Spring Quarterly Commentary

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Science advances one funeral at a time.” (paraphrased)

Max Karl Ernst Ludwig Planck, 1858-1947

German Physicist

Nobel Prize Winner, 1918

Originator of Modern Quantum Theories

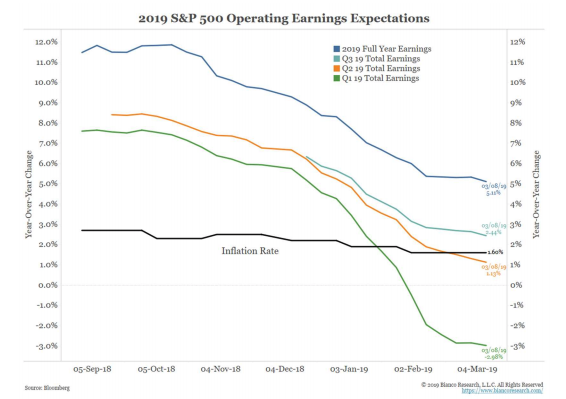

A near mirror image of the fourth quarter, the first quarter began with the stock market rocketing higher in a nearly straight line. In one of the strongest quarters since the current bull market began in 2009, it managed to largely erase the carnage of the prior quarter and index levels are now back at all-time highs. Curiously, corporate earnings are trending in the opposite direction. First quarter earnings are expected to be lower than a year ago, with growth projected in only three of eleven sectors.1 At present, the back half of 2019 is supposed to deliver better earnings growth, but Wall Street always seems to expect better conditions... just a little over the horizon. The chart on the next page shows earnings estimates over time, and they have been coming down (the first quarter is in green).

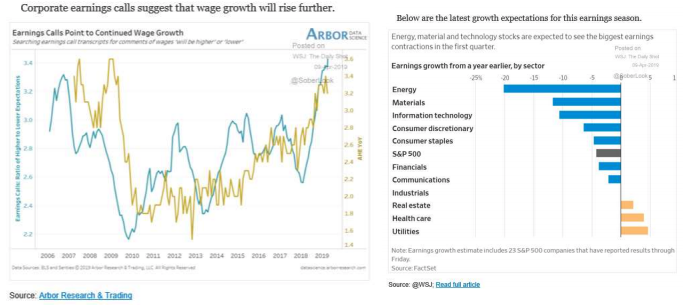

There are a lot of indications we are “late” in the economic cycle. Companies are talking a lot about higher wages, which typically leads increases in average hourly earnings, as the below left chart illustrates. Those higher wages can be good for the economy, but also can squeeze corporate profit margins and lower profits.

There are some other potentially worrying signs, such as a decline in shipping indexes and slowing growth in factory orders, but overall, employment and economic growth are fine... which is of course rather late cycle in and of itself.

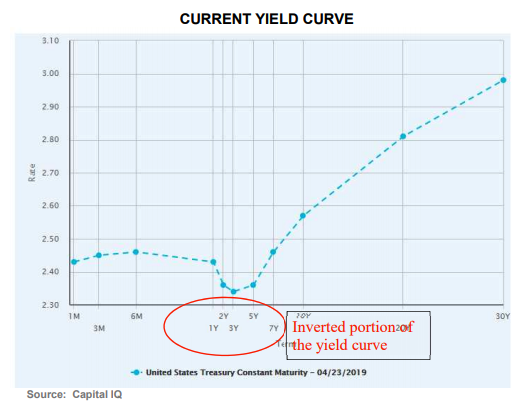

The biggest sign of caution this quarter came to us from the bond market. The Fed says it will hike rates twice during 2019, as it would in a healthy economy. The bond market disagrees, sees signs of economic weakness, and is thus pricing in a near 80% likelihood that the Fed will instead cut rates in 2019. Relatedly, last quarter we wrote about what an ominous sign it would be if the yield curve inverted2, and this quarter it finally happened! Well, sort of. We wrote about the figure that Wall Street pays the closest attention to: the 10y-2y spread, which is inverted when the 2-year treasury note yields more than the 10-year treasury bond. That spread is presently just fine3. However, this quarter the 10-year briefly yielded less than the 3-month treasury, meaning that the 10y-3m inverted (and then un-inverted) as you can see at the top of the next page. While practitioners tend to focus on a 10y-2y inversion, the Fed has said it believes the 10y-3m has a better predictive record.

The NY Fed maintains a model based on this 10y-3m spread which predicts the odds of a recession in the coming year. Historically, the yield curve flattened, and the odds of recession increased, heading into the grey recessionary bars in the chart at the top of the next page. The Fed says everything is fine, but their own model puts the odds of recession within the year at 27%.

As useful as models are, it is always best to go back to the actual data when trying to determine if an indicator is worth paying attention to. Here is a chart showing the history of the 10y-3m spread all the way back to 1920. Negative readings on the chart mean the yield curve was inverted and the shaded bars represent recessions.

