As the Friday early morning deadline (12:01 AM EST) expired, tariffs on an additional $200 billion of Chinese imports have technically gone into effect. However, as we go to press, negotiations are ongoing with the hope that a compromise can be brokered. However, rather than the “art of the deal” playing out, we are witnessing the “art of uncertainty.” The situation has grown more complex this week following President Trump’s Sunday tweet that not only threatened to raise tariffs from the existing 10% to 25% on $200 billion worth of Chinese goods but raised the stakes by potentially adding tariffs to an additional $325 billion dollars of Chinese imports at 25%. In total, that amounts to the potential of $575 billion in Chinese imports being taxed at 25% (~$144 billion or 0.7% of U.S. GDP). China’s threat to retaliate immediately with countermeasures (not yet specified) further clouds the situation. Admittedly, we have no additional insights other than what we have shared previously into what the endgame of these complex negotiations will be, however, we borrow a few points from “The Art of the Deal” to gain some additional insights:

- Think Big | In “The Art of the Deal,” Trump suggests “think big.” The negotiations between the U.S. and China impact the two largest economies in the world, representing ~40% of the global economy. With Europe and Japan next on the docket with the May 18 deadline for President Trump’s decision regarding tariffs on auto imports, that is an additional ~25% of the global economy. In total, we are dealing with approximately two thirds of the global economy when it comes to trade conflicts—that is big! As a result, an unfavorable outcome—a prolonged trade war—would place downward pressure on our global economic growth forecasts.

- Fight Back and Leverage | Trump’s belief that the U.S. has been treated unfairly and has been taken advantage of in regard to trade has led to his administration’s more aggressive stance. The U.S. is the largest, single most important and robust “goods” market in the world and access to it is critical for many companies around the world—a point brought up by U.S. negotiators. However, geopolitical and financial leverage is an important dynamic China has to play. China has supposedly been helpful with the North Korean nuclear discussions, has competing interests when it comes to Venezuela and Iran, and remains the second biggest holder of U.S. Treasury bonds (behind the Federal Reserve). A more cordial relationship between the two biggest economies in world could lead to a more collegial effort with many geopolitical hotspots in the world.

- Protect the Downside and the Upside Will Take Care of Itself | This may be the most important point of the book and the reason we believe a compromise will eventually be agreed upon to avoid significant trade disruption. The President needs a win to protect his downside, which is to keep the U.S. economy strong in order to bolster his re-election aspirations in 2020. Weakness in the economy, particularly from middle America (and farmers) would likely hurt his strong approval ratings on handling the economy. Similarly, China needs to maintain its momentum as the recent soft patch that they have experienced has not been viewed favorably by the government and its people. Both leaders have a strong desire to win and portray strength on a global stage and a compromise would allow both to do so.

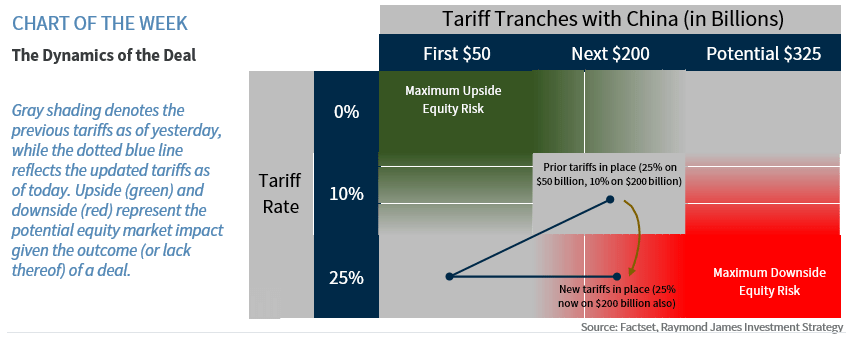

Will a Deal Be Struck? As we wrote yesterday, we remain optimistic a deal will eventually be struck (not necessarily today). However, with the uncertainty surrounding the outcome, we continue to believe the table below illustrates the likely direction of the equity market given various outcomes. The tariffs in place as of yesterday are represented in gray. An increase in tariffs, effective this morning as the $200 billion tariffed at 10% has gone up to 25%, are a headwind for the equity market and is likely to cause some downward pressure as long as they remain in effect. Should those tariffs be reversed or reduced, that could lead to upside pressure in the equity market whereas an increase in tariffs (the potential $325 billion tranche) could lead to further downside pressure. The timing and enforcement of these tariffs will similarly play a role in the market response. Regardless of the outcome, this topic is likely remain in the forefront for the foreseeable future as President Trump ramps up his re-election campaign.