It has been ten years since the financial crisis and many pundits are using this arbitrary anniversary to prognosticate the next great financial calamity. This week, collateralized loan obligations (CLOs) took their turn in the spotlight, cast as the villain most likely to bring the global economic system to its knees.

Make no mistake. Risk is elevated. This is particularly true for the broader corporate credit arena. Central banks responded to the global financial crisis by providing unprecedented amounts of liquidity, which fueled debt market growth and investor risk taking—as a percentage of GDP U.S. non-financial corporate debt is near the peaks seen in the tech bubble of the late 1990s and the housing bubble of the mid-2000s.

It is also true that much of the recent credit expansion has been in non-traditional categories, including senior loans, the underlying collateral of CLOs. However, gaining a comprehensive view of risk in this environment requires a deep understanding of the idiosyncrasies of the different instruments used to gain corporate credit exposure. As headlines and fear mongering rhetoric reverberate future doomsday scenarios caused by CLOs, panic is not the proper course of action. Below we offer our clients the following insight to help them most efficiently navigate the path ahead.

First and foremost, it is important to understand that CLOs are not some new, flashy financial instrument born out of current market exuberance—CLOs have been around since the late 1980s.

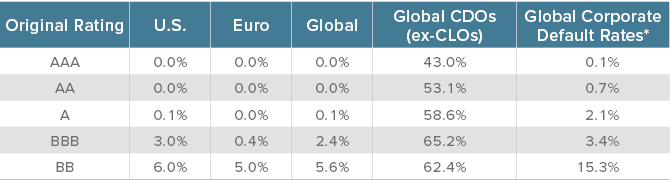

Since inception, AAA- and AA-rated CLO tranches never experienced a default or loss of principal, even during the depths of the financial crisis. As the chart below highlights, lower-rated tranches of CLOs have only experienced minimal long-term impairment rates over this same time period, faring much better than other corporate credit sectors of the same credit quality.

The Historical Track Record of CLOs

CLO Impairment Rate Comparison

Source: Barclays, Moody's *Global corporate default rate data based from 1983 to 2018.

Collateral: CLOs Provide Exposure to a Senior-Secured Asset Class

Senior loans, the underlying collateral of CLOs, are a large part of the reason why CLOs have delivered a track record of low impairment rates. Senior loans hold the highest rank in a borrower’s capital structure, making them senior to all other debt and stock, both preferred and common. In the event of a borrower’s bankruptcy or other liquidation scenario, senior loan obligations would be paid first, ahead of subordinated loans, bonds, preferred stock, or common equity. Furthermore, senior loans contain contractual provisions, known as covenants, that impose limits on what the borrower may do with the borrowed money.

However, it is important for investors to remember that despite the senior secured status of loans, the asset class still represents lending to companies that are below investment grade. Like other below investment grade allocations, nothing is guaranteed and issuer selection based on rigorous fundamental research is critical, especially in the latter stages of a credit cycle. For example, attention to detail in covenant packages, alluded to above, is of particular importance in today’s lending environment when making security selection decisions. Covenant packages, when measured overall in the asset class, have deteriorated in terms of their quality in recent years. While the implications are uneven across issuers, this is an enhanced risk for investors to chart course around when investing in CLOs.

Structure: Robust Protections that have been Tested through Time

In addition to the senior-secured status of their underlying collateral, CLOs have imbedded structural protections provided by a cash diversion mechanism of the CLOs. This mechanism is governed by Overcollateralization (OC) and Interest Coverage (IC) tests, and is triggered if there is meaningful deterioration in collateral performance from levels set at inception of the CLO.

Conceptually, Overcollateralization Tests require that the amount of senior secured loans held in the underlying collateral pool of a CLO has to exceed the amount promised to investors who purchase the debt tranches of the CLO by a certain percentage. Why does this matter? The levels of excess collateral in current CLOs would allow them to withstand the default and recovery experience of past credit cycles. For additional perspective, stress tests of a recent CLO showed that generating a principal loss in the BB tranche would require a constant default rate of 4.44% (assuming a 40% recovery rate) over the span of 8.5 years.

If any Overcollateralization or Interest Coverage Tests are failing, the CLO diverts interest and principal due to junior tranches to pay down senior tranches (or, purchase more collateral in certain cases) until such time that the covenants are back in compliance. These protections improve the resiliency of the more senior CLO debt tranches to default experience.

Revised Rating Agency Methodologies and Enhanced Regulatory Environment

Despite the relatively strong track record of CLOs through the crisis, the asset class was not immune from the sweeping regulatory changes and rating agency methodology revisions that followed in the wake of 2008. This means the CLO market has become stronger since 2008 from these important dimensions.

New U.S. regulations imposed after the financial crisis have reduced reliance on leveraged investors in the CLO market and influenced an improved risk profile via Volker Rule provisions. Real money investors such as pension funds, asset managers, and insurance companies, especially those from Asia, are larger holders of the asset class. Stable long-term investors currently represent a significant portion of CLO market participants.

This Risk in CLOs is Idiosyncratic, NOT Systemic

Despite the improved regulatory framework and the sector’s proven track record, CLOs are not for everybody. As standalone investments, CLOs are compelling for buy and hold investors like the insurance companies that have emerged as a significant presence in the CLO market. In addition, for multi-sector fixed income strategies with the appropriate structural and credit expertise, CLOs can be a compelling way to diversify a broader fixed income portfolio. However, in the context of multi-sector portfolios, CLOs can experience periods of pricing volatility in secondary markets. We witnessed this in December and CLOs have been slower to retrace spread widening relative to other risk markets.

It is also important for investors to understand that risk across the CLO asset class is not uniform—bad actors do exist and, like in any market, so does risk and so does reward. Given the nature of CLOs as a securitized asset class, we view the risk in CLOs as idiosyncratic and believe the systemic, fear mongering doomsday scenarios alluded to in the media are ultimately exaggerated.

This commentary has been prepared by Voya Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) changes in laws and regulations and (4) changes in the policies of governments and/or regulatory authorities. The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.