Is the Economic Slowdown Over or Just Getting Started? Part 2

In Part 1 of this series we talked about the lagged effect of interest rates and money growth, AKA “financial conditions” broadly speaking, on economic growth. We noted that changes in interest rates tend to impact economic growth with about a 2 year lag and changes in money supply tend to impact growth with about a 6 month lag. As such, the more than doubling in long-term US interest rates from mid-2016 to mid-2018 will be felt through the remainder of 2019 and the drop off in the monetary base thanks to Fed balance sheet shrinkage will be felt at least through the summer of 2019. This implies that the slowdown in US econ data is really just in its infancy and that the stock market may have gotten slightly ahead of itself in discounting a V-shaped recovery in the econ data. Indeed, it may useful to remind oneself of this fact on days like today when the market is up in part due to a positive surprise from the Caixin China PMI (it came in at 49.9 vs expectations of 48.5). After all, the other Chinese manufacturing PMI that was released just Wednesday disappointed as did today’s US manufacturing ISM.

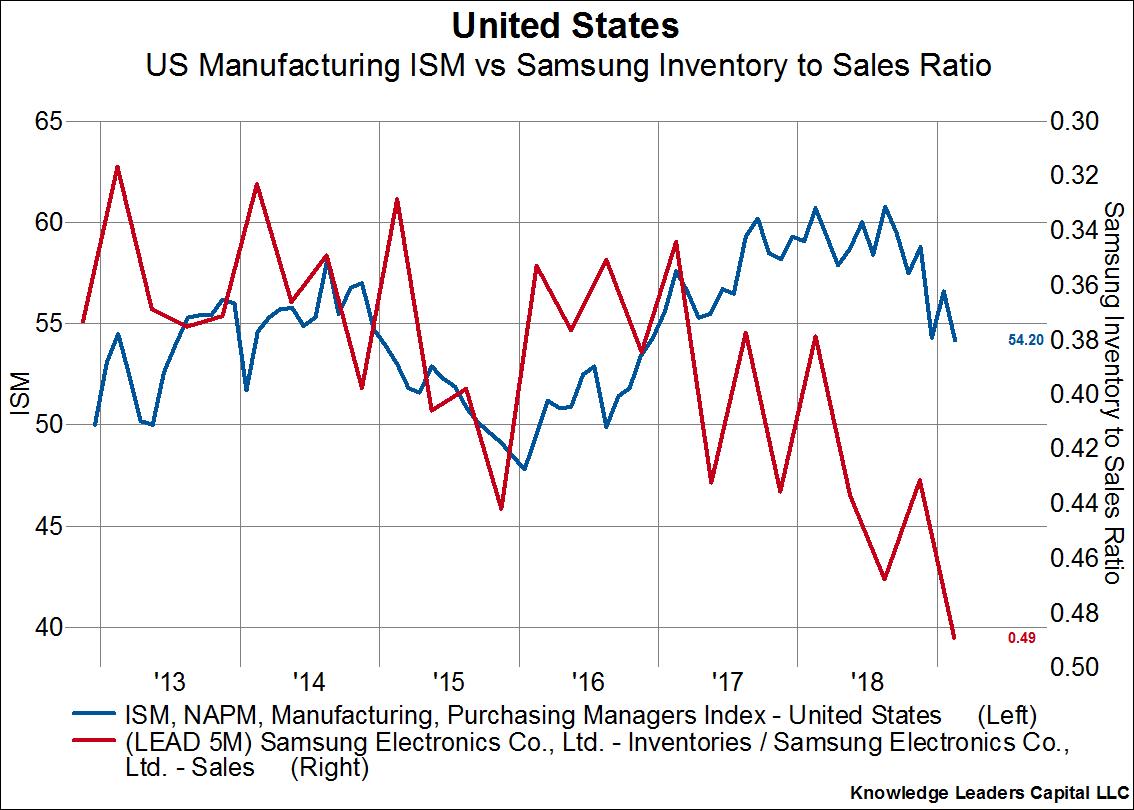

Monetary phenomenon aside, we observe ample confirmatory indicators from the supply chain that all is not well despite China’s months long easing campaign and the easing of Fed forward guidance. Specifically, it’s the beginning of the global supply chain that not only remains palatably weak, but also points to a further slowdown in US economic data. Of course, the fact that US economic data would lag economic changes in countries at the very beginning of the supply chain makes sense, since the US as the world’s largest consumer is located at the end of the supply chain.