There were in fact some false alarms and an entire period in the late 1930s – 1960 where the signal didn’t work at all. And yet for most of the last 100 years, it has been fairly reliable.

There is also the question of timing between a 10y-3m inversion and a resulting recession. Long ago the 3 mo. – 10 yr. spread (light blue bars on our chart) inverted after recessions began, but in recent years it has become an (increasingly) leading indicator. The average postwar lag between 10y-3m inversion and recession has been 10 months.

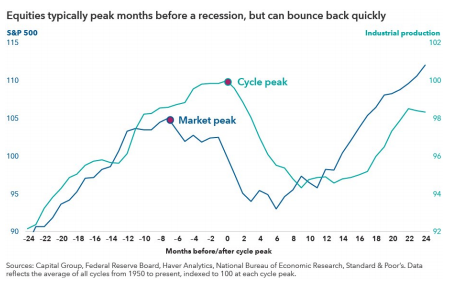

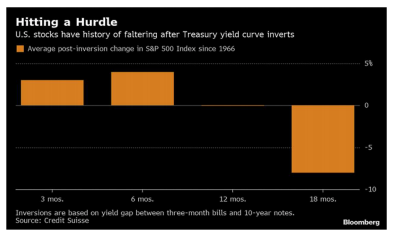

But what we really care about is the stock market reaction, not the recession itself. This lag is shorter: the market peaks on average six months ahead of economic downturns. This means we need to be thinking now about what the economy will look like later this year. The future isn’t always like the past, but if it rhymes, we might expect a market top six months after inversion (September 2019) with a recession following four months after that (January 2020). Something to keep in mind.

Now we’d like to switch gears and instead of writing about the economy, we’d like to write about economic theory, specifically, Modern Monetary Theory (often abbreviated as MMT). MMT is a topic which, while not having quite broken through to the mainstream, is becoming ever more commonplace in economic circles. It is likely to be a presidential campaign topic and we think will be increasingly talked about for another reason which we will get to later.

First, a primer. Modern Monetary Theory has emerged not so much as a challenger (it’s not popular enough) to orthodox neo-Classical conceptions of the economy, but at least as an alternative. MMT is not so much a single unified theory as it is a collection of ideas which come together to form a general understanding of how the monetary system works... and really just ideas about how the monetary system works for governments that issue their own fiat currency and borrow in that currency4. This is incredibly short shrift, but the main idea of MMT is that governments have more freedom to print money, spend freely, and run deficits than commonly thought. Speaking broadly, there are two parts of MMT. First there is what we will call descriptive MMT: a body of theories on how the monetary system works and what governments (who issue debt in their own currency) can do. Descriptive MMT is academic and conceptual. There is also prescriptive MMT: a set of policy prescriptions about what governments should do, which is necessarily political. So those are the two parts, but there are also two distinct types: SeriousMMT and Bastardized-MMT, and keeping these separate assists in comprehension.

Bastardized-MMT posits that governments can just print money willy-nilly without consequence. Its “proponents” urge governments to just run the printing presses to pay for all sorts of desired spending because “deficits don’t matter”. This notion has few adherents and innumerable detractors because it is a straw-man argument: one which people set up just to knock it down. It isn’t the real thing. This political season, you are likely to hear many commentators denigrate anyone who doesn’t immediately foreswear MMT, labeling them a dangerous quack who would lead the U.S. down the road to Venezuela5. Remember, they are talking about Bastardized-MMT... something that no one actually believes.

Serious-MMT says “of course” deficits matter, just not as much or in the same way that traditional economic theory posits. It points out the fact that a government which issues debt in its own currency never runs a risk of defaulting on that debt, because it can simply print more money to pay it back. However, a government cannot just go crazy doing whatever it wants. If it prints and spends too much money, it will be constrained by inflation6. We are far from ready to endorse Serious-MMT wholesale, but it seems reasonable to us that if you place idle assets into productive use (i.e. print money to employ the unemployed) – the consequences will not necessarily be dire. That’s what the policy arm of Serious-MMT recommends – the employment of idle assets in productive use via limited deficit spending. It’s worth noting a few things about Serious-MMT:

Serious-MMT is serious. Many economic papers on the subject have been written and published in academic journals.

Serious-MMT is not brand new. Discussions of the underlying ideas go back to at least the 1990s, though only now has the larger economic community taken notice.

Serious-MMT is probably at least half right! Consider Japan: traditional economic theory predicted that Japan’s fiscal deficits and rising debt levels would “crowd out” private investment, leading to rising interest rates and inflation. And yet despite some of the highest deficits in the world, interest rates in Japan have in fact hovered near zero for more than two decades and inflation is non-existent.

Serious-MMT is not without its prominent admirers. Former PIMCO Chief Economist, Paul McCulley recently suggested MMT offers a “robust architecture for a fiat currency world.” He went on to say, “Last time I checked, the U.S. has missed its inflation target for 10 years running, of which seven or eight were at zero interest rates. Let’s look at reality here, Zimbabwe is not on our curve.”

