The U.S. Federal Reserve’s dovish turn pushes recession risks out to 2020, but we think it is premature to expect the next move to be an easing. Global cycle conditions are improving at the margin and inflation is still in the long-term pipeline.

Calm after the storm

It’s been an eventful few months. The S&P 500® Index narrowly avoided a bear market and bounced back strongly.Brexit is on a knife-edge,theChina/U.S.trade negotiations are still unresolved (although sounding more positive) and markets have shifted from expecting the U.S. FederalReserve (the Fed)to hike its funds rate several more times to now anticipating the next move as an easing.

Our cycle, value and sentiment investment process identified a buying opportunity for global equities in early January when market panic hit an extreme and became strongly oversold.

The oversold signals have now faded, and our process is holding us at a broadly neutral weighting on global equities. The process favors non-U.S. over the U.S. mostly because of valuation. The U.S. is expensive while Japan,Europe and emerging markets are close to fair value. Inflation pressures and the unwinding of central bank balance sheet expansion mean the cycle is a modest headwind for government bonds.

Paul Eitelman argues that the Fed pause will help extend the U.S. economic expansion. He sees signs that the data weakness of the past few months is turning around and thinks markets have overreacted by pricing in Fed easing.

Andrew Pease thinks European growth is set to improve during 2019 as the impact of one-off events fade and fiscal stimulus provides a tailwind. These one-offs include a rebound in German motor vehicle production,the thaw in the global trade war, calmer political conditions in Italy,t

Alex Cousley is looking forChina policy stimulus to provide a boost to the Asia-Pacific region. He thinks the data weakness in Japan is unlikely to be sustained but has increased the dovish bias at theBank ofJapan. The housing downturn is creating downside risks for Australia, but Alex thinks the hurdle for Reserve Bank of Australia easing is high with the prospect of fiscal stimulus ahead of the federal election in May.

Van Luu and Max Stainton think the U.S. dollar can stage a further rally once investors see that pessimism on the U.S. economy is overdone.

The recession probabilities from the U.S. business cycle index model estimated by Kara Ng have trended higher over the past couple of months. Kara thinks much of this is due to transitory factors such as the government shutdown, weather and trade-war uncertainties. We will be watching this model closely in the coming months to see whether recession probabilities recede once the transitory factors fade from the data.

Investment strategy outlook

Outlook 2019: the pause that refreshes

Global central banks have turned dovish, China stimulus is stronger than expected and trade-war tensions are easing. The cycle is becoming slightly more supportive for equities, but it’s late in the cycle, so we see the upside as limited.

The S&P 500® Index missed official bear market1 status by a whisker in late 2018, falling 19.8% between September 20 and December 24. It has since rebounded 18% (as of March 12), but the volatility highlights how skittish investors have become.

Markets are caught between the incoming data pointing to slower global growth and forward-looking factors that suggest improvement later in the year. We think a modest improvement in global cycle conditions is likely. This would be led by the U.S. Federal Reserve’s shift to a more dovish outlook and China’s moves toward policy stimulus. It will also be helped by rebounds from a series of one-off events that have constrained global growth. These include the recovery in European automobile production after the collapse caused by the European Union’s new emissions regime, a series of natural disasters that affected output in Japan and the recovery in U.S. output following the 35-day federal government shutdown in January.

It also seems likely that U.S./China trade tensions are heading for a form of détente, which will lift a constraint on global trade and business confidence.

The window of opportunity for equity markets looks limited, however. Capacity pressure is growing in the U.S. with the unemployment rate below 4%. Wage growth is already threatening corporate profit margins. It will eventually find its way into inflation and bring the Fed back into action. We expect a Fed funds rate hike late in the year, followed by another two hikes in 2020. This would take Fed policy into slightly restrictive territory, creating the risk of a recession either in late 2020 or during 2021.

Goldilocks2 seems to have returned for now and history tells us that global equities can continue to rally late in the cycle, even as the Fed tightens. We also know, however, that the less costly late-cycle mistake is to be defensive early rather than chase the last rally. We’re comfortable with a market weight allocation to equities as the first quarter wraps up. With inflation pressures gradually building, we prefer to reduce long-duration bond exposure.

Loose lips sink markets

Novice Fed chair Jay Powell received a crash course in the pitfalls of unscripted commentary last October. His remark that interest rates were “a long way from neutral” gave the impression he was planning many more rate hikes. This helped trigger the late-2018 market correction. The subsequent dovish messaging in early 2019 has been one of the key factors behind the market rebound.

