investment representative with JPMorgan Chase as part of a wealth management team servicing the needs of high-net-worth individuals.

Mr. Urbanowicz earned a BA degree in business and economics from Wheaton College in Illinois, and holds the Series 6, 7, 24 and 63 registrations. He is also a Chartered Financial Analyst® (CFA) charterholder.

Read more commentaries by Invesco