Should High Yield Investors Be Concerned About ‘Fallen Angels’?

Earlier this year, our investment grade colleagues discussed the potential implications of the growing BBB segment of the US investment grade market (US investment grade credit: A buy or a bubble?). In high yield, we have also received questions regarding the growth of BBBs. In this blog, we address some important questions: Are we likely to see significant downgrades among these bonds into high yield territory (BB and below)? Would the high yield market be able to absorb these “fallen angels” and what would be the overall impact on high yield?

Are significant downgrades ahead?

We agree with our investment grade colleagues that most BBB companies will likely be able to de-leverage in the coming years and avoid downgrades. Increased leverage has not been driven by deteriorating operating results (which would concern us more) but by incentives created by central bank policies. Stimulative policies have made the cost of debt historically cheap, allowing companies to optimize their capital structures and reward equity holders with share buybacks, dividends and growth via mergers and acquisitions. Could there be some downgrades? We believe so, but we do not expect this behavior will lead to a massive wave of downgrades.

- What type of downgrade volume do we expect? Here’s how we estimate the possibilities: Moody’s average one-year rating migration rates for the past 35 years show the upper tiers of US BBBs (BBB and BBB+) experienced a 2.5% migration to high yield, on average, compared to around 9.5% for BBB- companies.1 Given this history, the Invesco Fixed Income High Yield team focuses on the “lowest-tier” BBBs (BBB-) for potential downgrades. The Bloomberg Barclays US Aggregate Baa Index currently contains just under $800 billion in market value of BBB- exposure.2

- During each credit cycle, there are always idiosyncratic issues that cause certain companies to be downgraded to below investment grade, but the market is currently concerned with the possibility of widespread downgrades due to slower economic growth. We believe the portion of BBB- companies likely to be most affected by slower growth are the highly cyclical sectors. We estimate the highly cyclical portion BBB- credits at approximately $460 billion in market value.3

- Applying the average historical migration rate of 9.5% to the highly cyclical BBB- segment suggests the potential for about $44 billion of high yield downgrades (peak year). Using the 2009 BBB- migration rate of approximately 14% (the highest during the global financial crisis) as a downside case, this implies $65 billion in potential rating downgrades.

We believe the high yield market could absorb these amounts, as discussed below.

Could the US high yield market absorb BBB downgrades?