The chart above shows the dramatic change in market views around the Fed’s decisions. Fed futures show where investors think the Fed funds rate is heading. In early November, this market was expecting the Fed to lift rates a further three times by the end of 2019. As of mid-March, Fed futures are now pricing in a 30% probability of a rate cut by the end of 2019 and a 70% probability of an easing by the end of 2020.

Our view is that the Fed futures market has over-reacted to some soft data and dovish Fed announcements. The U.S. economy is slowing as last year’s fiscal stimulus winds down. Gross domestic product (GDP) growth of 2.9% in 2018 was unsustainably strong. We’re expecting a slowdown to around 2.2% this year, a rate that is still well above the trend 1.8% growth rate. This means that price pressures should build, bringing the Fed back into action later in the year.

China getting more stimulus

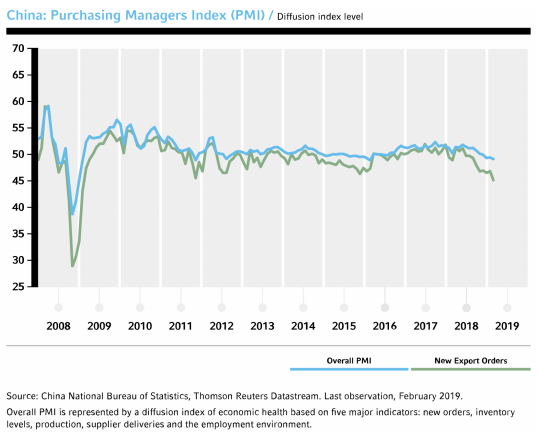

China’s economy continues to slow. The chart below shows that the manufacturing purchasing managers’ index (PMI) moved below the break-even level of 50 in December. The PMI index is being led lower by a dramatic decline in export orders as the effects of the trade dispute are felt.

The positive outcome is that the downturn is pushing authorities toward more aggressive policy stimulus measures. Data early in the year is always challenging to interpret due to the distortions caused by the timing of the Chinese lunar new year. Looking through the noise, there appears to have been a strong lift in bank lending and the broader total social financing measure over January and February.

Chinese authorities have announced a broad range of tax cuts, and it’s likely that local government spending on infrastructure projects will be ramped up over the next few months.

China responded to its last two economic downturns, in 2009 and 2015, with massive fiscal and credit stimulus. The response this time is unlikely to be as large given the concerns about high debt levels and financial stability.

Even so, stimulus measures are underway, which should provide support to both China and the global economy in the coming months.

Asset class preferences

Our cycle, value and sentiment investment process points to a broadly neutral view on global equities as of March 21, 2019.

- We have an underweight preference for U.S. equities, mostly driven by expensive valuation. The cycle has improved slightly with the Fed pause on rate hikes.

- We’re more positive on non-U.S. developed equities. Valuation in Japan and Europe is reasonable. Japan should benefit from an improving China outlook. Europe has fiscal stimulus and the potential for strong earnings-per-share growth in its largest sector, financials.

- We like the value offered by emerging markets equities. It is a beneficiary of a Fed rate hike pause, China stimulus and a potential thaw in the trade war.

- High yield credit is expensive and losing cycle support, which is typical late in the cycle, when profit growth slows and there are concerns about defaults.

- For government bonds, U.S. Treasuries offer reasonable value. Our models give a fair-value yield of 2.7% for the 10-year U.S. bond.

- German, Japanese and UK bonds are very expensive, with yields well below fair value. The cycle is a headwind for all bond markets as inflation pressures slowly build.

- We like real assets. Real estate investment trusts (REITs) are slightly cheap, while global listed infrastructure (GLI) and commodities are around fair value. Commodities typically benefit from late-cycle support as inflation pressures build. We expect GLI will benefit from its European focus as the region rebounds. Rising Treasury yields, however, are a headwind for REITs globally.

- The Japanese yen is our preferred currency. It’s significantly undervalued, can get cycle support as over-pessimistic growth expectations are revised higher and has contrarian sentiment support from large short positions by market speculators. The euro and British pound sterling are undervalued. The recovery in European economic indicators should support the euro. Sterling will be volatile around the Brexit negotiations but should rebound if a deal is agreed with Europe. It has more upside potential than the euro.

U.S. outlook: die another day

The global business cycle has been on a weakening trend for over a year. Chinese deleveraging, European politics and trade-policy uncertainty all played contributing roles. The U.S. economy, which was resilient to this malaise for the first 11 months of 2018, slowed abruptly in late December with regional manufacturing surveys and the Institute for Supply Management’s manufacturing index respectively logging their largest one-month decline since 2008. New orders and CEO confidence were crumbling at the start of 2019 on the back of tariffs, policy uncertainty and lackluster foreign demand. Left unchecked, a recession was possible. But in many ways this weakness sowed the seeds for a big policy response that should actually help extend the expansion—not forever, but the second-longest U.S. expansion on record lives to die another day3.

