Flatlining at The New Neutral

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY

- The Federal Reserve’s pivot to patience in January has reduced the risk of monetary overkill and raises the odds that U.S. short-term interest rates will broadly flatline within PIMCO’s long-standing New Neutral range of 2%–3% for the foreseeable future. The 20 March Fed meeting validated this outlook.

- Meanwhile, low borrowing costs, populist pressures in many countries and the ascent from obscurity of Modern Monetary Theory all suggest that fiscal policy will become more activist in supporting demand and inflation over time.

- However, with global growth still “synching lower” and political “rude awakening” risks abundant, we remain cautious in our overall macro positioning while focusing on specific carry (yield) opportunities away from crowded corporate cash bonds.

- We favor agency and non-agency mortgage-backed securities (MBS), U.S. Treasury Inflation-Protected Securities (TIPS), financials and a select basket of high-yielding emerging market (EM) currencies, while being cautious on corporate credit and Italian and U.K. sovereign bonds. We are broadly neutral on duration and maintain a modest curve steepener in the U.S. In equities, we prefer high quality defensive growth.

Following roller coaster financial markets and the Fed’s pivot to patience since our previous gathering in early December, PIMCO’s investment professionals and the Global Advisory Board chaired by Ben Bernanke convened in Newport Beach in early March for our Cyclical Forum. We reassessed the macro outlook for the next six to 12 months and zoomed in on three key topics:

- While global growth has been “synching lower” in the last three months in line with our December thesis, what are the chances that China’s stepped-up stimulus finds traction and stabilizes or even turns around Chinese and global growth momentum in the course of this year?

- As regards monetary policy, are markets right to assume that the federal funds rate has peaked and the next move will be down, or is the Fed just pausing before resuming hikes? Relatedly, how significant is the Fed’s upcoming review of potential “makeup strategies” for past inflation undershoots?

- Third, what about trade and fiscal policies – how disruptive or constructive will they be? Is the trade war passé? And with Modern Monetary Theory (MMT) in focus and populism a force, is fiscal policy the new monetary policy when it comes to supporting growth and inflation?

Here are our conclusions and how we position on the back of them.

GLOBAL CYCLE: CHINA IS THE SWING FACTOR …

The slowdown of global growth over the past year despite massive fiscal stimulus in the U.S. and still-supportive monetary policies in the advanced economies illustrates that, more than ever, China is a key driver of the global cycle. The Chinese government’s deleveraging campaign, which weighed down business and property investment, and the negative fallout of the trade conflict with the U.S. contributed to a slump in global trade growth, which in turn dragged down business confidence and investment around the world, in particular in export-oriented economies in Europe, Asia and EM.

So far, there are few signs that the global trade cycle has bottomed (Figure 1), and we see global growth still synching lower in the near term. However, with China upping the ante on stimulus and a trade deal between the U.S. and China in the making, there is a good chance that global growth will stabilize or even pick up moderately later this year.

Source: Haver Analytics, CPB Netherlands Bureau for Economic Policy Analysis as of 31 December 2018

See CPB for country classifications: https://www.cpb.nl/sites/default/files/omnidownload/CPB-Background-Document-September2016-The-CPB-World-Trade-Monitor-technical-description_28.pdf

… AND MOVES FROM CREDIT “IRRIGATION” TO “FLOODING”

One reason for our cautious optimism on a bottoming of global growth later this year is the easing of global financial conditions since the Fed’s dovish pivot at the start of the year. Another is that China has recently stepped up the pace of fiscal and monetary easing.

True, much of China’s fiscal easing is directed at consumers and small businesses via tax cuts, the bulk of which may well be saved rather than spent. However, as is evident in the rebound in total social financing – the broadest measure of credit growth – since the start of the year, China’s policymakers appear to have shifted from, as one forum participant put it, carefully “irrigating” perceived future growth sectors of the economy to “flooding” the entire system in an effort to prevent a hard landing (Figure 2).

Source: U.S. Bureau of Economic Analysis, People’s Bank of China, Haver Analytics as of 31 January 2019.

China Growth Indicator is based on Fernald, Hsu, Spiegel. 2015. “Is China Fudging its Figures? Evidence from Trading Partner Data.” Federal Reserve Bank of San Francisco Working Paper.

China’s credit impulse is the year-over-year growth in economy-wide-debt flows as a percentage of GDP, smoothed. Economy-wide-debt flows are based on UBS calculations.