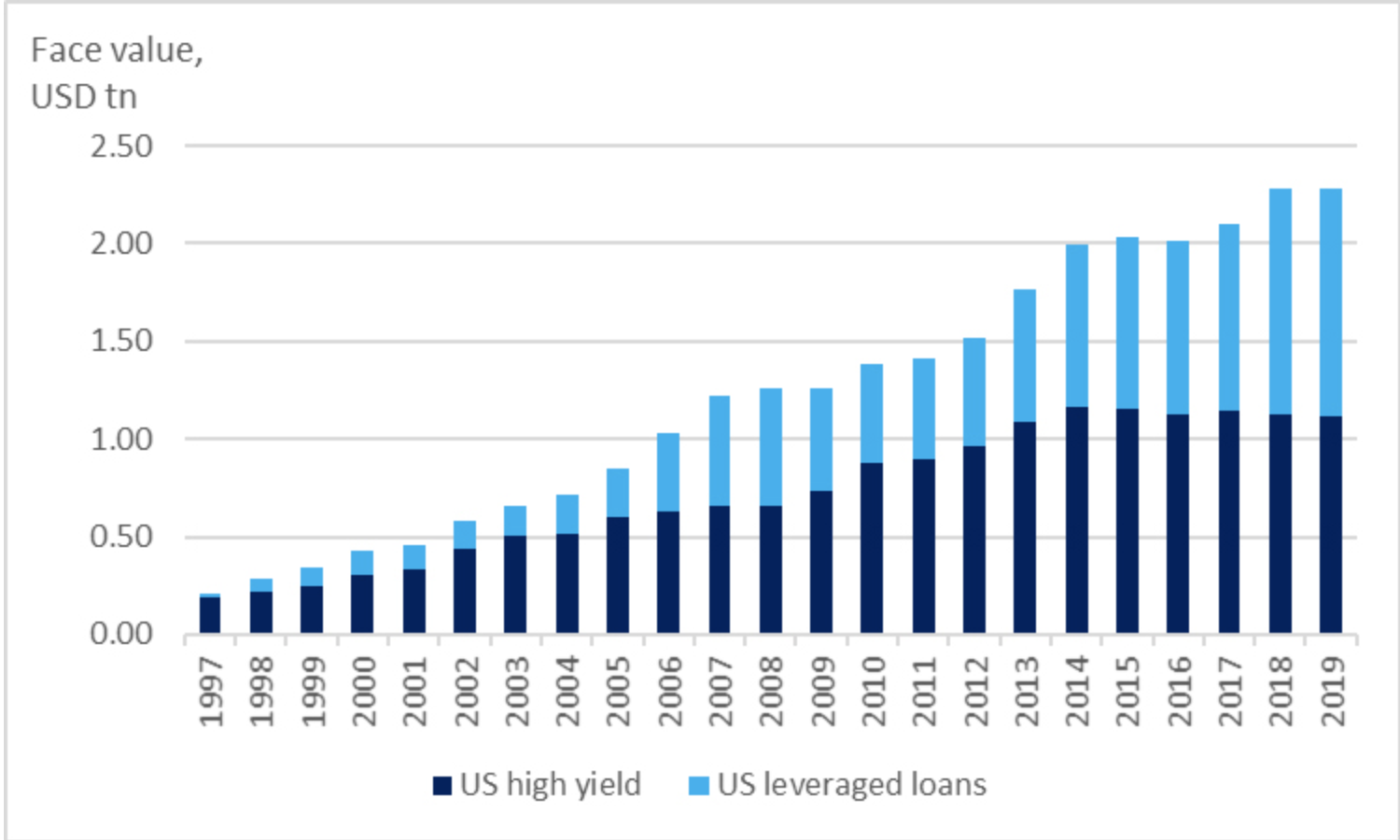

Much has been written about the shrinking US high yield market. The lack of new issuance and loss of share to the leveraged loan market are cited as factors potentially hindering the market’s ability to absorb fallen angels in the next downturn. We believe this concern is somewhat overblown. Figure 1 shows that the high yield bond market has not massively shrunk, but rather, the leveraged loan market has grown sharply. At the end of 2018, the US high yield market was only around $31 billion smaller than its peak of $1.16 trillion in 2014, equivalent to the outstanding debt of one large, high yield issuer.4

Partly feeding this perception was the fact that primary debt issuance was down in 2018 – totaling $187 billion compared to the trailing three-year average of $302 billion.5 Issuers have been opportunistic, choosing to tap the loan market due to strong investor demand for floating rate products and looser underwriting standards that have led to better economics for issuers. However, we view this as a cyclical phenomenon which is already reversing. Early 2019 has already seen multiple large, secured bond deals that likely would have been financed in the leveraged loan market a year ago.

We believe the entire leveraged finance market, including loans, must be considered when gauging the potential impact of fallen angels. The US leveraged finance market, including loans, totals over $2.2 trillion in size, which we believe is sufficient to absorb a potential uptick in fallen angels.6

Figure 1: Growth of US high yield bond and leveraged loan markets

Source: ICE BofAML US High Yield Index, S&P LCD, data from Dec. 31, 1997 to Jan. 31, 2019.

Expected impact on US high yield

The overall impact of fallen angels on high yield during a cycle downturn would be manageable for a few reasons, in our view. Historically, fallen angels have tended to experience the most spread widening prior to a downgrade, as investment grade investors rotate out of a name ahead of an announcement. In addition, a large portion of selling is due to forced sellers, often insurance companies facing higher risked-based capital charges for holding below-investment grade bonds. However, under new proposals that may be implemented in 2019, capital charges may be reduced on bonds downgraded one-to-two notches below investment grade, which may lead to less forced selling in a downturn.

Looking at historical experience, the last meaningful fallen angel cycle in the US occurred in 2016, with $142 billion in fallen angels, one of the largest years on record.5 Most of these downgrades were in the energy and materials sectors, driven by pressure on commodity prices. We do not expect such concentrated downgrades in the next cycle, even though the midstream sector is the largest within the lower-tier BBB market. We believe the market is more prepared for commodity volatility today than in 2016 and many BBB midstream companies would likely be able to maintain their investment grade ratings due to modest commodity exposure and strong cash flows. Moreover, even though the US high yield market experienced a heavy volume of fallen angels in 2016, it also posted the highest total return since the global financial crisis that year, with a total return in excess of 18%.7So, while we may see elevated fallen angel volumes in the next cycle downturn, we do not think it necessarily implies poor returns for the US high yield market.

