Improving regional connectivity

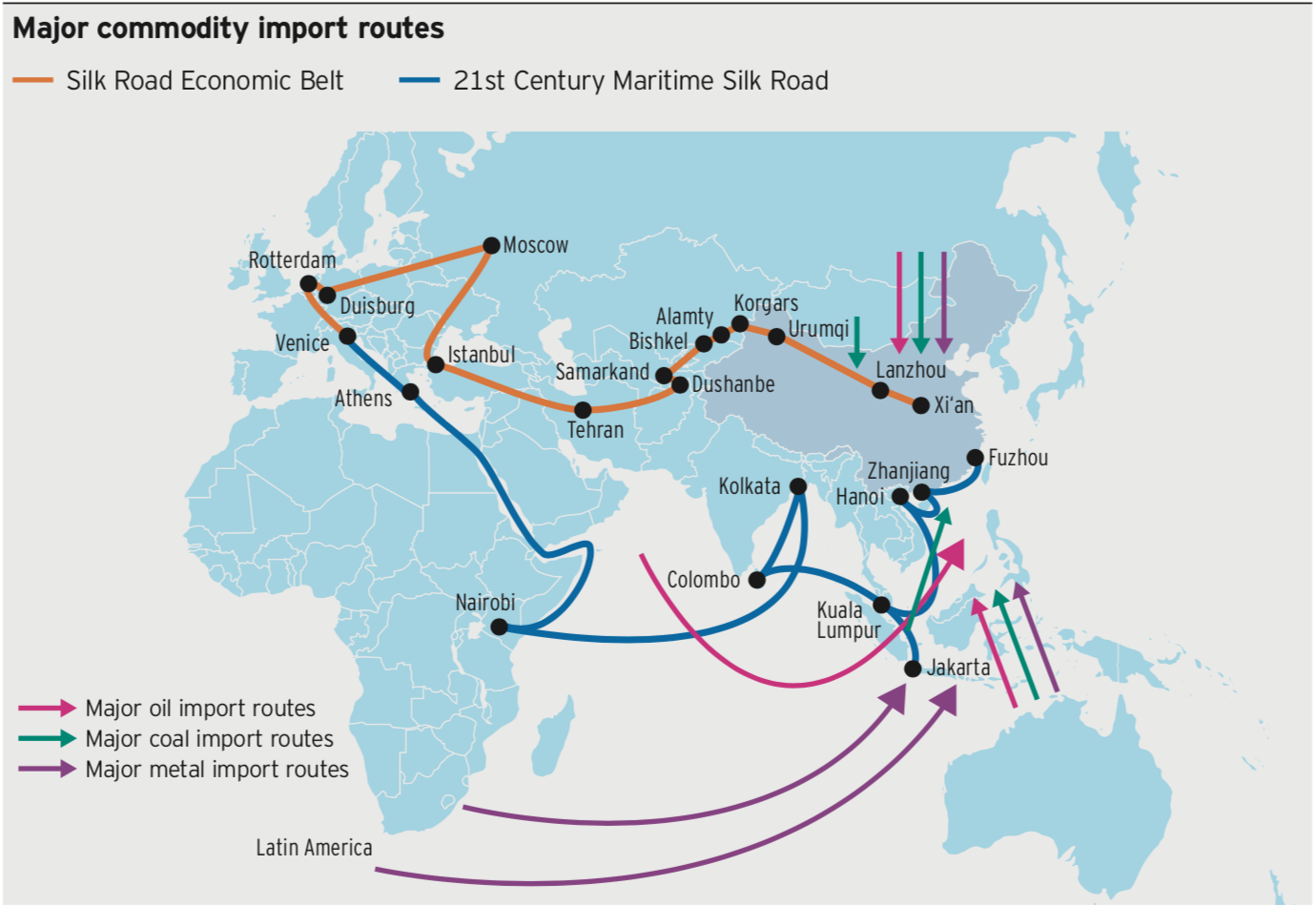

China’s Belt and Road Initiative (BRI), which aims to improve China’s connectivity with Africa and Europe along the former land and maritime silk roads, is expected to generate high levels of infrastructure spending, improve regional integration and promote economic growth. Chinese State Owned Enterprises (SOE), construction and building material companies, and commodity producers will likely be the primary beneficiaries of increased capital expenditure. We believe regional energy and metal and mining companies that take advantage of increased traffic and fixed asset investment will likely outperform their global peers. There is some potential for maritime supply route disruption for coal and bauxite, as increased continental freight capacity may present more efficient alternatives.

Potential opportunities created in infrastructure and energy related sectors

China’s BRI encompasses 84 countries, around 67% of the world’s population, over 36% of global gross domestic product and 38% of world trade.1 Invesco Fixed Income expects China to invest between USD150 to USD200 billion per year in major infrastructure projects to improve communication channels across countries ranging from rail, roads, bridges, ports and pipelines to telecommunication equipment, including fiber optic cables. These major investments are expected to initially benefit the metals and mining and building material sectors but will also likely spur increased energy consumption as regional trade expands. They may also disrupt existing commodity supply routes as alternative freight capacity becomes more economically viable.