While the jury is out regarding both the size of the stimulus and the amount of economic traction it will get, our baseline view is that China’s growth, and with it global trade growth, will stabilize in the course of this year, enabling a soft landing of sorts for the global economy, albeit with further air pockets along the flight path.

THE FED EMBRACES THE NEW NEUTRAL …

The most consequential development for global markets since our December forum was the Fed’s pivot from projecting further gradual rate increases to adopting a patient, wait-and-see attitude on rates and signaling an end to balance sheet runoff later this year. As Fed speakers have explained over the past couple of months, the pivot to patience was triggered by three factors: tighter financial conditions in late 2018, the sharp slowdown in global growth, and the lack of consumer price inflation pressures despite a 50-year low in the unemployment rate.

"The Fed has now acknowledged that the current policy rate (a target range for the federal funds rate of 2.25% to 2.5%) may be at or close to neutral."

More broadly, the Fed has now acknowledged that the current policy rate (a target range for the federal funds rate of 2.25% to 2.5%) may be at or close to neutral, in line with our long-standing view of a New Neutral range of 2%–3% (Figure 3). Obviously, this assessment could change again in the light of incoming data, which inform the Fed’s view on underlying (unobservable) key parameters such as the neutral rate of interest (r*) or the natural rate of unemployment (u*). Yet, for now, the Fed appears to have embraced The New Neutral.

Source: Bloomberg, Federal Reserve Bank of New York, Holston, Laubach, and Williams, 2017, “Measuring the Natural Rate of Interest: International Trends and Determinants,” and PIMCO calculations as of 31 December 2018.

"We expect inflation pressures to remain subdued over the cyclical horizon despite a relatively tight labor market."

Looking ahead, we expect inflation pressures to remain subdued over the cyclical horizon despite a relatively tight labor market. Thus, even though financial conditions have eased since the beginning of the year and we see a good chance of sustained U.S. growth at around trend following a likely air pocket in the first quarter, we now expect the fed funds rate to broadly flatline at the current level for the foreseeable future. We see a relatively high hurdle to both rate hikes and rate cuts for the remainder of this year.

… AND EXPLORES THE BENEFITS OF MAKEUP

While the view that the Fed would keep rates steady for quite some time was relatively uncontroversial at our forum, the relevance of the Fed’s announced review of its monetary policy strategy later this year was more hotly debated. As explained by Chairman Powell and other Fed officials, the strategy review will focus on whether the central bank should aim at making up for shortfalls of inflation below target in times when policy is constrained by the effective lower bound for interest rates by aiming at overshooting the target in normal times.

One camp at our forum argued that the Fed has always emphasized that its 2% target was symmetric, allowing for moderate overshooting as well as undershooting, but that it would shy away from making a major commitment to move to “average inflation targeting” or another variant of “price-level targeting.”

The other camp argued that the new Powell/Clarida/Williams/Daly Fed appears to be serious about re-anchoring uncomfortably low inflation expectations at around the 2% target by aiming to overshoot 2% in normal times, and that this would require the signaling of a new, modified approach following the strategy review.

While the jury remains out, we expect any changes in the Fed’s framework to be evolutionary rather than revolutionary. In any case we would expect the Fed not only to tolerate but welcome a moderate inflation overshoot, should it occur.

TRADE CONFLICTS: NOT BOILING, BUT STILL SIMMERING

With the Fed shifting to neutral, China upping its stimulus and better prospects for sustained global growth, we agreed that the left tail for markets is defined by politics rather than the economy or monetary policy.

In particular, we felt that while markets have fully priced in a U.S.–China trade deal, they are underestimating the potential for a flare-up of trade tensions elsewhere. The USMCA deal between the U.S., Canada and Mexico intended to replace NAFTA faces significant challenges to pass Congress over the coming months, and President Trump may decide to withdraw from NAFTA in order to increase pressure on Congress to pass the deal.

Moreover, now that the Department of Commerce Section 232 report investigating whether autos and auto parts constitute a national security threat has been completed and submitted to the White House, the administration could well threaten or even go so far as to impose tariffs on auto and auto parts imports in order to create leverage in its broader trade negotiations with the EU and Japan. A deadline for White House action is 18 May, although that deadline could be extended.

"Even though a full-blown trade war is still unlikely to come to pass, we expect trade tensions to continue to simmer, leading to occasional bouts of volatility."

