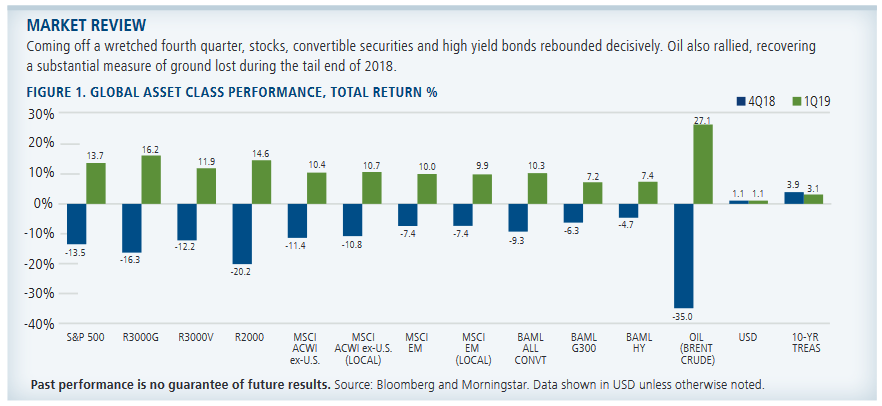

During the first quarter, market apprehension receded in the wake of the Federal Reserve’s December pivot to more dovish monetary policy. Investors set aside—or at least looked past—the anxieties that roiled financial markets in the fourth quarter. U.S. economic data remained positive overall, supported by business-friendly fiscal policy and a healthy consumer. Although many corporations issued more cautious guidance about future earnings in the first half 2019, markets focused on the string of strong earnings and revenue results being announced for the fourth quarter. Financial conditions improved dramatically after a December squeeze, and credit spreads tightened significantly. (Tighter spreads are a sign that corporate borrowers can issue debt more cheaply.) The global growth outlook improved, helped by a contained U.S. dollar, optimism about an eventual resolution to global trade disputes, and data supporting the view that China’s economy could achieve a soft landing. Looking forward, we believe:

- The U.S. economy will extend its steady expansion through this year and beyond. The global economy is positioned for moderate growth, with a pickup in the second half of the year.

- The relatively weaker earnings season currently underway reflects a high bar in terms of year-over-year earnings growth, and we would not be surprised to see earnings growth pick up in the second half of the year.

- Investors should not grow complacent: Volatility and sideways moving markets will characterize this phase of the economic cycle, due to a wide range of entrenched global uncertainties.

- Although we see tailwinds for economic growth and opportunities across asset classes—including in growth equities, convertibles and high yield bonds—conditions require a highly selective approach.

- Given the crosscurrents in the economy and markets, risk-managed alternative strategies can provide timely enhancements for both the equity and fixed income sides of an asset allocation.

United States

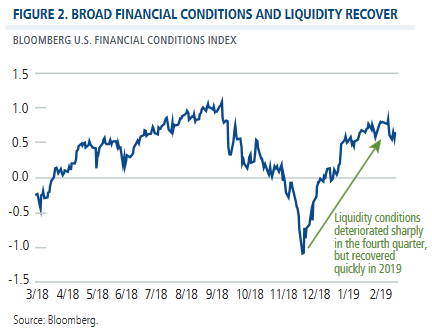

The U.S. economy is positioned for slow and steady expansion. As we have noted in our past commentaries, economic cycles should not be measured by their duration, but by fundamentals—and the fundamentals remain surprisingly compelling this long into an expansion. Energy prices and wages have risen, but inflation overall is benign. We expect healthy consumer activity to drive the economy, helped by wage growth, low unemployment and manageable debt levels. Broad financial conditions and liquidity have recovered after the fourth quarter’s tailspin (Figure 2). An accommodative Federal Reserve is likely to buoy U.S. economic growth and markets further, with positive knock-on effects globally.

Even though the initial boost of tax reform is in the rearview mirror, we believe that tax policies will still provide a sustained catalyst for the corporate sector, as will de-regulation. As we enter earnings season, we share the view that many corporations may be hard pressed to match or beat the earnings growth they posted a year ago. However, improving global conditions and continued steady growth in the U.S. could result in a reacceleration in earnings growth in the second half of the year, with positive growth for 2019 overall.

Although our U.S. economic outlook for these next quarters is constructive, this environment requires selectivity. We expect a stock picker’s market to prevail, rather than one in which a rising tide will lift all boats. The brief inversion of the yield curve should not be viewed as a precursor of imminent recession, but it does indicate building pressure within the economy, which we are monitoring closely, along with other potential risks such as corporate debt levels, shifts in global central bank policies, and indications of tightening in consumer borrowing. Geopolitical and U.S. political uncertainties are formidable and will fuel periods of short-term volatility; in the U.S., these will increase sharply in the run up to the 2020 election.

At this phase of the cycle, attention to valuations and company fundamentals will be essential. An improving global economy provides a favorable backdrop for a number of growth companies, including those tied to U.S. and global consumer activity. Our teams continue to identify opportunities in the financial sector, where we see compelling valuations. We are also looking for companies that are capitalizing on disruptive trends.

Global and International Strategies

We believe the slowdown in global conditions over recent months has likely been a soft patch, and we would not be surprised to see stronger economic growth data in the second half of the year. Accommodative monetary policy from global central banks, a contained dollar, and modest growth in the U.S. sets up well for non-U.S. markets. We expect the U.S. and China to reach a trade deal, and while this may not be the deal to end all deals, it would remove a key uncertainty. Regardless, economic conditions in China are improving, with consumer-focused stimulus, de-regulation and easing liquidity conditions sowing the field for green shoots.

