In October 2018, we published our views on the growing glut of BBB-rated corporate debt. The headline takeaway was the following: longer-term we have concerns, but shorter term a downgrade cycle did not appear imminent. In our multi-sector strategies, this view helped us capitalize on the December volatility and position our portfolios for the bounce back and strong rally in credit markets to start the year.

Since we published our view, ominous headlines about growing BBB debt and highly leveraged companies have only continued to mount. Given this headline noise, we have prepared a more detailed follow-up to help our clients navigate this volatile and uncertain market backdrop.

Downgrade cycle imminent? Depends on how you look at it.

Analyzing risk and opportunity requires a comprehensive view of not only historical market performance, but also current market conditions. Leverage, while certainly important, requires context to account for market fundamentals and characteristics that are unique to this credit cycle. As we noted in our initial post, although leverage has increased for investment grade companies, much of this increase has been the result of M&A transactions by larger companies that have several levers to pull to ensure they remain investment grade. We have also observed that many of these companies are higher quality companies that operate in defensive sectors, which should help insulate them from an economic downturn.

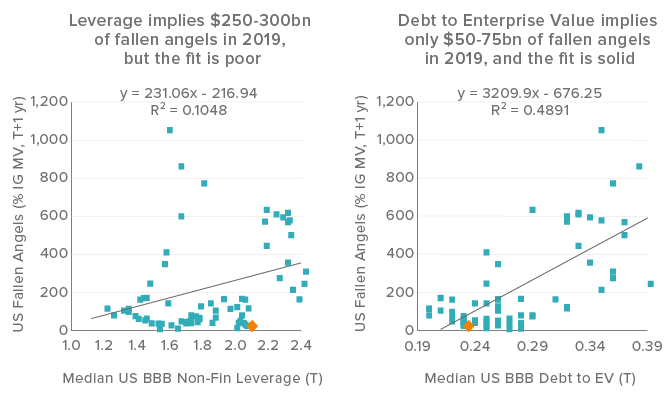

Figure 1. Leverage is not the only lens to view current credit market risk

Source: Moody’s, Worldscope, Bloomberg Barclays Index Services Limited, UBS. As of 9/30/18.

In addition, per Figure 1, there does exist an alternate framework for gauging BBB downgrade risk. Of note, BBB leverage has a less reliable fit than debt-to-enterprise-value as a predictor of potential fallen angel volume. Leverage metrics, such as Debt to EBITDA, assess the level of debt relative to trailing cash flows, which makes these metrics backward looking. In contrast, the debt-to-enterprise value metric assesses leverage based upon the market’s forward-looking expectations for the company. In essence, it provides a real-time measure of the equity cushion supporting the level of debt. As Figure 1 shows, this debt-to-enterprise value ratio is forecasting a much more benign scenario for fallen angels in 2019.

Source: JPMorgan, Bloomberg, Voya Investment Management. As of 12/31/18

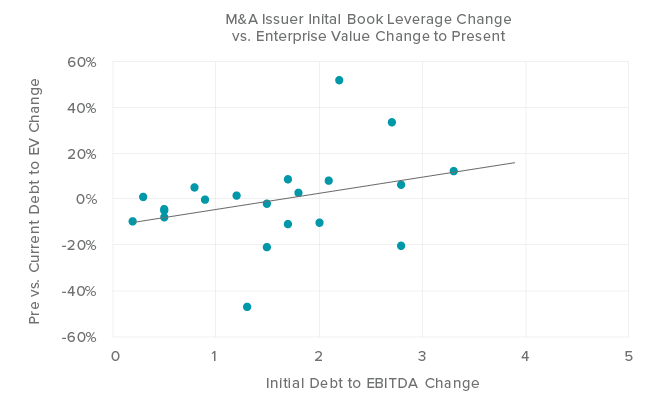

A few additional metrics to support this notion for reduced concern over the short-term include the leverage dynamics of last year’s M&A transactions and a closer look at interest coverage ratios. As Figure 2 shows, while book leverage increased by zero to three turns as a result of each deal, market leverage for these issuers went largely sideways relative to the pre-acquisition time period. In other words, from a market perspective leverage has not changed, but the longer term fundamentals resulting from the transactions could very well contain encouraging credit stories worthy of consideration. And while a large stock market sell-off does pose a risk to this measure, we nonetheless believe this illustrates a measure of fundamental stability.

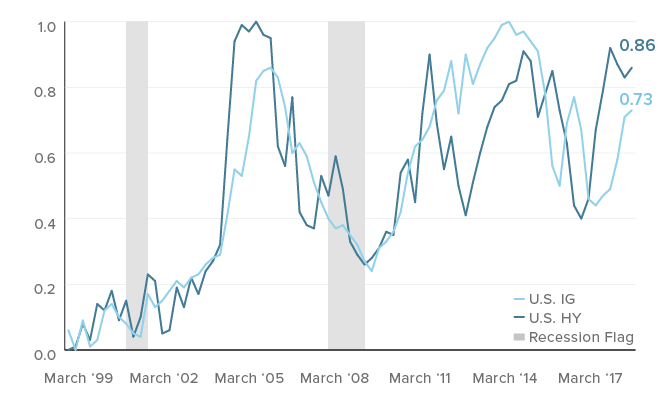

Furthermore, as we also noted in our initial post that the higher rate of net leverage and declining coverage ratios is a running and understandable concern for investors. However, we take a somewhat contrarian view in that we think current interest coverage is an offset to leverage. Why? Per figure 3, if the Federal Reserve is truly close to concluding the current tightening trend, then the monetary policy influence on this metric should also be largely complete. In other words, the big interest coverage convergence to lower levels that some have feared may not take place, absent a slowdown in growth.

Median EBITDA to Interest Expense ratio, percentile back to 1999

Source: Worldscope, Bloomberg, UBS. As of 9/30/18

What continues to matter most in this environment? Security selection

While we continue to believe that a downgrade cycle is not imminent, we acknowledge that we remain in the latter stages of the business cycle, particularly as it relates to corporate credit. In this environment, security selection is more important than ever. While security selection is obviously conducted on a case-by-case basis, our higher level view of the credit markets provides valuable insight, particularly as it relates to the efficacy of leverage as an indicator of risk. In this environment, we are more focused on the strength of the company than the strength of the balance sheet.

Going forward, we feel the greatest longer term value will be found among issuers that may be slightly more leveraged but with solid fundamentals, versus those that may currently have healthy balance sheets but poor fundamentals.

Despite headline concerns, we are maintaining our focus on identifying issuers with strong market-share leadership, stable cash flows and a management team with a track-record of deleveraging when the opportunity arises, as well those with a low to moderate dividend burden and a low capital intensive business model. It is important to note that not every company will exhibit all of these characteristics, but it is often possible to find issuers with most of them.

We believe this high-level view of credit markets combined with our unwavering commitment to bottom-up security selection will help us navigate what is sure to be a volatile and uncertain path ahead.

This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) changes in laws and regulations and (4) changes in the policies of governments and/or regulatory authorities. The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.