Circuit breakers

Three important policy responses have reduced the left tail risk for the U.S. economy.

- China: Alex Cousley writes in our Asia Pacific section that Chinese stimulus is ramping up in a way that is likely to stabilize economic growth there at/above 6% in 2019. Weak foreign demand has been a major factor behind the downgrade cycle for earnings estimates of large U.S. multinationals. We think Chinese policy stimulus should help stabilize earnings growth for the S&P 500 Index at around 5% in 2019.

- Trump: The U.S. aggressively pursued tariffs and other punitive measures against China over much of 2018 in an effort to extract concessions. But late in the year, with U.S. markets and business confidence sagging, President Donald Trump reversed course and now regularly professes confidence in his negotiators’ progress toward a deal. Politics aside, this step away from brinksmanship is a positive for corporate fundamentals and markets. We expect a trade deal will be announced in the second quarter of 2019, although the exact contours of that deal and the durability of any agreement remain hard to forecast with any degree of confidence.

- Powell: With the stress in financial markets, the slowdown in global growth, and importantly the U.S. economy’s participation in that slowdown in late December, Federal Reserve Chair Jerome Powell abruptly shifted course, stressing a much more patient approach to monetary policy. Powell’s thesis is that with core inflation failing to threaten the central bank’s 2% target, the Federal Open Market Committee can be patient to wait and see how the economy evolves in the coming months. This was a big change. Previously the Fed seemed happy to hike rates simply on an expectation that a strong economy and a tight labor market would gradually lift inflation over time. Now, Powell is requiring evidence that the actual inflation data accelerates before he is willing to hike rates beyond neutral. That’s particularly important because in the subsequent months, our tracking data for core PCE4 inflation has actually downshifted from a 2% run rate to 1.8% as of mid-March. With this “miss”, we think the current Fed pause can prove durable even in the early phase of a global growth recovery. That’s a tailwind for markets. We do think that the Fed will eventually come back to the table and hike once more this year. But we’ve pushed our baseline timing on that to December from September. A restrictive Fed and yield curve inversions are hallmark early warning signs for the end of an expansion. While we previously thought an inversion was possible in the first quarter of 2019, that now looks like a late 2019 story. With the normal lead times, this pushes our best thinking on the likeliest timing of the next recession out by six to nine months (into late 2020, or even 2021).

The U.S. economy looks like it is responding to Chinese stimulus, the Trump pivot and the Powell pause. There is tentative evidence that lower mortgage rates are stabilizing the housing market. And our high-frequency trackers of consumer and business confidence show early signs of an inflection higher in February, as reflected in the chart below. Meanwhile, U.S. consumer fundamentals continue to look robust, as declining unemployment rates and accelerating wage inflation buoy household income.

Strategy outlook

- Business cycle: Neutral to slightly positive. We are late cycle, and fading fiscal stimulus is likely to slow the economy relative to its breakneck pace from 2018. But with the Fed pause and a healthier outlook for global growth, we think the U.S. economy can deliver above-trend economic growth this year. We now forecast S&P 500 earnings-per-share growth of 5% in 2019, which is roughly on par with the consensus view of bottom-up equity analysts.

- Valuation: The year-to-date rally has pushed U.S. equity market valuations significantly higher. Assuming a mean reversion (lower) in corporate profit margins over the next 10 years, our risk premium estimates5 for the S&P 500 Index remain very unattractive.

- Sentiment: Our momentum signals lack direction as the tug-of-war from the sharp Q4 selloff and the sharp Q1 rally works its way through the data. The market which looked panicked at the end of 2018 now looks neither panicked nor euphoric.

- Conclusion: We maintain a small underweight preference for U.S. equities in global portfolios, solely on the back of their expensive valuations.

Eurozone outlook

Europe is set to benefit from a rebound in German automobile production, the end of the “yellow vest” protests in France, political stability in Italy and a dose of fiscal stimulus. The thaw in the U.S./China trade war will be a tailwind given the region’s reliance on exports to emerging markets.

A series of unfortunate events

The survey of forecasters by Consensus Economics expects 2019 European GDP growth of 1.3%. This is above-trend growth of around 1% but is a significant downgrade from a year ago when the consensus was predicting 1.8% growth in 2019. Europe has suffered from several one-off events that have depressed growth. These include the shift to a new emissions testing regime that caused a collapse in German automobile production, the political turmoil in Italy, Brexit uncertainty, the U.S./China trade dispute and the populist yellow vest/gilets jaunes protests in France.

It’s not clear yet whether these factors are temporary, meaning Europe should rebound during 2019, or whether there is a deeper underlying cause of weakness.

We’re in the ‘mostly one-offs’ camp and expect to see eurozone growth improve through the year. German motor vehicle production is already rebounding, a China trade deal is looking likely, a hard Brexit is becoming less likely and Italy looks less risky. Regarding the latter, Italian 10-year bond yields are nearly 120 basis points (bps) below their October 2018 peak as of mid-March.

Fiscal easing is likely to provide a decent tailwind, with the European Commission expecting that eurozone fiscal thrust will be 0.4% of GDP this year. The European Central Bank (ECB) has become more dovish, pushing out its guidance on the timing of the first rate rise to the end of 2019 (however, we don’t think a rate hike is likely until mid-2020 at the earliest) and outlining a new program of cheap bank funding to replace the TLTROs (targeted long-term refinancing operations) that mature next year. Furthermore, European households are in relatively good shape with falling unemployment and rising wages.

Strategy outlook

- Business cycle: The cycle should improve over the coming months as the impact of one-off events starts to subside. Exports to emerging markets are equal to nearly 10% of eurozone GDP, so the region will be a beneficiary of a thaw in the trade war.

- Valuation: Eurozone equity valuations are neutral while core government bonds are long-term expensive.

- Sentiment: Contrarian sentiment signals were heavily oversold in late December, but they have moved toward neutral with the subsequent equity market rebound. Equity price momentum is flat.

Europe has a track record of disappointing, so it’s worth thinking about the main risks.

- Italy moves back into crisis: GDP data confirm Italy was in recession during the second half of 2018, and GDP growth will probably be negative during Q1 of 2019. The political situation is volatile, and we can’t rule out new elections in 2019. The likely winner would be a Matteo Salvini-led center-right coalition controlled by the Lega political party. This could provide more political stability, but it could also trigger more clashes with the European Commission over fiscal policy.

- ECB makes a policy mistake and tightens too early: This risk has declined following the dovish turn at the March ECB Governing Council meeting. The key issue now is the leadership of the ECB when Mario Draghi’s term as president expires at the end of October. The moderately dovish Finn (and former governor of the Finnish Central Bank) Erkki Liikanen appears the favorite to replace him, but the appointment of Jens Weidman, head of Germany’s Bundesbank, would signal a hawkish shift.

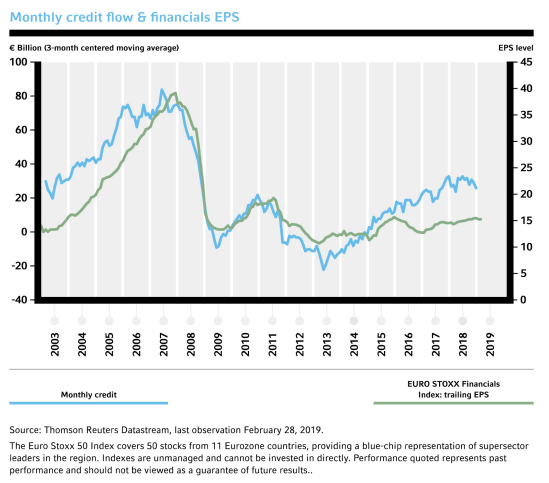

- Credit growth remains lackluster: The weakness in credit flows over the past few months is a concern (see the chart below), both from the aspect of earnings-per-share (EPS) growth in the largest equity sector, financials, and the near-term outlook for economic activity. Continued weak credit growth will indicate deeper eurozone malaise. We will be tracking monthly credit flows closely.

- Trump imposes tariffs on European motor vehicles: President Trump has had a report on his desk since Feb. 17 from the U.S. Commerce Department that probably recommends a 25% motor vehicle tariff. He has 90 days (until May 18) to announce a decision, and we believe a decision to implement tariffs seems unlikely.

- Hard Brexit: This would affect exports, supply chains and confidence. It’s looking less likely, but the UK political situation is very unpredictable.