In Europe, there are still many formidable headwinds—political uncertainty, social discontent and challenging fiscal policy. Even so, conditions are unlikely to get much worse. Given their close economic relationship, improved growth coming out of China could provide a welcomed boost to Europe, although as we have noted in the past, the impact may be tempered by the domestic bias of China’s consumer-focused stimulus.

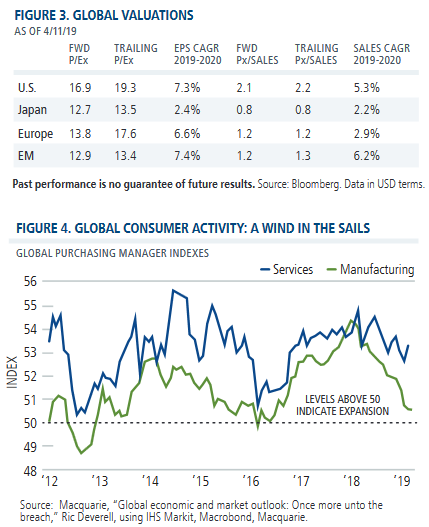

We expect to see more convergence among growth rates globally, and this “re-synchronization” of global growth should be positive for risk assets, including emerging market equities where valuations are compelling on the whole (Figure 3). From a regional perspective, we are favoring China, India, and Brazil. In Europe, our positioning is largely in global secular growth opportunities and in some cases, more regional businesses with stable, less-cyclical growth characteristics.

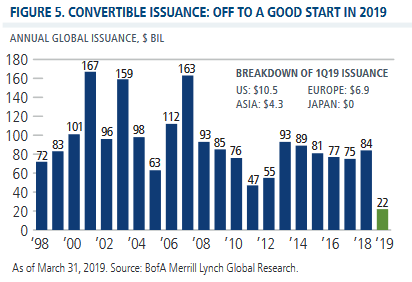

Our global and international strategies reflect a bias toward higher quality growth businesses, which served us in good stead during the quarter, as market sentiment pivoted to a more fundamentally oriented trading environment. We have emphasized companies that can benefit from consumer activity—the more robust segment of the global economy (Figure 4) and the linchpin of many of the long-term secular growth trends we favor. At the margin, we have been reducing our exposure to more defensive sectors given the strong performance of many of these positions during the past few quarters, which has resulted in less attractive risk/reward profiles.

Convertible Securities

Convertible securities snapped back very quickly from their fourth quarter declines. In an environment characterized by economic growth and market volatility, convertible securities provide an attractive way to gain equity market exposure while mitigating downside risk.

So far, convertible issuance trends have been encouraging (Figure 5). U.S. companies brought more than $10 billion in new issuance during the quarter, contributing to $22 billion of global new issuance. Although both U.S. and global issuance levels lag slightly behind last year’s pace, they are a solid follow through on 2018, particularly in light of the fourth quarter’s volatility. The market remains well distributed, including many convertibles that offer the characteristics we favor.

As we have discussed in the past, the attributes of convertibles can vary significantly and change over time, which necessitates the need for active management. Our positioning reflects this dual focus, as we seek to manage the hybrid characteristics of convertibles to capture more equity upside than downside over full market cycles. We continue to view market volatility as an opportunity to rebalance the portfolio, maintaining a preference for secular and cyclical opportunities, primarily in technology, health care and select areas of the consumer sector. Because of their outsized exposure to stock market downside, we remain cautious on the most equity-sensitive issues.

Fixed Income

A flat yield curve is likely to persist as a global low rate environment keeps long-term rates in check and the Fed pauses in its hikes. We believe the yield of the 10-year Treasury is likely to be in the area of 2.75% to 3.00% at year end. This base case assumes that inflation pressures build modestly in the second half of the year and also that the U.S. holds to the pace of slow and steady growth we expect.

As we noted, we do not believe that the inversion of the curve earlier this year sets the shot clock for a recession. But we are paying attention to what the curve could be saying about the pressures at this stage of the cycle. Curves typically invert during tight labor markets, and a flat curve tends to disincentivize growth in a variety of ways—including squeezing net interest margins for providers of capital and increasing the cost of capital for borrowers.

Given our outlook for interest rates and the economy, we remain constructive on high yield issues, and expect defaults to remain below the long-term historical average of 3% until U.S. economic activity softens. Even so, rigorous research and risk management will be very important at this point of the cycle. As we have discussed in the past, we take a bond-by-bond approach focused on being well compensated for risks we undertake. We are favoring companies with reliable debt servicing and stable-to-improving leverage metrics. We maintain elevated caution about the lowest credit quality tier of the investment grade market, where high levels of debt on balance sheets give us pause.

Conclusion

We have shared our favorable outlooks for economically sensitive areas of the market, including growth equities, high yield and convertible securities, and we maintain high conviction that our teams will be able to capitalize on evolving opportunities through active, fundamentally driven approaches. Given the challenges facing investors today—including equity volatility and persistently low interest rates—we believe there are also considerable potential benefits for including risk-managed liquid alternative strategies within both the equity and fixed income sides of an asset allocation.

For example, on the equity side of the allocation, our global long/short and hedged equity approaches can change their level of exposure to the equity market, dampening the impact of volatility while still participating in upside. Meanwhile, to address the limitations of traditional fixed income bonds in a low interest rate environment, our market neutral income approach sources income from strategies that are not dependent on interest rates.

When markets rally as strongly as they did in the first quarter, investors may be inclined to overlook the need for risk management. However, as the fourth quarter illustrated, markets can succumb to short-term selloffs in the midst of longer-term advances. Successful asset allocation strategies should focus on both current opportunities as well as being prepared for turns in market, economic and political cycles.

We remain committed to helping investors navigate the current investment environment as well as the course ahead, and we thank you for your continued trust.