Weighing the Week Ahead: Should Investors Fear A Market Top?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe calendar is modest, with the big reports all hitting last week. Investors will never have more current information on the economy, the Fed, corporate earnings, and various risks than they do right now. It is difficult to guess what the punditry will do when given an open slate. We should be asking:

Should we fear a market top?

Last Week Recap

In last week’s installment of WTWA, I took note of the avalanche of relevant data, suggesting that it was time for some synthesis and analysis. I didn’t expect any help from the pundits, who analyzed piecemeal as expected. I hope that readers did better by using my suggested framework. More about that below.

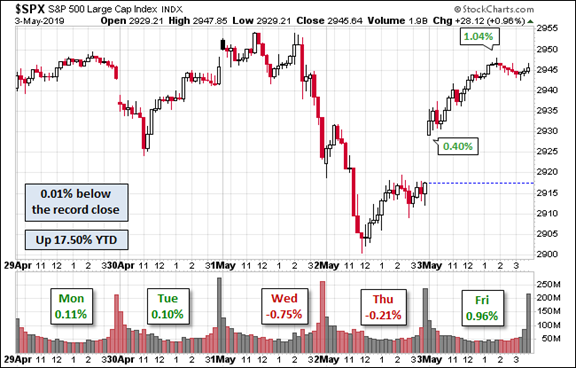

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski, who packs a lot of relevant information into the weekly chart without sacrificing clarity.

In another quiet week, the market was virtually unchanged. The trading range was only 1.8%. The volatility seemed higher to some, because of the two-day decline after the Fed meeting. As always, our indicator snapshot in the quant section below summarizes volatility and the VIX index in various time frames.

Noteworthy

Mrs. OldProf wishes everyone a happy Star Wars Day (May 4th, for those who need a hint). RIP Peter Mayhew.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

When relevant, I include expectations (E) and the prior reading (P).

New Deal Democrat’s high frequency indicators are an important part of our regular research. In his post this week, Further Trend Toward Positive Numbers Could Signal A Renewed Boom, he reports that indicators in all time frames have become more positive. NDD remains skeptical and is watching indicators closely.

The Good

- Personal spending rebounded 0.9% even more than the expected 0.8% and P of 0.2%. But see personal income below in the “bad” section.

- Core PCE registered no increase versus the 0.1% expected and prior. The overall index was up 0.2%.

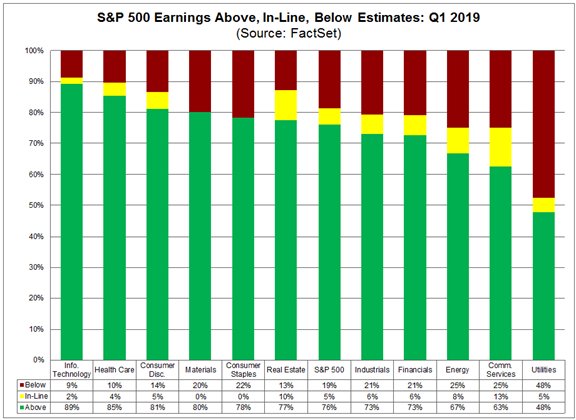

- Earnings growth remains strong. Brian Gilmartin describes the positive revisions to the S&P 500 estimates – now taking the lead over negative changes. John Butters (FactSet) updates earnings season results, which continue a beat rate higher than we have seen in the last five years. Here is the sector breakdown.

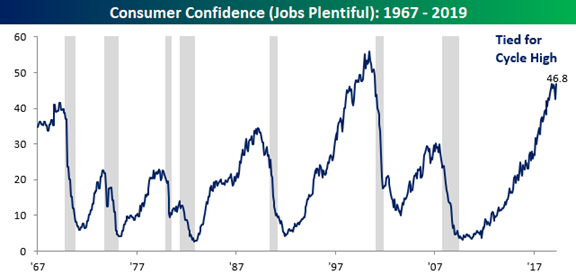

- Consumer confidence for April registered 129.2 better than the expected 125.3 and P of 124.2. Bespoke’s analysis includes the charts we have come to expect and the reasons behind the rebound. I enjoyed meeting their chief global strategist, George Pearkes, at last weeks National Association of Active Investment Managers meeting in Phoenix. George gave a fine presentation to the entire group and answered questions with aplomb.

