The Function of the Form: What Advisors Need to Know About the New Form 1040

Are investors paying too much in investment taxes? Can you help them create better after-tax outcome? Without a basic understanding of the individual tax forms, it can be challenging to critically analyze. Given this is the first tax year to reflect the Tax Cut and Jobs Act, there are a few changes advisors should understand to better prepare for reviewing clients and prospects tax situations relative to their investments. Understanding these changes will allow you to identify problem areas or opportunities that can add meaningful value to your practice.

What changed?

Forms 1040A and 1040EZ have gone the way of the dodo bird. The IRS has promoted its simplification of Form 1040, with all taxpayers reporting basic information on the new "postcard-sized" 1040.

But most taxpayers with any investment income, capital gains, business income or other type of income beyond very basic wage income also will have the pleasure of completing the new Schedule 1 (see below).

How to help clients with investment taxes

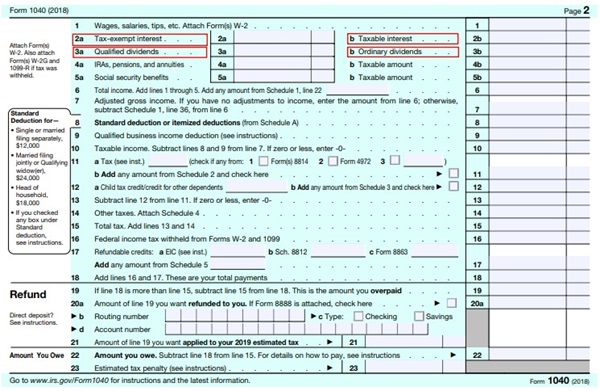

To analyze the impact of taxes for your clients, you first need to know their marginal tax rate (which is the tax rate on the next dollar earned) and effective (average) tax rate. Then go through page two of the new Form 1040.

Line 2a: Tax-exempt interest. Is the client's marginal tax rate so low that municipal bonds may not make sense? Evaluate the tax-equivalent yield of municipal bonds versus taxable bonds.

Line 2b: Taxable interest. Conversely, is the client's marginal tax rate enough to erode after-tax income? Clients always want to focus on the yield of a given investment and often fail to consider the after-tax yield.

Line 3a: Qualified dividends. Qualified dividends are taxed at long-term capital gains rates. Does the client's situation require generating income? Perhaps a strategy focusing on capital appreciation or a similar tax-smart approach focusing on capital appreciation versus high dividends is warranted.

Line 3b: Ordinary dividends. Sometimes referred to as nonqualified dividends, these dividends are taxed as ordinary income and can be taxed at higher rates than qualified dividends. Many non-U.S. equity mutual funds (active and passive) have nonqualified dividends greater than 20% of the total dividend amount. Tax-smart funds will look to minimize this amount.

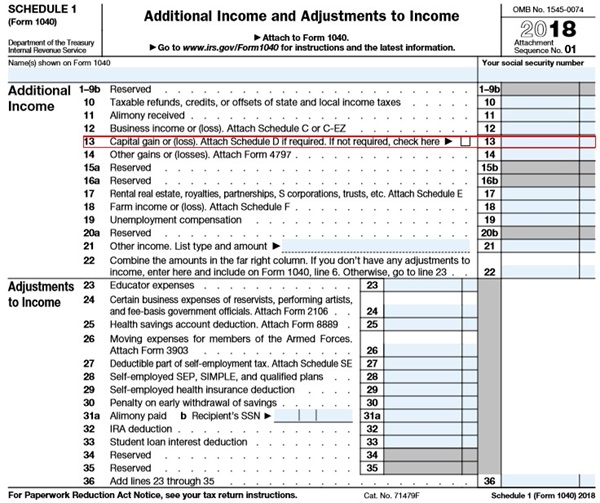

New Schedule 1, Line 13: Capital gain (or loss). Look to Schedule D to see the source of gains for line 13. Are the investments creating capital gains that are too high as a percentage of the investment amount? In 2018, the average U.S. equity mutual fund paid out capital gains equal to 11% of its net asset value. Does the distributed gain reflect an amount larger than this? Even 11% is painful and can likely be improved upon with a more tax-friendly approach.

Schedule D: Capital Gains and Losses and supporting statements: Look to see if turnover (the selling of mutual funds, stocks or bonds) appears too high given the value of the investment amount in Parts I and II. There may be a reason for the high turnover, such as harvesting losses or generating income, but one should understand the investment purpose of the turnover on Schedule D. Nonproductive turnover can lead to increased taxes.

And the attempt to make the new Form 1040 “post card sized” at 5 x 7.5 inches? The U.S. Postal Service stated they would deliver something this size at the standard-size letter rate, not as a postcard.

The bottom line

Helping your clients reduce the impact of taxes and maximize their after-tax returns can be one of your most valuable services. Thoughtful planning around taxes can improve successful after-tax outcomes.

For taxable investments, consider tax-managed equity funds, municipal bonds and thoughtful withdrawal strategies to help deliver successful outcomes. And remember that the goal is not to avoid taxes but to maximize after-tax wealth. Not paying tax is not a financial goal.

Disclosures:

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

Copyright © Russell Investments Group, LLC 2019. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

Russell Investments Financial Services, LLC, member FINRA (www.finra.org), part of Russell Investments.

RIFIS: 21433