Even though a full-blown trade war is still unlikely to come to pass, we expect trade tensions to continue to simmer, leading to occasional bouts of volatility in markets over the course of this year. This argues for caution on risk assets but will also create opportunities when markets overreact.

FISCAL IS THE NEW MONETARY

Next to trade policy, another area where nothing should be taken for granted anymore is fiscal policy, for better or worse. Among the potential “rude awakenings” for investors that we highlighted in our Secular Outlook last May were a potentially much more expansionary fiscal policy in the future and a more radical populist backlash aimed at redistribution from capital to labor via taxes and regulation.

Both risks have become more real since, with more radical policy proposals in Europe and the U.S. to levy wealth taxes, increase marginal income and corporate tax rates, introduce universal basic income and break up large tech companies. Many of these potential policies would likely increase market volatility and challenge the valuations of risk assets.

We also discussed the recent ascent from relative obscurity of Modern Monetary Theory (MMT) and its implications. Some of its critics say that MMT is neither Modern, nor Monetary nor a Theory. Or, as one participant quipped at our forum, what is correct in this doctrine is not new, and what is new in it is not correct.

In a nutshell, proponents of MMT postulate that active fiscal policy should be used to target full employment, and that monetary policy should finance directly (via accepting an expansion of the monetary base) whatever deficit level fiscal policy chooses. Expansionary fiscal policy would thus automatically increase the money supply rather than the bond supply, and financing the deficit would never be a problem. And if inflation ever were to become a problem, the appropriate tool would be a contractionary fiscal policy that would force the central bank to reduce the money supply.

While we think that such a policy framework, which resembles the wartime and postwar era of fiscal dominance, is unlikely to become reality in the foreseeable future, the recent prominence of MMT in the public debate is symptomatic of a broader paradigm shift away from discussions of fiscal austerity to a new mainstream view that fiscal policy should become a more active tool to stimulate growth, counter the global savings glut and address rising income and wealth inequality. We’ll keep discussing this shift at our upcoming annual Secular Forum in May, but for now we conclude that rising support for a more active, expansionary fiscal policy should contribute to a steeper yield curve and upside risks to future inflation.

Investment implications

Financial markets have priced in the “synching lower” theme and central bank dovishness with a sustained move lower in global yields, while risk assets are generally back to or close to their early December levels. We continue to be concerned about the ongoing secular potential for “rude awakenings” and market disruption as the result of recession risks, shifts in the balance between monetary and fiscal policy, trade tensions and political populism. Therefore, we continue to think this is an environment in which it makes sense to stay fairly close to home in terms of top-down macro risk factors, to generate income without relying excessively on corporate credit, and to emphasize flexibility and liquidity in our portfolio construction, keeping powder dry to be put to use during periods of higher volatility and market dislocation.

LOOKING FOR A STEEPER CURVE AND WIDER BREAKEVEN INFLATION

We plan to be close to home on duration in light of the slower growth outlook and the Fed’s pivot driving the move lower in yields. While we think there is a good chance that the Fed is done hiking in this cycle, equally we also believe the market is premature in pricing in rate cuts.

On the yield curve, we expect to have a modest steepening bias. This is in line with our structural preference for curve steepeners and with our view that they offer the potential benefit of shielding portfolios if we are wrong and the downside macro risk and more Fed cuts are priced in, and in the upside event of stronger macro outcomes as we think the bar will be high for the Fed to flip-flop back to a more hawkish stance. Related, we think TIPS provide reasonably priced hedging against upside inflation risks. Even if the Fed’s discussion around various average inflation makeup proposals is unlikely to lead to significant changes in the framework, it reinforces the view that the Fed will be slow in responding to any upside inflation pressures.

PICKING UP CARRY AWAY FROM GENERIC CORPORATE CREDIT

On spread products, we will aim to generate income without relying on generic corporate credit, reflecting both bottom-up views and our concern about credit market structure and liquidity. While the baseline outlook for corporate credit looks fine, following the large growth of the market and increasingly crowded positioning in credit – which has not been matched by the sell-side’s balance sheet for corporate trading – we want to ensure that our portfolios are not overly exposed in the event of a sustained period of credit market weakness, and we actively seek to take advantage of the opportunities that such an environment would provide.