- Factory orders increased by 1.9% in March, beating expectations of 1.6% and much better than February’s decline of -0.3%, revised from -0.5%.

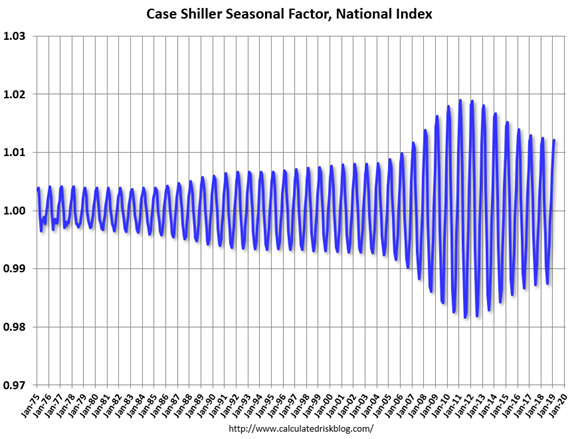

- Pending home sales bounced 3.8% in April, beating expectations of 1.1% and the prior month decrease of -1.0%. Calculated Risk reports and comments on seasonal factorsin home prices, which increased during the bubble and have declined since.

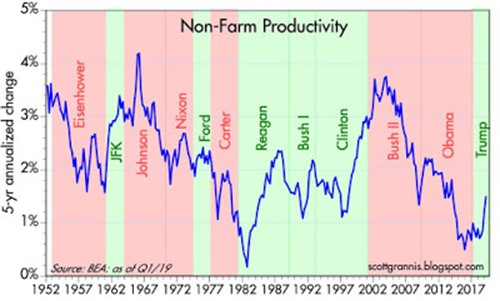

- Q1 productivity increased by 3.6% nicely beating expectations of 2.3% and the prior of 1.3% (revised downward from 1.9%). (Scott Grannis).

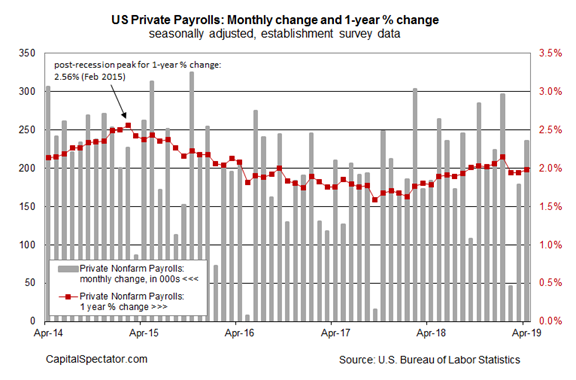

- Payroll jobs increased 263K. (E 200K and P 189K). James Picerno provides an early take with reactions from some key economists.

My own quick take was that it was not as good as it seemed, but my own concerns related to the Household survey.

New Deal Democrat, rather dour of late, identifies leading indicators of a slowdown or a recession.

My FATRADER colleague, Eric Basmajian, prefers to use a second derivative approach, measuring the pace of deceleration. He also highlights key sectors showing weakness, especially jobs in auto production.

Meanwhile, the headline number, and the low unemployment rate, dominated the headlines for regular news shows. It was also great for political spin. There is nothing unusual about that, except that the participants have changed sides!

The Bad

-

The ISM manufacturing index, the only one of the PMI measures that has a long history, declined to 52.8, missing expectations of 55.0 and last month’s 55.3. Read the official ISM site for some color, including border delays with Mexico and suppliers moving out of China to avoid tariffs. ISM data suggests that a reading of 52.8, “if annualized, corresponds to a 2.9% increase in real GDP.”