Asia Pacific: stimulus trumps trade

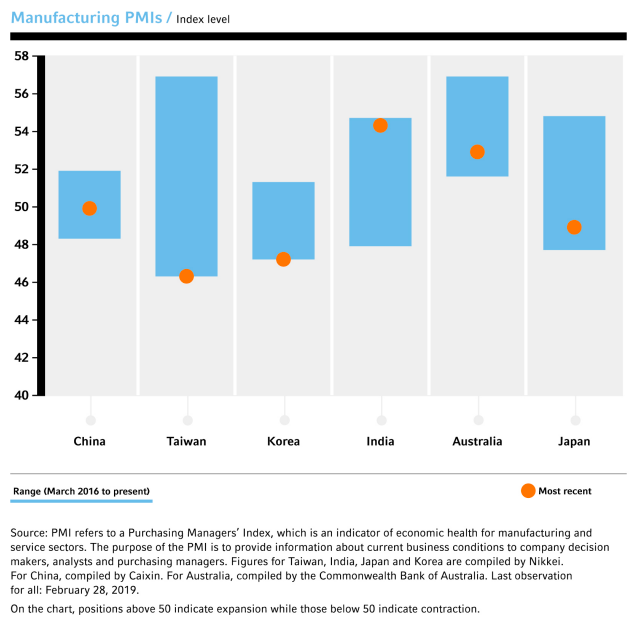

Chinese stimulus is starting to take hold, which will provide a boost to the region. We expect solid growth in India and above-trend growth for the Japanese economy. Equities are fairly valued, and we have confidence that 2019 earnings will meet market expectations. While we were never of the view that trade tensions would significantly derail growth, it is encouraging nonetheless that the risks are reducing.

The Asia-Pacific region is set to benefit from Chinese policy stimulus. We think emerging Asian equities should deliver around 10% earnings growth for 2019. Japanese economic activity has been disappointing, but we think the big downgrade to industry consensus earnings expectations is too pessimistic. Looking at risks, we are closely watching the Indian election in April and the raising of the value-added tax (VAT) rate in Japan that’s scheduled for October.

Let’s begin with China, where we are becoming more constructive on the economy. In our 2019 outlook, we said the economy should be able to deliver GDP growth of 6%. Recently announced stimulus measures (including the cutting of the VAT rate) provide upside support to this forecast.

We expect to see significant equity flows into the region following global index provider MSCI’s decision to increase the weighting of mainland China shares in its global benchmarks. This change could see up to $70 billion of net buying to mainland Chinese shares over the year. There will also be money flowing into Chinese bonds, as Chinese government bonds are added to the Bloomberg Barclays Global Aggregate Index, which will occur over a 20-month period beginning in April.

Indian growth should remain solid, albeit slightly below the pace set in 2018. The upcoming election will be a watchpoint, with published opinion polls in India predicting incumbent Prime Minister Narendra Modi’s coalition will secure the highest number of seats, though short of a majority. Election uncertainty is likely to be a headwind to investment, which has been the most disappointing component of economic growth over the past year. The Reserve Bank of India has followed the global shift toward more accommodative policy.

The growth outlook for South Korea and Taiwan has slipped a bit, in our opinion, but should remain positive through 2019. Our expectation of stabilizing Chinese growth will be supportive. The South Korean economy will also likely benefit from a more accommodative central bank—though, we don’t expect further funds rate hikes by the Bank of Korea this year—and an increase in government social spending.

Japanese economic data has been disappointing, with the economy having contracted twice in the last four quarters. We maintain a constructive outlook and expect slightly above-trend growth (though, trend growth is very low in Japan, given demographic dynamics such as a declining population). While inflation remains tepid, there are anecdotal signs of it rising, particularly in food and services (due to the extremely tight labor market). The big hurdle for the Japanese economy this year is going to be the increase of the VAT rate scheduled for October. The disappointing data, weak inflation pulse and VAT increase should keep the Bank of Japan on hold through the rest of the year.

The outlook for Australia has deteriorated over the past couple of months as the downturn in the housing market has weighed on economic activity. The Reserve Bank of Australia (RBA) has wanted to see prices fall from very elevated levels, so we are unsurprised to see the RBA remaining calm. The market is pricing one rate cut by the end of the year. A rate cut seems unlikely, in our view, given the strength of the labor market.

The battle between the tailwinds of potential fiscal stimulus and accommodative monetary policy and the headwinds of slowing population growth and a slowing housing market continues to play out in New Zealand. As with the RBA, we do not expect the Reserve Bank of New Zealand to hike rates this year. Foreign demand, particularly in the region, will remain positive.

Risks around the trade war, in our opinion, have eased. Regional politics still pose some risk, along with the increase in the consumption tax rate in Japan.

Investment strategy

For Asia-Pacific regional equities, we assess business cycle, value and sentiment considerations as follows:

- Business cycle: We are becoming more constructive on the region, underpinned by increasing signs of Chinese stimulus.

- Valuation: Despite the strong start to the year, we are not seeing many signs of stretched valuations. Chinese mainland shares stand out as attractively valued, while Japanese valuations are close to fair. We see New Zealand equities as less attractively valued than Australian equities.

