In perhaps the most deliciously ironic example of misattribution of all time, Mark Twain is often held to have said “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so”. There is no evidence that Twain ever said or wrote those words, but the sentiment is indeed valid irrespective of the authorship. It resonates particularly on the subject of so-called total factor productivity growth (TFP). This once arcane topic has found its way into more mainstream discussions. For instance:

The productivity slowdown is a major explanation for the stagnation in real incomes…This seems to reflect weak investment and, above all, declining growth of “total factor productivity,” a measure of output per input of capital and (quality-adjusted) labour. TFP is a measure of innovation, of the ability to produce more valuable output with given quantities of inputs. Without innovation, the rising prosperity of the past two centuries would have been impossible. In truth, innovation…is almost everything.

The Financial Times, 12 June 2018

So why are rich countries growing so slowly? Part of it is due to the lingering effects of the Great Recession, but part is due to a slowdown in the rate of productivity growth. Productivity is any economy’s long-term underlying engine of growth: once you put all of a country’s people to work and provide them with as much capital equipment as they can use, further growth depends on the efficiency with which they can create goods and services – i.e. on productivity.

Bloomberg, 8 October 2018

China’s economy is slowing…After the financial crisis, China’s total factor productivity growth – a measure of how fast an economy increases the efficiency with which it uses labour and capital – suddenly began to fall, and has stayed low ever since.

Bloomberg, 15 January 2019

As the above makes clear, economists often tend to fetishize productivity in general. Productivity is often talked about as if it were a real thing – rather than the result of calculation (output divided by hours worked). This is then compounded when so-called growth accounting exercises are undertaken, and the topic turns to the mysterious TFP.

Growth accounting is often framed in terms of a Cobb-Douglas production function:

Where Y is output, L is the actual number of hours worked, K is the value of the capital stock, and A is a scale factor, the exponent ɸ is often assumed to correspond to the observed labour share of income.

When Solow first laid out his framework way back in 1957, he himself noted “it takes something more than the usual ‘willing suspension of disbelief’ to talk seriously of the aggregate production function”. This is something of an understatement. There is almost no reason to assume such a thing exists at all.

As Franklin Fisher (an MIT professor) has written,1 “Indeed it is truly amazing that, after so many years, we should be having a symposium of aggregate production functions: for, perhaps even more than the square root of negative one, aggregate production functions are truly imaginary…Nevertheless, economists go on behaving as if there were no problem here”. Indeed one of our colleagues made what we believe was an appeal to the wisdom of crowds when he observed “plenty of economists seem to believe there is benefit of using a production function”. However, since we have spent a good deal of our lives disagreeing with the majority of economists this left us unmoved. We find it reminiscent of Greenspan’s statement in 1999 that “To spot a bubble in advance requires a judgement that hundreds of thousands of informed investors have it all wrong”.

Despite the tenacity of many economists, the aggregate production function is riddled with problems. As Joan Robinson long ago noted:2

The production function has been a powerful instrument of miseducation. The student of economic theory is taught to write Q = f (L, K) where L is a quantity of labour, K a quantity of capital, and Q a rate of output…He is instructed to assume all workers alike, and to measure L in man-hours of labour; he is told something about the index number problem involved in choosing a unit of output; and then he is hurried on to the next question, in the hope that he will forget to ask in what units K is measured. Before ever does he ask, he has become a professor, and so sloppy habits of thought are handed on from one generation to the next.

How do you go about adding up all the different types of capital in an economy? How do you combine shovels and semiconductors in some non-monetary fashion?3

This is just one of many ‘aggregation issues’. Even if one allows for the existence of well-defined and optimized production functions at the level of the firm (already an implausible belief), the aggregation from the micro to macro requires such stringent conditions that it is almost impossible to believe in an aggregate production function. For instance, you would need to believe that all firms employ different types of identical workers in the same proportion, you would need to believe all firms produce all outputs in the same proportion (no specialization in production), and you would need to believe all micro production functions are identical except for the capital efficiency coefficient. Clearly, these assumptions are at odds with reality.

Nor is it acceptable to argue that the aggregate production is an approximation, close enough to reality for working purposes. As Fisher opines,4 “One cannot escape the force of these results by arguing that aggregate production functions are only approximations…good approximations to the true underlying technical relations require close approximations to the stringent aggregation conditions, and this is not a sensible thing to suppose”.