-

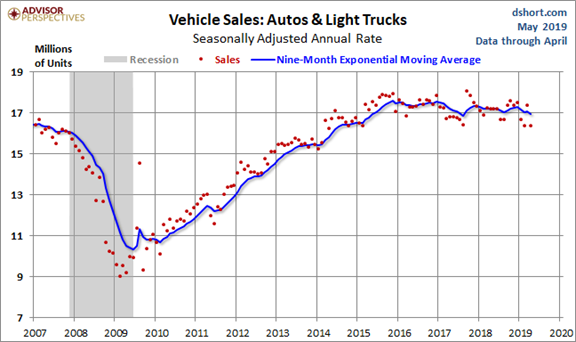

Light vehicle sales for March were only 16.4 million (SAAR), 5.7% lower than in February. The series is pretty noisy, including the erratic effects of holiday promotions. Jill Mislinski’s chart shows both the actual sales for each month as well as a moving average.

-

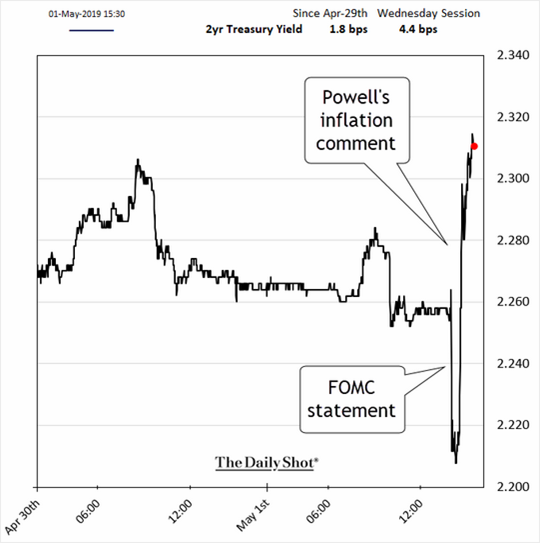

The FOMC rate decision was exactly in line with expectations. A word or two in Chairman Powell’s press conference let to a negative market reaction. Top Fed analyst Tim Duy explains how The Fed Muddled Its Inflation Message. Here was the reaction (via the Daily Shot).

-

Construction spending declined by -0.9% worse than the expected gain of 0.1% and February’s (downwardly revised) gain of 0.7%.

-

Hotel occupancy decreased on a year-over-year basis. It is down -1.4%. Another alleged Easter effect? (Calculated Risk).

-

Rail traffic declined on a year-over-year basis. (Steven Hansen, GEI).

-

Initial jobless claims remained a bit off the levels of a month ago. 230K was the same as the prior week, suggesting that the “Easter timing” explanation was not correct.

- ISM non-manufacturing declined to 55.5 from last month’s 56.1 and missing expectations of 57.4. The ISM official site provides detail and color. They state, “The past relationship between the NMI® and the overall economy indicates that the NMI® for April (55.5 percent) corresponds to a 2.4-percent increase in real gross domestic product (GDP) on an annualized basis.”

-

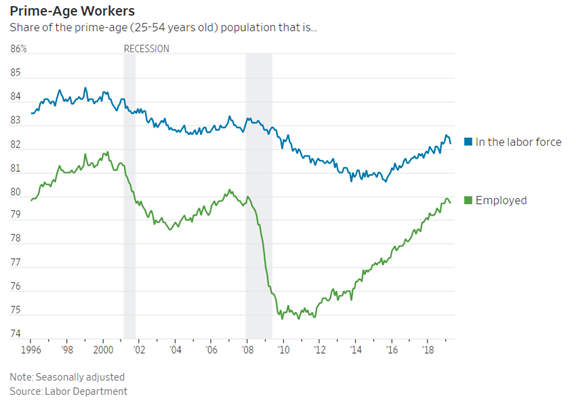

Employment reflected by the household survey was very different from the payroll report. The BLS reported an unemployment rate of only 3.6%, and that was the newspaper headline. Unemployment did decrease by 387,000, but the labor force declined by 490,000. Business cycle expert Bob Dieli gave the Household report a grade of “F.” The WSJ chart (see the full article for much more) shows the downtick among prime-age workers.