- Sentiment: Investment flows into the region are going to be boosted by extra weight that MSCI is giving to Chinese A-shares equities. Anecdotally, it also appears that more investors are becoming interested in developing Asia6.

- Conclusion: Within the region, we maintain a preference for emerging Asia over developed, underpinned by solid underlying growth and the benefits of Chinese stimulus.

Currencies: residual dollar strength ahead

As the U.S. Federal Reserve shifted from a tightening bias to its current “wait and see” mode, the U.S. dollar treaded water in Q1. However, other central banks also turned more dovish, which should lead to a final leg up in this U.S. dollar bull market.

Six weeks can be a long time in financial markets and central bank policy. Between the December monetary policy meeting, when the U.S. Federal Reserve raised interest rates for the fourth time in 2018, and its decision to hold rates steady on January 30, 2019, the central bank did a complete 180-degree turn. After strongly indicating in December that interest rates would have to rise this year, the most recent statement removed references to further gradual increases and noted that inflationary pressures are muted. The implication could not be clearer: Fed policy is on hold for the foreseeable future.

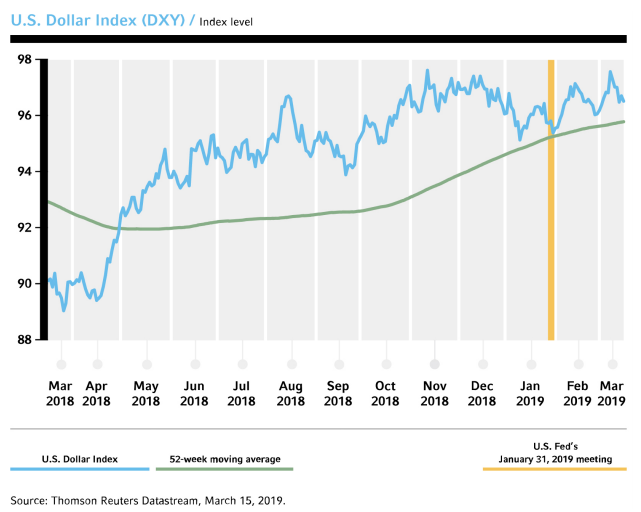

Currency and bond markets had sniffed out that dovish pivot by the Fed, selling the U.S. dollar heading into the policy meeting and bidding up the prices of bonds. Market participants in aggregate seem to believe the Fed is done hiking rates for the entire cycle. With markets currently pricing a chance of rate cuts this year, one could be forgiven for thinking that the dollar bull run has ended. Several times in recent months, the U.S Dollar Index (DXY)7 could not overcome resistance at 97.7 (see chart below), making it potentially vulnerable to a larger setback.

However, we believe that pessimism around the U.S. economy is overdone and we expect another leg up in DXY that could take it to 98, possibly to 100, before its bull run ends for this cycle. Our baseline outlook is that economic growth will stabilize and a tight U.S. labor market, coupled with accelerating wage inflation, will exert further upward pressure on consumer prices. Meanwhile, the European Central Bank (ECB) and the Bank of Japan (BoJ) have also become more dovish, weighing on the euro and the yen.

Other major currencies

Euro (EUR) As the budget crisis in Italy faded into the background, new factors weighing on the euro have emerged. Data flow for eurozone growth and inflation has been weak in early 2019. Some of the softness in economic activity was driven by idiosyncratic shocks that are now in the rearview mirror. For example, changes in emissions standards temporarily impacted German auto production. The impact of these transitory factors should fade over the coming months. However, muted inflation in the eurozone allowed the European Central Bank (ECB) to rule out interest rate increases for all of 2019.

All this keeps the euro under pressure in the short term, although cheap valuation of the currency probably limits the downside. We believe that buyers of the euro will re-emerge if the EUR/USD exchange rate touches 1.10 from 1.13 as of March 15, 2019.

UK pound sterling (GBP) As of March 16, the pound has been the strongest major currency in 2019. The appreciation of sterling this year has been driven by increasing optimism about an imminent benign Brexit outcome. On March 12, Prime Minister Theresa May’s deal with the European Union to enter an orderly transition period was rejected by the British House of Commons for the second time. However, on the following two days a majority in the UK parliament voted against a no-deal Brexit and in favor of postponing the departure date from March 29 to June 30. A delay on its own just moves the no-deal cliff edge a few months back. Ongoing Brexit uncertainty is detrimental to the British economy, and we can already see its impact in the data. Corporate confidence is low, which prevents businesses from investing. The consumer is pessimistic, slowing demand for durables like houses and cars.