U.S. non-agency mortgages continue to be our preferred spread assets, given valuation, compensation for liquidity risk and seniority in the capital structure. We expect certain commercial and residential mortgage-backed securities from other jurisdictions will provide opportunities. U.S. agency mortgages also provide an attractive source of carry in our portfolios.

On corporate credit, we will focus on shorter-term bonds in companies where we see default risk as extremely remote. In addition, we continue to see financials as a sector offering attractive opportunities based on valuation. More broadly, while looking to be underweight generic corporate credit, we will seek to benefit from the high-conviction ideas of our global team of credit portfolio managers and analysts.

OPPORTUNITIES IN EM CURRENCIES

We do not see significant imbalances in developed market currency valuation and therefore don’t expect to have large G-10 currency positions. But we do expect to have a modest overweight to emerging market currencies in portfolios where this is consistent with the mandate, based on valuation and the view that currencies offer attractive relative value versus other EM assets.

CAUTIOUS ON ITALY, OVERWEIGHT CORE DURATION

We continue to favor an Italian sovereign underweight given valuation, the end of asset purchases, short-term political risks and the secular fragilities of the eurozone. We see European duration in the intermediate part of the curve as a relatively attractive source of carry – in spite of low yields – given the shape of the curve and the expectation that the European Central Bank (ECB) will find it a real struggle to raise rates from negative levels back to a zero rate in this cycle.

GOOD VALUE IN U.K. FINANCIALS

While uncertainties over Brexit remain, we continue to view an uncontrolled and chaotic Brexit as a low probability. In that context, we think there is a good case for being underweight U.K. duration on valuation grounds, and we see U.K. financials as offering good value, given that we think capital positions would prove robust even in the event of an uncontrolled Brexit.

EQUITIES: FOCUS ON HIGH QUALITY DEFENSIVE GROWTH

We expect equity volatility to remain a feature of markets, but it will be driven more by profit and global growth expectations rather than central bank liquidity conditions going forward. Indeed, the sharp policy turnaround that led the rebound in equities is now fully priced. We still favor a cautious, patient position in high quality defensive growth and reduced exposure to cyclical beta.

COMMODITIES: OIL ANCHORED IN RANGE, POSITIVE ON NATURAL GAS

Commodity markets have recovered from the late 2018 weakness, leaving valuations less compelling. We view OPEC’s production cuts, both voluntary and involuntary, as being sufficient to offset rapid production growth in the U.S., allowing the market to remain balanced. Until U.S. aggregate production growth no longer exceeds global demand growth, the oil market will likely remain anchored in the current range. Our outlook remains more positive on natural gas than current market prices due to increasing discipline of natural gas producers and steadily expanding demand and exports.