However, never ones to be daunted by such untidy concepts as reality, economists have steadfastly continued to use (and abuse) the aggregate production function to this day. In general their defense appears to be that when estimated empirically the model fits the data very well. However, this has nothing to do with the usefulness of the model and everything to do with the fact that such estimates are really running regressions on an identity that ensures a great fit (equation 4 is the identity in question). This is perhaps the greatest criticism of all, because even if there were no aggregation issues, estimating an identity is a fruitless exercise that can reveal nothing.

Way back in 1957 Solow suggested that TFP growth could be treated as an unobserved variable equal to the ‘unexplained residual’ in a growth accounting framework. That is to say, using log differentiation the production function above becomes:

This can obviously be rearranged to give an equation for TFP growth (the Solow residual).

This is then interpreted in a wide variety of ways. For instance, Gordon describes it as “the best available measure of the underlying pace of innovation and technological change,”5 Furman states it “tells us how efficiently and intensely inputs are used…This is easily mapped to innovation of the technological and managerial sorts.”6

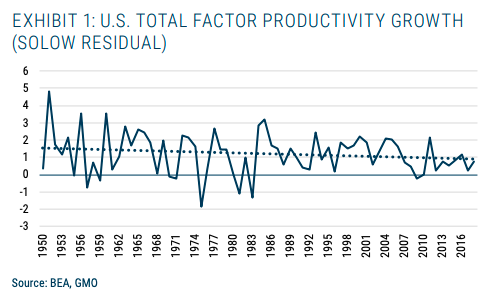

This is all the more concerning when one is then shown estimates of the Solow residual that exhibit a downward trend over time (as per Exhibit 1). Some argue that this is a permanent decline (the supply-side pessimists) driven by societal decay and a chronic lack of investment in education etc. Others suggest that this is a tempoorary slowdown (the technology optimists), and that innovation is still alive and well.

We would suggest a third perspective – the Solow residual doesn’t really measure anything as profound as is widely claimed.7

Let’s start by pointing out that National Income Product and Accounts follow the form:

Where ω is an index of the real wage, and r is the rate of profit. So (4) simply says that valued added can be decomposed between labour and capital.

As before, we can log differentiate the above equation and we get:8

Where a hat denotes growth rate, and φ is ωL/GDP, which is of course the labour share, and 1 - φ is the capital share.

Now we can define TFP as a residual again:

Substituting our expression for GDP (5) into the definition of TFP (6) reveals:

That is to say that TFP is nothing more than the weighted average of real wage growth and profit growth, pure and simple. Note that we didn’t need to invoke any aggregate production function or make any assumptions about the nature of competition to derive this. We simply needed the national income identity.

One can also rewrite the equation 6 (or, equivalently, equation 3) as:

This makes it clear that TFP is just a weighted average combination of labour productivity growth and capital productivity . It is hard to see why a weighted average of these productivities should be seen as a measure of technological innovation.

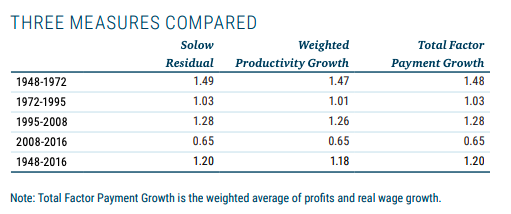

To show the natural equivalence of these measures (given that the Solow model is estimated on national income accounts that contain the identity (4) by construction) we can look at the table below. This shows the three ways of calculating TFP growth as above. The first column is calculated as per equation 3, the second column is calculated as per equation 8, and the third column is calculated as per equation 7.

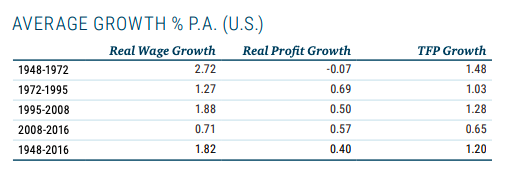

Unsurprisingly given the analysis above, all three methods produce essentially the same outcome. Remember two of these methods involve no concept of an aggregate production function at all. In fact, TFP could be dropped from economists’ toolkits altogether as it tells us nothing at all. The slowdown in TFP growth is actually a reflection of the well-documented, very slow wage growth that has been observed.

There is no mystery behind the TFP growth slowdown. Time would be much better spent understanding why real wage growth has slowed so dramatically.

© GMO LLC.

© GMO

Read more commentaries by GMO