Perspectives on European BBBs

As in the US, European BBBs have grown significantly post-global financial crisis. According to Barclays, BBBs have grown from EUR472 billion in 2013 to EUR907 billion in 2018.8 BBB corporates now represent about 50% of the Bloomberg Barclays Euro Aggregate Corporate Index.9 We also believe it is important to focus on the lowest-tier (BBB-) category, as this rating cohort is most likely to transition to high yield.

According to Barclays, since the end of 2012, the BBB- category has grown from EUR117 billion to EUR228 billion.10 Within the BBB- category, subordinated debt has exhibited the highest rate of growth. Subordinated debt is typically owned by investors with more flexible mandates than traditional investment grade investors, meaning they tend to be less affected by downgrades than traditional investors.

In Europe, the historical downgrade rate for BBB- corporate debt peaked at 13.7% during 2010-2015 according to Barclays.10 Applying this rate to EUR228 billion of outstanding BBB- debt implies potential downgrades totaling EUR31 billion, about 10% of the market value of the Bloomberg Barclays Pan-European High Yield Index.11 Notably, we use a peak historical downgrade rate in our calculation, which is higher than the often-cited, longer-term downgrade rate published by Moody’s. Furthermore, the BBB- category includes subordinated debt issued by higher-rated issuers that tend to have lower downgrade risk than BBB- issuers.

Overall, we think the European high yield market would be able to absorb fallen angels over time without much long-term impact to spread levels. In terms of concentration risk, we note that there is a large single financial issuer in the BBB- segment. If this paper entered high yield, it could be a challenge for the market to absorb because of its relative size and because there are fewer natural buyers of bank debt within the European high yield market.

1 Source: Moody’s, Annual Default Study, February 2019, Invesco.

2 Source: Bloomberg Barclays Aggregate Baa Index, February 2019, Invesco.

3 Source: Bloomberg Barclays Aggregate Baa Index, February 2019, Invesco.

4 Source: BofA Merrill Lynch Global Research, ICE Data Indices LC, S&P LCD, Invesco.

5 Source: JPM Annual Review, December 2018.

6 Source: BofA Merrill Lynch Global Research, ICE Data Indices LC, S&P LCD, Invesco.

7 Source: JPM US High Yield Index, Jan. 1, 2016 to Dec. 31, 2016.

8 Source: Barclays Credit Research ‘The BBBs of Damocles,’ Aug. 24, 2018.

9 Source: Barclays Euro Aggregate Corporate Index, Feb. 25, 2019.

10 Source: Barclays Credit Research ‘Who’s afraid of the triple-Bs?’ Jan. 18, 2019.

11 Source: Barclays Pan-European High Yield Index, Feb. 25, 2019.

Important information

Blog header image: Humannet/shutterstock.com

The Bloomberg Barclays US Aggregate Baa Index includes all of the corporate bonds in the Bloomberg Barclays US Aggregate Bond Index with Triple-B ratings. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS and CMBS (agency and non-agency).

The Bloomberg Barclays Pan-European High Yield Index measures the market of non-investment grade, fixed-rate corporate bonds denominated in the following currencies: euro, pounds sterling, Danish krone, Norwegian krone, Swedish krona, and Swiss franc. Inclusion is based on the currency of issue, and not the domicile of the issuer.

The Bloomberg Barclays Euro-Aggregate: Corporates bond index is a rules based benchmark measuring investment grade, EUR denominated, fixed rate, and corporate only. Only bonds with a maturity of one year and above are eligible.

Fixed income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Mike Kelley, CFA

Head of Global High Yield Research

Mike Kelley is the Head of Global High Yield Research within the Invesco Fixed Income High Yield team. He has research responsibilities for the aerospace/defense, airlines/rail/transportation, industrial and health care/pharmaceuticals sectors.

Mr. Kelley joined Invesco in 2013. He was previously at Allstate Investments for 12 years and most recently served as a senior analyst in their high yield and bank loan group. Mr. Kelley earned a BS degree in finance from Miami University. He holds the Chartered Financial Analyst® (CFA) designation and is a member of the CFA Institute.

Samira Sattarzadeh, CFA

Senior Analyst

Samira Sattarzadeh is a Senior Analyst with the Invesco Fixed Income High Yield team. She is focused on a variety of sectors including consumer goods, retail and utilities.

Prior to joining Invesco in 2013, Ms. Sattarzadeh was a lead credit analyst at Standard and Poor’s, specializing in consumer good companies. Prior to that, she served as an investment grade and high yield analyst at Western Asset Management Company.

Ms. Sattarzadeh earned a bachelor’s degree in economics from University College London. She is a Chartered Financial Analyst® (CFA) charterholder.