A V-shaped snap-back helped equities recover from the fourth-quarter selloff of 2018. The move reflected a stark change in mood from the pessimism that ruled during the previous period, yet the fundamental narrative for companies was largely unchanged.

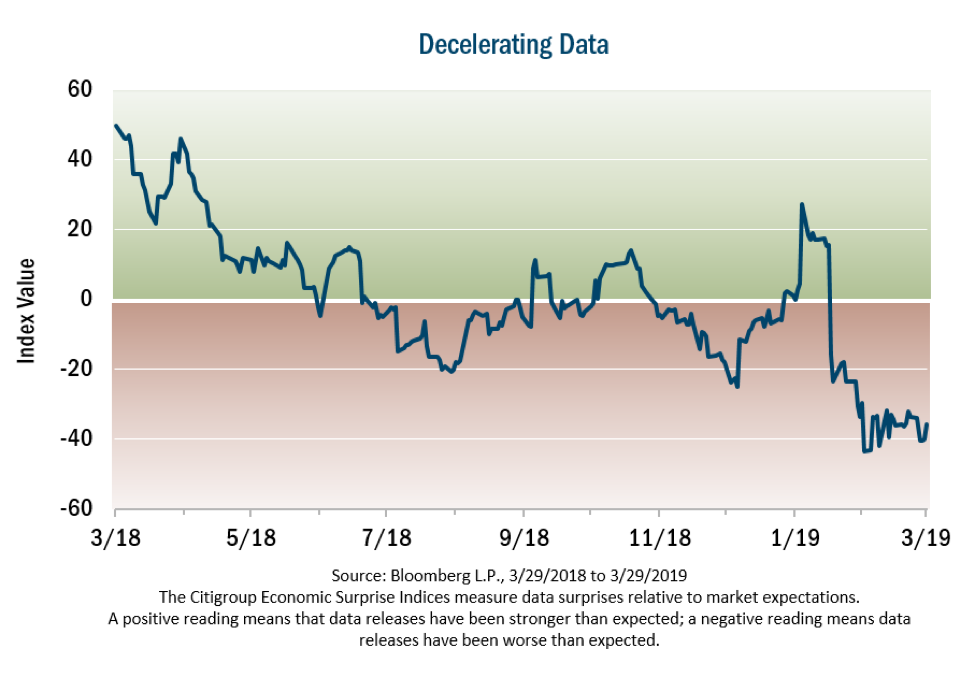

Earnings growth projections remained muted, and global trade tensions persisted. Data began to confirm earlier forecasts of a slowing economy, as shown in the Citi Economic Surprise index below. Even the Federal Reserve’s decision during the period to suspend its program of raising rates, which was cheered by investors, had been widely anticipated for months.

Risky Devotion to Emotion?

While the strong performance is welcomed, we remain frustrated by the persistence of what we see as a bear market in logic. Volatility of the past six months has been long on emotion but short on common sense.

The impact of emotion is driving many investors to pay too much attention to the short term and thus overlooking businesses with solid fundamentals and valuations. Instead of chasing an investment horizon of just a few weeks or months, we take the long view and are sticking to our time-tested 10 Principles of Value Investing™ when evaluating opportunities.

Taking the Long View

With uneven economic data and emotions running high, we think volatility is likely to persist in the broad indices over the next several quarters. But whether the ride is bumpy or smooth, eventually, we believe, perceptions and fundamentals will converge. And as always, our focus remains on the fundamentals.

For example, we continue to seek companies that can capitalize on opportunities even in changing economic conditions. That takes balance-sheet strength, which is likely to be a key differentiator in the quarters ahead, particularly given the significant runup in corporate debt.

The fact that we continue to find exceptional valuations 10 years into a bull run is a remarkable reminder of the value of a bottom-up approach. We remain unwavering in our efforts of finding these compelling opportunities and believe these are the type of companies that will thrive over the long run.

Disclosure:

Past performance does not guarantee future results.

Investing involves risk, including the potential loss of principal. There is no guarantee that any particular investment strategy will be successful. Value investments are subject to the risk that their intrinsic value may not be recognized by the broad market.

The statements and opinions expressed in this article are those of the presenter(s). Any discussion of investments and investment strategies represents the presenter’s views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. Any forecasts may not prove to be true. Economic predictions are based on estimates and are subject to change.

Definitions: 10 Principles of Value Investing™ consist of the following criteria for selecting securities: (1) catalyst for recognition; (2) low price in relation to earnings; (3) low price in relation to cash flow; (4) low price in relation to book value; (5) financial soundness; (6) positive earnings dynamics; (7) sound business strategy; (8) capable management and insider ownership; (9) value of company; and (10) positive technical analysis. Bear Market occurs when the price of a group of securities is falling or is expected to fall. Bottom-up is an investment approach that de-emphasizes the significance of economic and market cycles. This approach focuses on the analysis of individual stocks and the investor focuses his or her attention on a specific company rather than on the industry in which that company operates or on the economy as a whole. Bull Market occurs when the price of a group of securities is rising or is expected to rise.

©2019 Heartland Advisors heartlandadvisors.com

2019121