Economics is less understood than physics and its laws are not necessarily as immutable – the world did not even have real fiat currencies until Nixon closed the gold window in 1971. Even if SeriousMMT is not “right”, there is much in conventional economic theory that appears to be wrong, or at least incomplete... and when old theories cease to fully explain observations in the field, old theories must be set aside, and new ones examined. When that happens, as Max Plank noted in the introductory quote, there will always be resistance from the old guard. Thus, some descriptive aspects of Serious-MMT might indeed be “right” and at least deserve a serious and fair hearing7.

Importantly, we think MMT is going to become an ever-larger part of the conversation, and indeed we think it will eventually be implemented to some degree, not at all because it is “right”, but because it would allow politicians to do what they want to do and not pay for it8! MMT has the potential to be a theory adopted not because of its merits, but because it serves as a useful and politically expedient justification for what politicians wanted to do anyway.

However, if this is the real reason MMT policy prescriptions like deficit spending, tax cuts, low interest rates and money printing are likely to be adopted, is it more likely to be Serious-MMT, where politicians carefully and dispassionately evaluate just how much deficit spending can be undertaken without sparking inflation? Or will we end up with the policy prescriptions of Bastardized-MMT: printing money willy-nilly until we finally cause a currency and inflation crisis? The question is not just whether Serious-MMT works in theory (still a debate). It’s not even about whether it could work in practice. It’s also about whether it would work in practice. Keynesians extol the virtues of running deficits during recessions while saving money and running surpluses during expansions. But what actually happens? In practice, politicians focus on the short term and run deficits during recessions... and then “forget” and run deficits during expansions. They don’t follow the theory. Any embrace of MMT policy prescriptions would risk this outcome9.

To sum it all up:

Bastardized Descriptive MMT is a straw man that no one actually believes.

Serious Descriptive MMT has a relatively good predictive track record and should be considered seriously.

Serious Prescriptive MMT might be useful, but we think it is dangerous because if implemented it might actually turn into:

Bastardized Prescriptive MMT, an after-the-fact justification for massive government spending which would risk hyperinflation or a currency crisis.

This will be an interesting area to watch going forward.

One final note: we have instituted a $40,000 minimum for those under age 40. We look forward to helping our next generation build a path toward financial security.

Sincerely,

John G. Prichard

Miles E. Yourman

1 We cannot help thinking this is consistent with the idea we expressed in our Summer Q2 2018 letter: the corporate tax cut would initially boost corporate profits but then some of those newly fat net margins would be eroded as companies compete more on price.

2 Last quarter’s letter includes an introduction to what the yield curve is and can be found at www.knightsb.com. In general, the curve is inverted when a longer-term government bond yields less than a shorter-term government bond. When comparing two specific spots on the yield curve (two specific maturities) it can be called a “spread” and is likewise “inverted” when the long maturity yields less than the short maturity (expressed as a negative spread value).

3 Well, at 20 bps it is in the “flashing yellow” zone, but at least it is not inverted.

4 Japan and the United States would be good examples of countries that issue their own fiat currencies and issue debt in that currency. So the ideas we usually talk about when we talk about MMT would not apply to countries like Italy, which does not issue its own currency (the multinational ECB does) nor to most emerging market countries, which often do issue their own currency, but equally as often issue debt (borrow) in a foreign currency.

5 For the next two years we’re bullish on people claiming that other people want to turn us into Venezuela.

6 To be fair, too much inflation can result in a default-like situation but is technically different.

7 If one is to accept Serious-MMT, the most important question becomes how much money printing and deficit spending can an economy tolerate? So far, we haven’t seen material on MMT that even addresses, let alone satisfactorily answers this key question. If the amount able to be tolerated were only a few percent, then what is the difference between MMT and seigniorage anyway? However, as we said, MMT has actually generated a lot of material and we’ve yet to review most of it so perhaps this question has been addressed and we are unaware.

8 So far, Serious-MMT policy prescriptions have only been openly embraced on the left side of the political spectrum. Its highest profile proponent was Bernie Sanders’ Chief Economic Advisor during his 2016 run, and Alexandria Ocasio-Cortez has famously embraced it as part of the Green New Deal. We would note, however, that it is the current administration which has done more than anyone else to actually implement MMT’s policy prescriptions, by substantially increasing deficit spending and advocating for the Fed to keep interest rates low and resume QE (money printing).

9 To be fair, the Fed has done a pretty good job over the last 40 years of managing a fiat currency without rampant inflation, currency depreciation, or succumbing to the pressure to print more money endlessly... so far.

Past performance is not indicative of future results. The above information is based on internal research derived from various sources and does not purport to be a statement of all material facts relating to the information and markets mentioned. It should not be construed that the information in this commentary is a recommendation to purchase or sell any securities. Opinions expressed herein are subject to change without notice.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All