In addition to infrastructure development, the BRI comprises strategic energy supply routes for major oil producers, including Saudi Arabia (10% of global supply), Iraq (5%), Iran (3%), Kuwait (3%), Emirates (3%) and Russia (10%), and natural gas producers, including Russia (17% of global production), Iran (6%) and Qatar (5%).2 The protection of regional energy supplies via China’s developing military presence along Middle East and South Asian routes may support Asian regional growth potential in the coming years. According to the International Monetary Fund, Asia is estimated to account for around two thirds of global growth in 2018, representing the world’s most dynamic region.3

The BRI may also further the development of existing supply routes. For example, while China currently imports thermal coal primarily from Australia, Indonesia, Russia and Mongolia, the development of rail infrastructure may reduce bottlenecks in continental freight capacity. This could favour coal production from Mongolia and Russia at the expense of supplies from Indonesia and Australia.

Metals and mining industry a likely beneficiary

Increased infrastructure spending is expected to benefit the metals and mining industry, especially steel, aluminium and copper producers. China accounts for 52% and 59% of global steel and aluminium production, respectively, and is expected to be the primary beneficiary of increased capital spending.4 Other countries likely to benefit include Australia and Brazil (iron ore), Chile and Peru (copper ore) and Australia, Guinea, and Brazil (bauxite ore used in aluminium production).5 As rail infrastructure develops, bauxite may experience a partial supply shift in favor of continental producers such as Kazakhstan and Russia, each currently accounting for approximately 2% of global production, at the expense of maritime suppliers, such as Australia and Brazil, currently accounting for 28% and 12% of global production, respectively.5

Revival of silk road may create investment opportunities

We believe China’s BRI, which aims to revive the historic Silk Road path traveled by

Italian merchant and explorer Marco Polo, could accelerate and strengthen economic growth across East Africa, the Middle East and Europe. While regional commodity companies operating in the metals and mining and energy sectors are likely to benefit most from increased infrastructure spending and regional trade, cheaper continental commodity supply routes could disrupt traditional maritime suppliers, generating potential opportunities for outperformance in corporate credit investments among land-based commodity suppliers.

Risks we are monitoring

While offering potentially attractive investment opportunities, the development of the BRI will likely rely heavily on China’s economic growth and financial conditions. A significant growth slowdown in China could reduce capital spending and delay major infrastructure projects. The changing geopolitical landscape as China expands its regional influence, may also generate periods of diplomatic instability. In addition, unrestrained capital investments might result in unsustainable sovereign leverage and fiscal tightening, eventually leading to debt restructurings, as underlined by the Maldives’ request to China in January 2019 to reorganize its accrued BRI debt. Nevertheless, we believe a balanced approach should allow significant development in regional trade and investment, while potentially fostering regional security.

Source: Invesco, as of Jan. 31, 2019. For illustrative purposes only.

1 Source: World Bank, Belt and Road Portal (yidaiyilu.gov.cn), Invesco, data as of Dec. 31, 2018.

2 Source: Oil production: Bloomberg L.P., Dec. 31, 2018. Natural gas: British Petroleum, Dec. 31, 2018.

3 International Monetary Fund, Regional Economic Outlook: Asia Pacific, May 2018.

4 World Steel Association, International Aluminium Institute, Dec. 2018.

5 Source: World Steel Association, International Aluminium Institute, Dec. 2018.

Investment risks

– Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

-

– Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

-

– The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

-

– Investments focused in a particular industry or sector are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

-

– Investing in securities of Chinese companies involves additional risks, including, but not limited to: the economy of China differs, often unfavorably, from the U.S. economy in such respects as structure, general development, government involvement, wealth distribution, rate of inflation, growth rate, allocation of resources and capital reinvestment, among others; the central government has historically exercised substantial control over virtually every sector of the Chinese economy through administrative regulation and/or state ownership; and actions of the Chinese central and local government authorities continue to have a substantial effect on economic conditions in China.

-

- The performance of an investment concentrated in issuers of a certain region or country is expected to be closely tied to conditions within that region and to be more volatile than more geographically diversified investments.

FOR PUBLIC USE ONLY

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GARUNTEE

All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. This is not to be construed as an offer to buy or sell any financial instruments and should not be relied upon as the sole factor in an investment making decision. As with all investments there are associated inherent risks. This should not be considered a recommendation to purchase any investment product. This does not constitute a recommendation of any investment strategy for a particular investor. Investors should consult a financial professional before making any investment decisions if they are uncertain whether an investment is suitable for them. Please obtain and review all financial material carefully before investing. Past performance is not indicative of future results. This does not constitute a recommendation of the suitability of any investment strategy for a particular investor. The opinions expressed are those of the author, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Invesco Advisers, Inc. is an investment adviser; it provides investment advisory services to individual and institutional clients and does not sell securities. Invesco Distributors, Inc. is the US distributor for Invesco’s retail products and private placements. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

Read more commentaries by Invesco