For the sterling rally to live on, we need either a deal to pass in the next few weeks or the discussion to shift toward a softer Brexit/people’s vote.

Japanese yen (JPY) The yen is an attractively valued currency that we like for its diversification properties. As of February 28, 2019, the yen was 9% cheap vis-à-vis the U.S. dollar on the purchasing power parity measure8. If equity markets sell off, we believe that the yen will be the best safe-haven currency. It is traditionally a defensive asset, due to its net foreign creditor position, which causes repatriation of capital during times of crisis. The defensive nature of the yen is likely to be compounded by its low carry. During good times, investors engage in so-called carry trades where they buy high-yielding currencies like the Australian dollar and use the yen as a funding currency. Unwinding of carry trades during bad times would give the yen a major boost, in our view.

We would stay long yen or increase our allocation when the exchange rate versus the U.S. Dollar weakens toward 114 (from 111.4 as of March 15, 2019).

Quantitative modeling insights

On the cusp

The U.S. equity bull market celebrated its 10-year anniversary on March 9, and the U.S. economic expansion could become the longest in history by June 2019. The natural question around such milestones is to ask, “How much longer?” The Business Cycle Index (BCI) model, which uses a range of economic and financial variables to estimate the strength of the U.S. economy and to forecast the probability of recession, is on the cusp of risk-on versus risk-off. Short-term risks are still low, but the BCI model estimates the probability of recession in the next 12 months is around 30%—right on top of the warning threshold for leaning out of risky assets.

Some weakness in U.S. consumer spending and the labor market since December 2018 raised BCI recession risk in the last couple of months. However, the weaker data was likely driven by transitory factors such as the partial U.S. federal government shutdown, unusually cold weather and uncertainty with trade-war negotiations. Going forward, the tight labor market with rising wages should support a healthy consumer. Offsetting the weaker economic data was the dovish shift in Fed forward guidance since January 2019. With the Fed no longer raising interest rates at a quarterly pace, financial conditions loosened, and the rate of yield curve flattening slowed, which eased some BCI recession risk.

How long the economic expansion can continue, from the point of view of the model, depends on sustaining a Goldilocks level of growth—hot enough to avoid a negative confidence spiral, but cold enough for accommodative monetary policy. If consumers and businesses become pessimistic, spending and hiring could slow, raising BCI recession risk. If the Fed fears overheating, then restrictive monetary policy could tighten financial conditions and invert the yield curve, also raising BCI recession risk. The elevated 12-month recession risk reflects the late-cycle balancing act, where there’s less room for error.

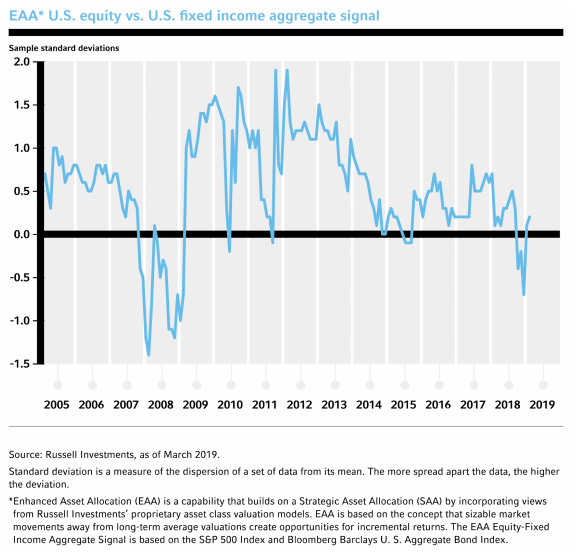

Thinking positive (barely)

After a drop in December, equity markets bounced back in early 2019. For a few months at the end of 2018 our Equity-Fixed model dipped below zero in response to the market’s momentum. The model shows an improvement since then along with the

After a drop in December, equity markets bounced back in early 2019. For a few months at the end of 2018 our Equity-Fixed model dipped below zero in response to the market’s momentum. The model shows an improvement since then along with the general market trend. It is time to go back to thinking positively about equities but there are still some macroeconomic concerns in the background.

Within our cycle, value and sentiment investment framework we make the following overarching assessments based on our quantitative models.

- Business cycle: We see signs of late-cycle woes, but otherwise the model indicates low probability of recession in the very near term.

- Valuation: After the year-end 2018 market selloff, the Fed model, which compares the equity yield to the 10-year U.S. Treasury yield, signaled equities as more attractive, but that preference has since faded.

- Sentiment: The Momentum model’s signal has stabilized to neutral after the late-2018 selloff.