Regional economic forecasts

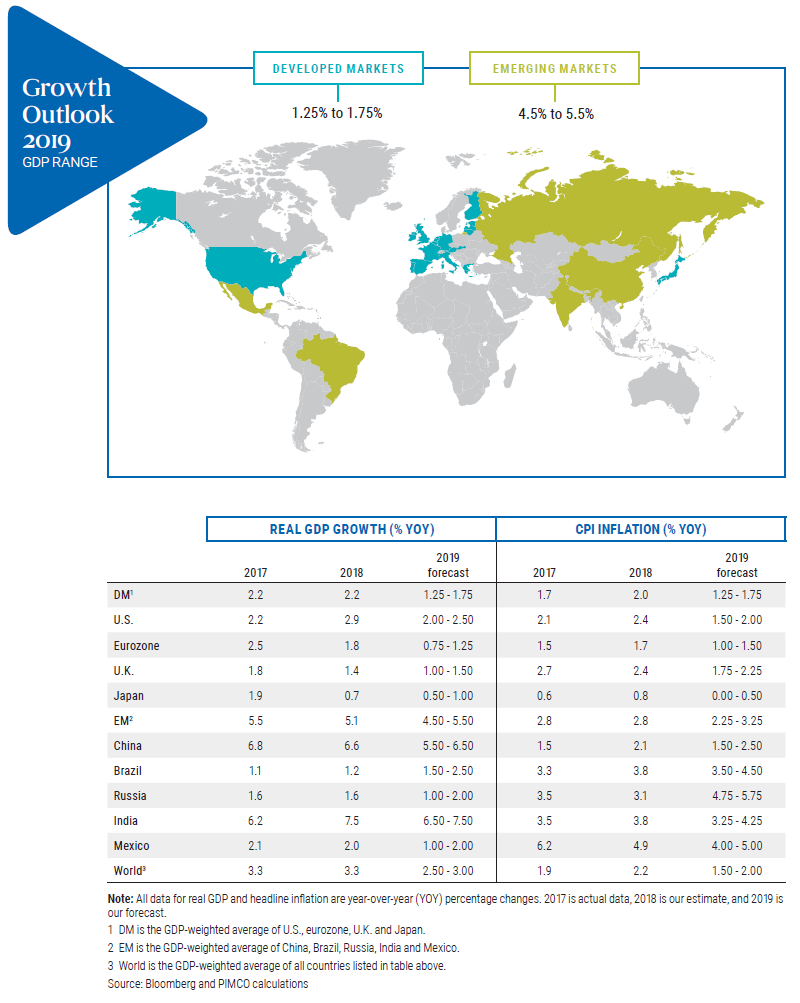

U.S.

We continue to expect real GDP growth to slow into a 2% to 2.5% range this year, from nearly 3% last year. Factors contributing to the deceleration include fading fiscal stimulus, the lagged effect of tighter monetary policy over the past few years, and headwinds from the China/global slowdown. Despite the stepped up pace of policy easing in China, the headwinds to U.S. growth are unlikely to abate until late in our cyclical horizon. Chinese easing and tightening cycles tend to affect U.S. growth with a lag, and based on these lags we estimate that recently announced fiscal and monetary easing won’t filter through to U.S. growth until late 2019 or early 2020.

While underlying growth is likely to slow during the year, the quarterly path is likely to be bumpy. A weak first quarter, currently tracking at around 0%, could be followed by a rebound in the second quarter as tax refunds should help consumer spending and exports to China should normalize.

Despite some pickup in wage pressures, we expect core consumer price inflation to move broadly sideways during this year. With growth slowing and inflation remaining below target, the Fed is now likely to remain patient and keep rates unchanged during the year.

EUROZONE

We see growth slowing to a trend-like pace of 0.75% to 1.25% this year as weak global trade is still exerting significant downward pressure on the economy and Italy is in recession. Meanwhile, domestic demand is likely to be relatively resilient, supported by moderate fiscal stimulus and solid real income growth. An improvement in global trade conditions through this year should contribute to a gradual reacceleration.

We expect a moderate pickup in core inflation, which has been stuck at around 1% for some time, during the year, reflecting firmer wage growth. In line with the ECB’s recently extended forward guidance, we expect policy rates to remain unchanged and do not foresee any change in the current reinvestment policy aimed at keeping the stock of assets unchanged over the cyclical horizon.

U.K.

We continue to think that a chaotic no-deal Brexit is a low probability event and that either a compromise between the EU and the U.K. can be found during a short extension of Article 50 beyond the end of March or a much longer extension will be agreed to, with another attempt at a deal with the new EU Commission and potentially a new U.K. prime minister.

Under this baseline, we expect GDP growth of 1.0% to 1.5% this year, modestly below trend, supported by higher government spending and consumer spending in line with real income growth of about 1.5%.

We see core CPI inflation stable at or close to the 2% target as import price pressures have now faded and domestic price pressures remain subdued. In the event of a soft Brexit by midyear, a rate hike by the Bank of England in the second half of the year would appear likely.

JAPAN

We expect modest growth in a 0.5% to 1% range this year, broadly unchanged from 0.7% in 2018. Headwinds from the sharp slowing of external demand should abate, while fiscal stimulus and a robust labor market are likely to support domestic demand.

With core CPI inflation expected to dip into negative territory (albeit due to temporary factors) around the middle of the year, we expect the Bank of Japan to keep its targets for short rates and the 10-year yield unchanged over our cyclical horizon.

CHINA

We see growth slowing into the middle of a 5.5% to 6.5% range from 6.6% in 2018, but stabilizing in the second half of the year as fiscal and monetary stimulus find some traction and a likely trade deal between the U.S. and China should support confidence. We expect fiscal stimulus of 1.5% to 2% of GDP supporting household spending, infrastructure and corporate investment. Inflation remains benign, and we look for another rate cut by the People’s Bank of China in addition to more reductions in banks’ reserve requirement ratios. CNY stability is well-anchored with a patient Fed and the understanding that this needs to be a component of the China-U.S. trade deal.

© PIMCO

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits