From June 2017 to June 2018, customers withdrew more than $30 billion from US bank accounts that didn’t earn interest — the first decline in more than a decade.1 Some of that may have been used to fund purchases, but there are also many people who have found more appealing opportunities for their short-term investments, largely thanks to multiple interest rate increases by the Federal Reserve (Fed) since 2015.

From 2008 to 2015, the Fed held the federal funds rate between 0% and 0.25%. When rates were near zero, risk-averse investors often preferred government-insured bank accounts rather than stretching for higher yields with longer-dated or lower-quality bonds. From 2008 to 2017, the Fed reported 10 years of consecutive inflows — totaling over $2 trillion — into bank deposits that earned no interest.2 But after several rate increases over the past few years, the fed funds rate now stands between 2.25% and 2.50%.

At Invesco Unit Trusts, we believe higher rates have created an opportunity for investors in short-term investment grade corporate bonds. Current factors making short-term bonds appealing, in our view, include a compelling rate environment, a flattened yield curve and less interest rate risk.

Reason 1: Higher rates

The Fed’s 3-Year High Quality Market Corporate Bond Spot Rate as of January 2019 was 3.3% which is near the highest level since 2009, as shown in the chart below.

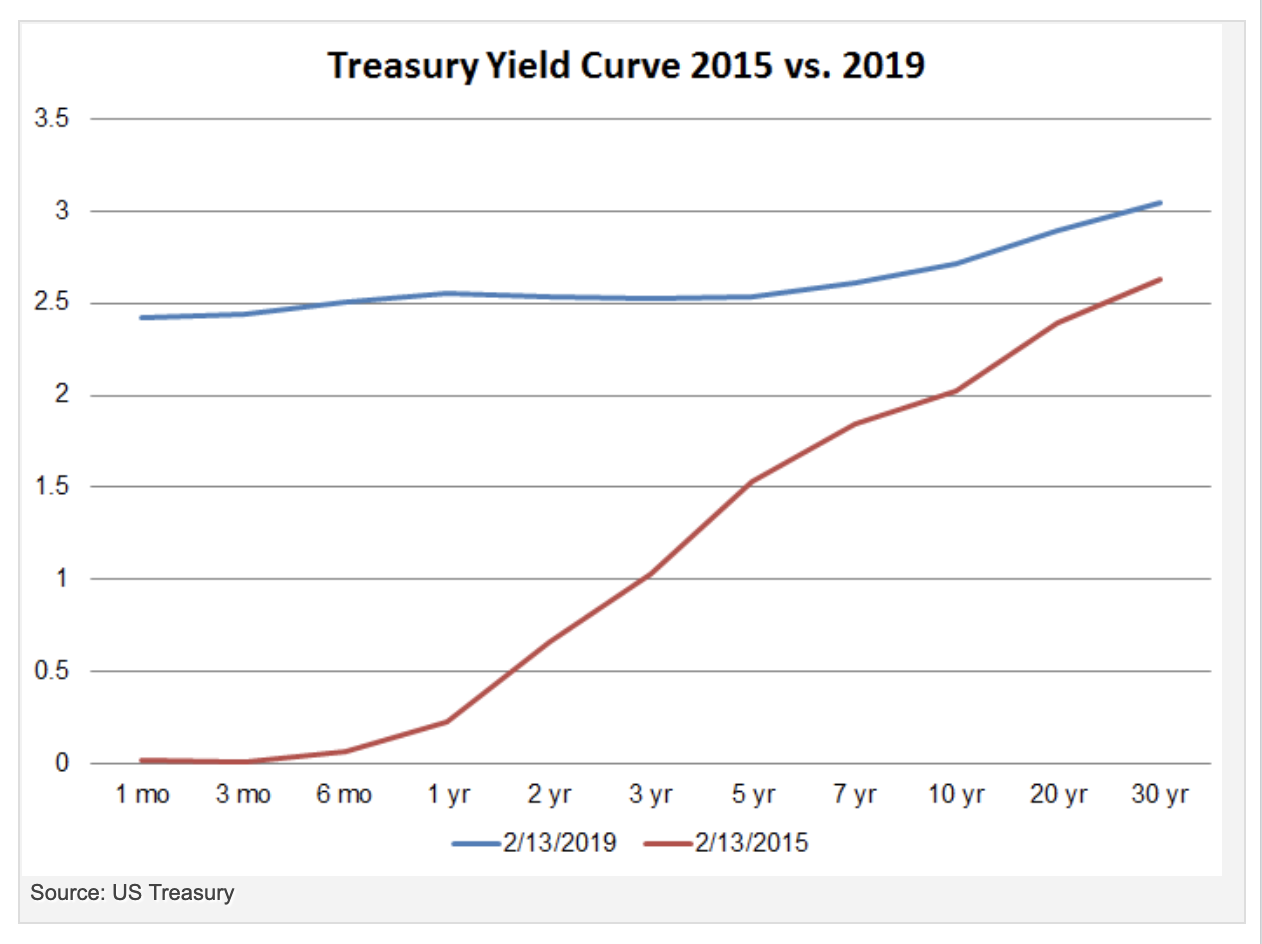

Reason 2: Flattened yield curve

The flattening of the yield curve has reduced the incentive to invest in longer-term bonds. As of Feb. 13, 2019, the 3-year Treasury rate was 2.5% versus the 30-year rate of 3.0%. By comparison, on Feb. 13, 2015, the 3-year Treasury rate was 1.0% versus the 30-year rate of 2.6%.

Reason 3: Less interest rate risk compared to longer bonds

Generally speaking, when rates rise, bond prices fall. However, if the Fed raises interest rates further, short-term bonds should be less impacted than long-term bonds.

Invesco Investment Grade Corporate Trust, 2-4 Year (IGSB)

Interested in the potential benefits of short-term corporate bonds? Talk to your financial advisor about the IGSB unit investment trust (UIT), a diversified portfolio of short-term corporate bonds.

At Invesco Unit Trusts, our process assumes we hold all bond issues to maturity, so investors can take comfort in knowing what bonds provide their monthly payments and, ultimately, the return of principal at the end of the trust. Second, we analyze the fundamentals of each bond, assign an internal credit rating for each bond and stress-test potential investments before adding them to the portfolio. Additionally, our surveillance process provides ongoing assessment of the credit quality for each issuer throughout the life of the trust.

1 Source: MSN.com, “Banks’ golden deposits are heading out the door,” Oct. 23, 2018

2 Source: Federal Deposit Insurance Co.

Important information

Blog header image: stilllifephotog/shutterstock.com

There is no assurance that a unit investment trust will achieve its investment objective. An investment in this unit investment trust is subject to market risk, which is the possibility that the market values of securities owned by the trust will decline and that the value of securities owned by the trust will decline and that the value of trust units may therefore be less that what you paid for them. This trust is unmanaged and its portfolio is not intended to change during the trust’s life except in limited circumstances. Accordingly, you can lose money investing in this trust.

An investment in the trust should be made with an understanding of the risks associated therewith, such as the inability of the issuer or an insurer to pay the principal of or interest on a bond when due, volatile interest rates, early call provisions and changes to the tax status of the bonds.

The value of the bonds will generally fall if interest rates, in general, rise. In a low interest rate environment risks associated with rising rates are heightened. The negative impact on fixed income securities from any interest rate increases could be swift and significant. No one can predict whether interest rates will rise or fall in the future. The negative impact on fixed income securities from any interest rate increases could be swift and significant. No one can predict whether interest rates will rise or fall in the future.

The financial condition of an issuer may worsen or its credit ratings may drop, resulting in a reduction in the value of your Units. This may occur at any point in time, including during the primary offering period.

During periods of market turbulence, corporate bonds may experience illiquidity and volatility. During such periods, there can be uncertainty in assessing the financial condition of an issuer. As a result, the ratings of the bonds in the Trust’s portfolio may not accurately reflect an issuer’s current financial condition, prospects, or the extent of the risks associated with investing in such issuer’s securities.

Although the underlying securities in the portfolio are rated at or above the minimum credit quality as of the date of deposit, the ratings may change after inclusion in the trust. The federal funds rate, or fed funds rate, is the rate at which banks lend balances to each other overnight.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Greg Rawls, CFA, CAIA

Investment Research Analyst

Greg Rawls is an Investment Research Analyst on the Unit Trust Investment Research Team, responsible for investment recommendations, surveillance and research.

Mr. Rawls has over ten years of industry experience, including equity and debt research. He has a diverse knowledge base with experience in equity, private equity as well as municipal and corporate fixed income securities.

Mr. Rawls earned a BS degree in finance from Marquette University, where he was a member of the Applied Investment Management Program, and earned a MS degree in finance from the University of Notre Dame. He is a CFA charterholder and a CAIA charterholder.

Read more commentaries by Invesco