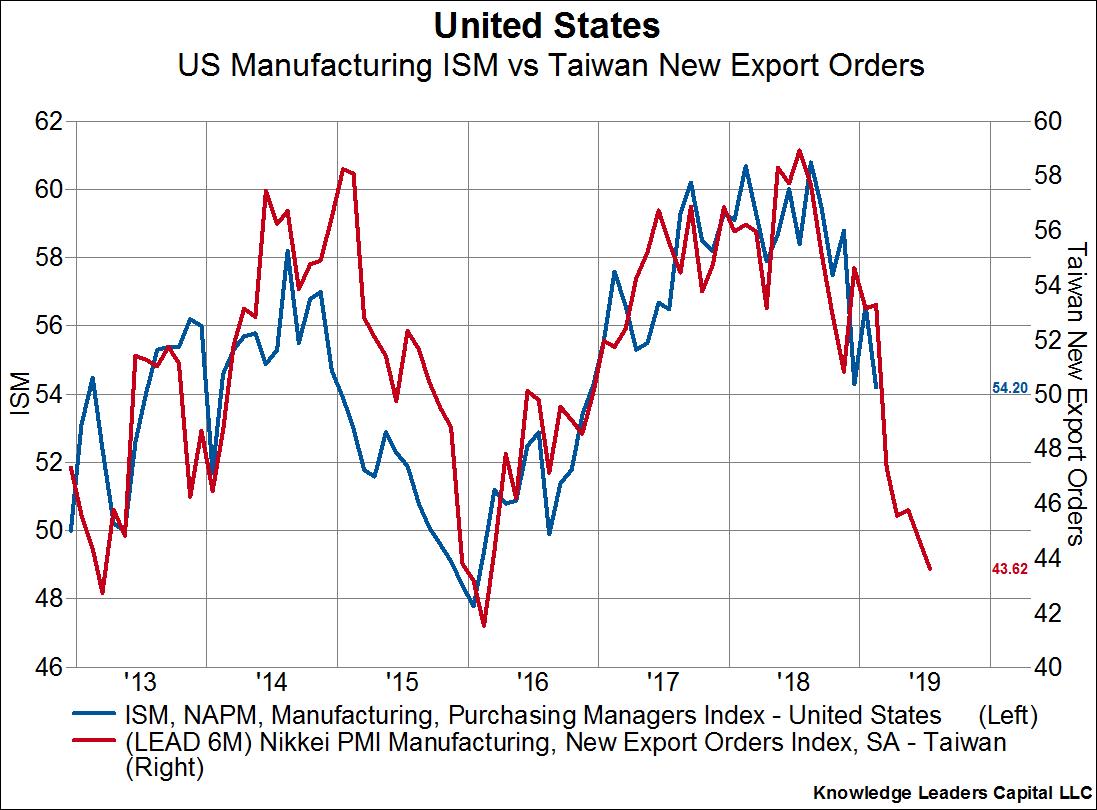

Taiwanese new export orders are a perfect example. New orders are the among the most forward looking series for any country’s economy and tend to lead hard data by about a quarter. When we compare new export orders from a country like Taiwan that produces semiconductors and other electronic components (i.e. piece parts of end use consumer goods) to US economic growth, it follows that the Taiwan export orders series should lead US growth by some healthy margin. And indeed it does. Taiwan new export orders lead the US ISM by six months and are making a b-line toward the 2016 lows. If the relationship holds then the weakness we observed in today’s US ISM print should continue through July at the earliest.

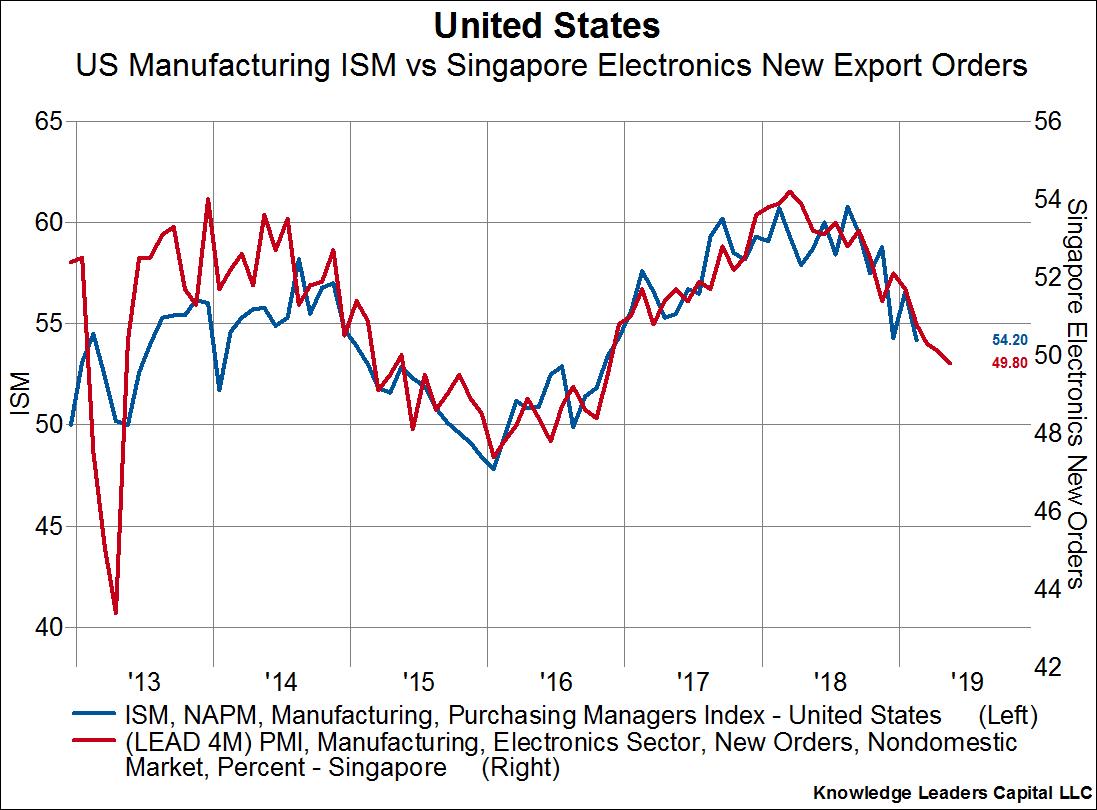

What’s more, Taiwan export orders aren’t an outlier. We get the exact same message from Singapore new electronics export orders, albeit with a slightly smaller lead time of four months.