Moving into the second quarter of 2019, the Equity-Fixed model’s signal is slightly above-neutral for equities, which suggests a mid-single-digit return on equities for 2019.

IMPORTANT INFORMATION

The views in this Global Market Outlook report are subject to change at any time based upon market or other conditions and are current as of March 21, 2019. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Keep in mind that, like all investing, multi-asset investing does not assure a profit or protect against loss.

No model or group of models can offer a precise estimate of future returns available from capital markets. We remain cautious that rational analytical techniques cannot predict extremes in financial behavior, such as periods of financial euphoria or investor panic. Our models rest on the assumptions of normal and rational financial behavior. Forecasting models are inherently uncertain, subject to change at any time based on a variety of factors and can be inaccurate. Russell believes that the utility of this information is highest in evaluating the relative relationships of various components of a globally diversified portfolio. As such, the models may offer insights into the prudence of over or under weighting those components from time to time or under periods of extreme dislocation. The models are explicitly not intended as market timing signals.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

The Business Cycle Index (BCI) forecasts the strength of economic expansion or recession in the coming months, along with forecasts for other prominent economic measures. Inputs to the model include non-farm payroll, core inflation (without food and energy), the slope of the yield curve, and the yield spreads between Aaa and Baa corporate bonds and between commercial paper and Treasury bills. A different choice of financial and macroeconomic data would affect the resulting business cycle index and forecasts.

Investment in global, international or emerging markets may be significantly affected by political or economic conditions and regulatory requirements in a particular country. Investments in non-U.S. markets can involve risks of currency fluctuation, political and economic instability, different accounting standards and foreign taxation. Such securities may be less liquid and more volatile. Investments in emerging or developing markets involve exposure to economic structures that are generally less diverse and mature, and political systems with less stability than in more developed countries.

Currency investing involves risks including fluctuations in currency values, whether the home currency or the foreign currency. They can either enhance or reduce the returns associated with foreign investments.

Investments in non-U.S. markets can involve risks of currency fluctuation, political and economic instability, different accounting standards and foreign taxation.

Bond investors should carefully consider risks such as interest rate, credit, default and duration risks. Greater risk, such as increased volatility, limited liquidity, prepayment, non-payment and increased default risk, is inherent in portfolios that invest in high yield (“junk”) bonds or mortgage-backed securities, especially mortgage-backed securities with exposure to sub-prime mortgages. Generally, when interest rates rise, prices of fixed income securities fall. Interest rates in the United States are at, or near, historic lows, which may increase a Fund’s exposure to risks associated with rising rates. Investment in non-U.S. and emerging market securities is subject to the risk of currency fluctuations and to economic and political risks associated with such foreign countries.

The S&P 500, or the Standard & Poor’s 500, is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ.

Performance quoted represents past performance and should not be viewed as a guarantee of future results.

Indexes are unmanaged and cannot be invested in directly.

Source for MSCI data: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

The MSCI All Country World Index is a market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. The MSCI ACWI is maintained by Morgan Stanley Capital International, and it is comprised of stocks from both developed and emerging markets.

The Citigroup Economic Surprise Indices are objective and quantitative measures of economic news. They are defined as weighted historical standard deviations of data surprises. A positive reading of the Economic Surprise Index suggests that economic releases have on balance been beating industry consensus. The indices are calculated daily in a rolling three-month window.

Copyright© Russell Investments 2019. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

© Russell Investments Group, LLC. 1995-2019.All rights reserved.

UNI-11446

1 A bear market is a condition in which stock prices fall 20 percent or more from recent highs amid widespread pessimism and negative investor sentiment.

2 Goldilocks defines an economy that is not too hot or cold; in other words, one that sustains moderate economic growth and has low inflation, which allows a market-friendly monetary policy.

3 This analogy refers to the 2002 James Bond film, Die Another Day.

4 PCE refers to personal consumption expenditure inflation, which is a measure of the change in prices of goods and services purchased by consumers throughout the economy.

5 Risk premium is the expected return on equities relative to cash or another safe asset like government bonds.

6 Developing Asia includes all of the countries in the continent of Asia except for the Middle East, and excluding the advanced economies in Asia, which are classified as Japan, Singapore, Hong Kong, South Korea and Taiwan.

7 The U.S. Dollar Index (DXY) is a measure of the value of the United States dollar relative to a basket of foreign currencies, often referred to as a basket of U.S. trade partners' currencies. The index goes up when the U.S. dollar gains "strength" (value) when compared to other currencies.

8 Source: Organization for Economic Co-operation and Development (OECD), as of March 15, 2019.