The Ugly

There are so many incidents of senseless violence. We also have massive natural disasters, like the typhoon in India. Anyone not affected should be grateful and helpful to those who were.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

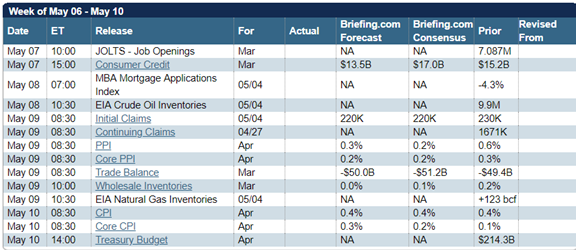

After last week’s data avalanche, this week’s calendar is light. Inflation data will get attention, especially given discussion that the Fed is considering alternative measures. I am interested in the JOLTS report as insight into labor market structure, but most simply use this to gauge employment growth.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Last week’s calendar included the key reports, leaving us with a much lighter schedule this week. While earnings reports continue, we have the key trends in mind. Fresh data feature PPI and CPI. Since these are expected to increase more than last week’s PCE measure, there could be some talk about the Fed switching to an alternative measure.

I haven’t seen a good synthesis of what we learned in the fragmented methods of financial media. We should be asking:

Should investors fear a market top?

Last week I provided a guide for data interpretation. It was not as much fun as the Buffett Bingo Card for today’s meeting but should have a bigger payoff for readers. Remember that we were suggesting a baseline of real GDP growth of 2 – 2.5%, enough to support earnings and a continuing stock rally. The key questions are below, with the result in italics.

- The FOMC meeting is very unlikely to reflect a change in policy, so be alert if it does. I don’t regard modest changes to current policy as very important, but the market is reacting aggressively in such cases. Here is a cheat sheet based upon recent FedSpeak. [There was no change of policy. Nearly all Fed members have weighed in after the employment report. The Fed is “patient” and on hold.]

- Personal Income and (March) and Spending (February) are key elements of the economic picture. We’re still catching up from the shutdown. Income is especially important. [Personal spending was high while income had only a slight gain. Since spending drives the GDP benchmark, it meets our test, but ultimately income gains are required.]

- PCE price index. The core rate is the Fed favorite, so it is more important than other inflation indicators. If it remains low, the Fed will remain on hold. [This was good news.]

- ISM manufacturing index is important as a near-contemporaneous read on an important sector. It has some leading qualities for employment. ISM non-manufacturing covers a wider range of businesses but has a shorter history. The historical relationships are a key to any inference about overall economic strength. Beware of dramatic reactions to a small change. [As expected, the result drifted lower. Despite this “bad” news, the data are consistent with our benchmark suggestion.]

- Employment is a fundamental element in measuring economic strength. We crave this information so much that we are often uncritical about the data. I am equally interested in the ADP report and the “official” non-farm payroll report. They use different methods, and each contributes value. [Both the payroll jobs and ADP reports were excellent. The household survey has drifted away from these results and needs further consideration. In any case, it does not suggest weak economic growth.]

- Corporate earnings should support the current economic picture, both in continued earnings beats and outlook. [The earnings story continues to be excellent. Current earnings have a high beat rate, and forward earnings are seeing upward revisions.]

- Housing data are less interesting. Case-Shiller prices are older and on a subset of the data. Pending sales are interesting, but less significant than the new home sales data. Construction spending is also of lesser importance. [The pending sales data were strong and construction spending weak. The mixed picture is in line with the benchmark growth suggestion.]

Does the evidence support the base case of 2 – 2.5% growth? That should be the question for each report – not whether there is a small change from the prior month. [It was a clean sweep. While some reports were lower than expectations nothing suggested a violation of our base case.]

I have a few additional conclusions in today’s Final Thought.

Quant Corner and Risk Analysis

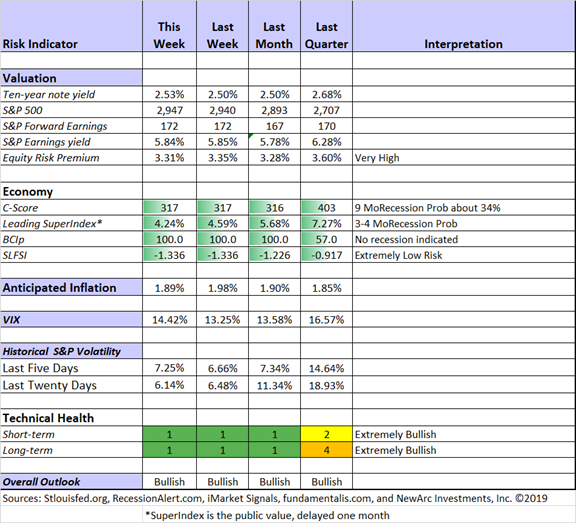

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term and long-term technical conditions continue at the most favorable level. Our fundamental indicators have remained bullish throughout the December decline and rebound. The C-Score reflects the increase in headline inflation, despite slight steeping in the yield curve. I am watching this closely, including analyzing signs of possible confirmation of higher recession odds. We remain well within the warning period.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession and he has pushed back the date for possible concern indicated by his employment model.

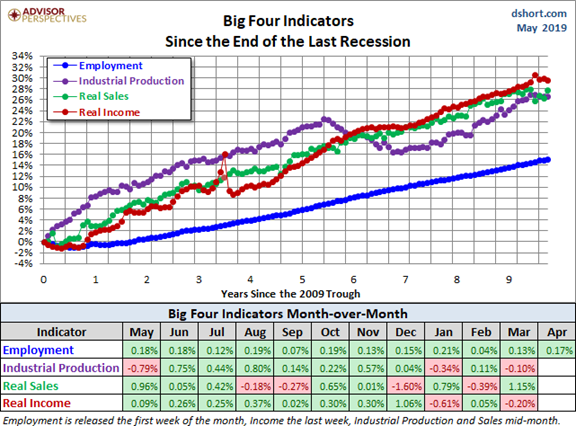

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis, especially the Big Four indicators most important for recession dating. Here is the current picture.

The picture has a few red spots but remains strong.

Guest Commentary

“Davidson” (via Todd Sullivan) explains the oil inventory build that has depressed oil prices and energy ETFs – refinery downtime for capacity upgrades.

Exxon has reportedly restarted its refineries after being shutdown for capacity upgrades, but other refiners have shutdown for similar capacity upgrades. The Net-Net is that refining activity is unusually low for this time of year and we see a sharp drawdown in gasoline inventories which are usually building for summer demand.

We can only watch to see when refining activity returns to normal seasonal levels.

Insight for Traders

Check out our weekly “Stock Exchange.” We combine links to important posts about trading, themes of current interest, and ideas from our trading models. Last week we took up a theme from that sage, Yogi Berra, the future ain’t what it used to be. We provided some specific trading themes as well as the expected expert advice. As always, we cited some great sources and discussed some recent picks from our trading models. With all of the models back in action, there are more trading ideas and interesting contrasts with a fundamental approach. Felix rated the top twenty stocks in the S&P 500 and Oscar did the same for the most liquid ETFs. Pulling this altogether was our regular editor, Blue Harbinger.

Insight for Investors

Investors should embrace volatility. They should join my delight in a well-documented list of worries. As the worries (shutdown, Fed policy, trade) are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Dr. Brett Steenbarger’s Trading Psychology: How to Improve Your Trading Results. It is further amplified in this Forbes article. As he often does, Dr. Brett highlights principles that are important for traders and investors alike. Here is a key quotation:

Many traders focus on their results–their P/L–and never make the process changes that could lead to sustained results. A great deal of writings in the area of trading psychology emphasize the changes that traders should make–not actual techniques traders could employ to make those changes.

Brett made a dynamic presentation at the NAAIM conference, drawing rave reviews. His comments inspired my own ideas about how investors become preoccupied with the short-term implications of a trade. The immediate dollar result is not the best criterion, despite its popularity. What is a Good Trade?

Stock Ideas

Chuck Carnevale continues his sector-by-sector quest for attractively valued stocks. Each post in this series provides both interesting ideas and a lesson in how to perform solid analysis. He analyzes the technology services sector where “sound valuation has been thrown out the window.” Despite this, he identifies five stocks to consider, comparing them to some of the big names. His post on the transportation sector focuses on only four candidates (you’ll recognize them all) from airlines, air freight, trucking, railroads and other transports.

Kirk Spano analyzes the cross-currents in oil and gas stocks. He identifies the current sources of selling as well as the effect of the Anadarko Petroleum Corp (APC) buyout offer. With a long-term trend away from petroleum stocks, monitoring these trends and possible further consolidation is important for investors. He references a prior article (which I linked to at the time) discussing his “dirty dozen” choices for 2019.

Stone Fox Capital opines that the reaction of Alphabet (GOOG) stock to the revenue miss was overdone – a “crazy reaction.” Peter F. Way sees more upside in Facebook (F).

Peter F. Way maintains that the best auto stock does not make autos. What is necessary for the wheels to go ’round? His unique, market-maker method displays a risk reward chart for this universe.

My colleague at FATRADER, Bhavneesh Sharma, was recently ranked #1 at SumZero’s institutional stock-picking platform. Last week I cited Part One of his analysis of Moderna Therapeutics (MRNA). Here is Part Two.

Charlie Munger prefers Costco (COST) to Amazon (AMZN). (WSJ). [I’m not sure he is considering Amazon Web Services in reaching that conclusion]. And why is Amazon a Warren Buffett pick?

Or how about the #3 off-price retailer, Burlington Stores (BURL). (Barron’s).

A bottom in Gilead (GILD). (John C. Ogg, 24/7 Wall St.)

Yield

Ploutos reviews the dividend aristocrats, including YTD performance and long-term comparisons.

The Rose Portfolio had a great April, with a 19.7% increase in income over April of 2018. This is a fully transparent portfolio without a lot of turnover.

It is also important to know when to sell your dividend stock. Dividend Sensei identifies three blue-chips that you might want to sell. And also three that you might buy.

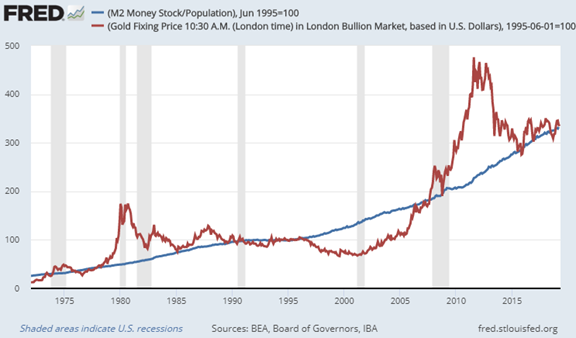

Gold

Gold represents a challenge for the value investor. As Lyn Alden Schwartzer writes,

Gold stocks, meaning companies that mine gold or finance gold production, can potentially throw a wrench in a value investor’s plan. Gold is an esoteric commodity; a substance that has ideal characteristics to store wealth but is endlessly debated on how to value it. It produces no cash flows, which throws out discounted cash flow analysis as a valuation tool. The bulk of it is not consumed by industry, so the immediate balance between supply and demand does not dictate price, since most gold ever mined is still stored and can be sold. And yet, in order to value gold stocks as businesses, we need to be able to determine if gold is grossly overvalued, deeply undervalued, or somewhere in the middle. Hence the problem.

She uses two charts to help in adjusting her allocation. Here is one of them but read the full post for the reasoning and the second method.

Personal Finance

Abnormal Returns always provides interesting ideas on a wide variety of topics. I am a subscriber, and I read it daily. Each Wednesday’s edition includes a post focused on personal finance. This week I especially appreciated the excellent post by FATTAILED, Prepay Mortgage Or Invest? Leverage & Negative Bonds. This is a frequent question and the post provides a good analysis with easy-to-understand examples. I doubt that most think of their mortgage as a negative bond. And your risk calculation depends critically on the real estate cycle.

Gil Weinreich’s series on Seeking Alpha (SA for FA’s) is ostensibly geared to financial advisors. The analysis is much broader than that. Most DIY investors will find it quite useful. This week I especially enjoyed the post, The Problem of Too Much Cash. He summarizes the analysis of Jim Sloan, who concludes that Mr. Buffett should be buying back more stock. He compares the problem to that of the average investor. It is interesting and timely.

Watch out for…

Newspaper stocks. Warren Buffett says that the business is “toast.” Excellent data and interactive charts from the WSJ provide support. There is a big decline even for papers that have successfully instituted paywalls, and it is even steeper for regional papers.

Bets on robotaxis. Beth Kindig takes the role of myth-buster in this discussion of autonomous vehicles. There are implications for Intel (INTC) and Tesla (TSLA) among others.

Final Thought

This week I tried to emphasize the many attractive investment ideas. I encourage readers to take some time with these ideas. You will never have more facts available. While markets are hitting new highs, stocks are much more attractive than they were last fall. New highs are part of the process of any bull market.

Eddy Elfenbein noted the new information and updated the excellent results on his buy list. He wrote:

The takeaway is clear. All the doomsayers of a few months ago were overstating the case. The economy is still expanding, and markets are responding.

I have a continuing concern about investors who are taken in by stories designed to scare them witless (TM OldProf euphemism). These seem to fall into a few key groups:

- Economic data that are “decelerating” or “rolling over.” No economic series remains indefinitely at a peak. A “wave style” series is quite normal. If the economy was overly “juiced” after the tax cuts, it is no surprise to see it return to trend.

- Newly minted recession experts. I am absolutely dismayed at the Seeking Alpha Editor’s Pick on a story that has been on the front page for days – How the Next Recession Will Occur. It is a typical exercise in taking a pop economics concern – debt – and saying that it will all end badly. The author has no credentials in recession forecasting and no evidence for the causal reasoning. The leading email source of market commentary has been on this same theme for six weeks. The debt is a fact. The implications are conjecture. I often express concern about government debt. When I see it as a near-term threat to investors, you will hear about it. Meanwhile, beware of those who are just selling something.

- Fed bashers. They are back in action. As usual, some think that rates are too high, and others see them as too low. The nuanced argument is that the Fed missed the chance to raise rates earlier and now it is stuck. I am absolutely amazed at the number of people who claim to know more than all the Fed economists. A little peer review would go a long way.

The consequence is that many intelligent investors are being punished. In their professions they are rewarded for acquiring knowledge. In the financial world, they are punished, since the “knowledge” is bogus.

A final example from Dr. Brett’s NAAIM presentation, illustrating incorrect focus. He gave the example of a trader worried about a long-term matter like debt. Disaster. And also an investor glued to the trading screen. That doesn’t work either.

If you want to find long-term gains without guessing short-term timing, reach out to us. We have a great program for dependable and less risky income investment income. Send an email to main at newarc dot com. We’ll provide some helpful free information, and at your option, a no-charge portfolio consultation.

And also, some longer-term items on my radar

I’m more worried about:

- The ongoing drag from trade policy. This is happening so slowly that it is difficult to see. Meanwhile, the headline economic data has relieved internal pressure for a policy change.

- Post Mueller report politics. Needed compromises cannot happen with such intense partisanship. The latest likely victim is an infrastructure compromise – still at an early stage – that we highlighted earlier this week. Here is the actual story.

I’m less worried about

- Stock buybacks. Some of the reliably bearish clan claim that this is the only reason for the stock rally. Ed Clissold looks at alternatives, showing that the impact has been modest (5% since 2010), even if the alternative was holding cash. HT GEI and UPFINA.

- Disability insurance. Recent data show that a short-term fix bought more time to achieve solvency. (Timothy Taylor).

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits