Each year, Russell Investments examines the largest publicly listed corporate defined benefit (DB) plans, those with liabilities of $20B and above, which we refer to as the $20 billion club. This collection of jumbo-sized plan sponsors is uniquely situated to set the trends that the industry may follow. This paper and the following write-up provides an update on these plans' experience over 2018. We have reviewed the changes made by plan sponsors over the year as they continue the trend of de-risking and protecting their large investments in these plans.

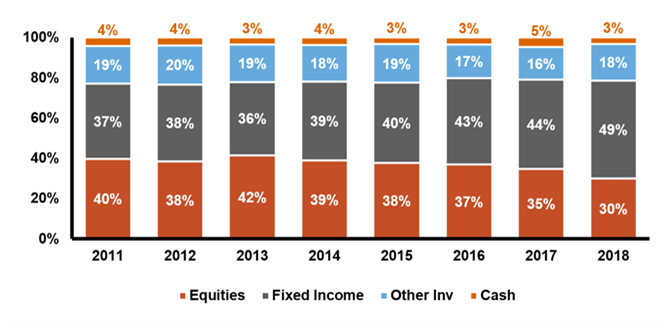

After several years of little news on the investment policy front, there have been big changes in asset allocations for the $20 billion club. Fixed-income allocations are up 5%, while equity allocations are down 5%. This shift in asset allocation is the largest de-risking move in recent history in a continuing shift out of risky assets. While some of this could be attributed to the fourth-quarter downturn (with equities down relative to fixed income), some companies have indicated intentions to de-risk their plan assets, such as Honeywell after a 19% increase to fixed income from 2017.

Source: 10-k filings

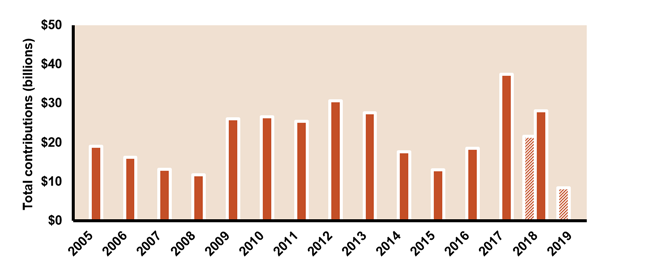

The $20 billion club also continues to funnel money into their plans. While the $20 billion club contributions were down from the record-breaking contributions in 2017, they were still at historic highs in 2018. Discount rates rebounded by 60 basis points (bps) from the lows in 2017, leading to significant increases in funded status. However, larger gains were not to be, as the global equity markets experienced severe difficulties during the fourth quarter.

Contributions and discount rate increases overcame the fourth quarter equity troubles to ultimately bring funded status up by 1% on average to 85%. ELTRA also continues to decrease as plan sponsors shift out of equities and into fixed income. While half of the group decreased their ELTRA, Honeywell and Pfizer had the largest decreases and reduced their ELTRA the by 100bps. In 2018, the $20 billion club saw an average decrease of 30bps, the largest decrease in the past 8 years . This brings the average ELTRA for the group to just under 7%, down 115 bps from 2011.

The $20 billion club continues to adjust the benefits policy to decrease plan costs and risks. This was no different for 2018 as several plans had freezes go into effect and executed annuity purchases. The full freeze of DuPont’s US and Pfizer’s US and UK DB plans went into effect in 2018. Also during 2018 FedEx, Lockheed Martin, and Raytheon made use of group annuity purchases and insurance buy-ins to de-risk their plans.

Plan sponsors continued to take advantage of the tax benefits associated with the Tax Cuts and Jobs Act of 2017, which ended for calendar year plans on September 15, 2018. Together 2017 and 2018 saw the largest two years of contributions in recent history, as 2017 was a record high year and actual 2018 contributions were 30% higher than expected. These circumstances have encouraged plan sponsors to prefund their plans. Contributions are expected to drop off a cliff as expected. 2019 contributions are down 77% from the high in 2017 and for some years after in certain cases. The following exhibit illustrates the contribution timing around other legislative events.

Source: 10-k filings

All these actions come together to continue the de-risking path that these jumbo-sized plans have been on for the past several years. The traditional asset-only allocation seen in the past appear to truly be a thing of the past, with the $20 billion club firmly at the forefront of the movement. For additional commentary and analysis, look here for the full report.

Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

These views are subject to change at any time without notice based upon market or other conditions and are current as of the date at the top of the page. It is made available on an "as is" basis. Russell Investments does not make any warranty or representation regarding the information. While all material is deemed to be reliable, accuracy and completeness cannot be guaranteed. The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

AI-27433-04-22

© Russell Investments

© Russell Investments

More Tax Planning Topics >