EXECUTIVE SUMMARY

The duration and magnitude of value’s recent underperformance has caused many to ask once again if value investing is no longer effective. While it is possible that secular shifts have helped to compress value’s premium relative to its long-term history, we believe most of the recent decline can be traced to more transitory factors. Our research indicates that value’s underperformance has stemmed from multiple factors including, among other things: a smaller relative income benefit; less tailwind from rebalancing; and an increasing discount to the market. We also believe that even if the normal value premium has compressed, value is currently priced to outperform across all regions.

Overview

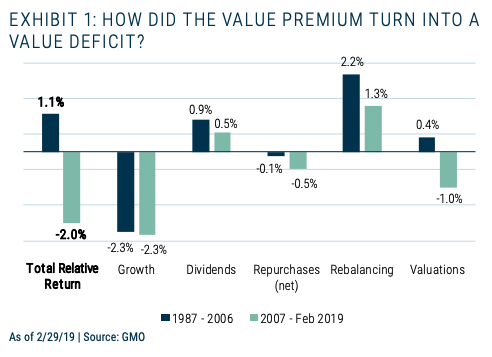

2018 marked another year in which U.S. value stocks underperformed relative to the market (and, of course, growth stocks). Value stocks have trailed the market in 9 of the last 12 years by an average of 2.0%1 per year. This value deficit during this most recent cycle stands in contrast to the long-run premium generated by buying cheap stocks.2 Decomposing returns suggests the value premium stems from multiple drivers of relative performance and recent underperformance comes from a variety of those sources, not one sole culprit. We believe many of these effects have been time-specific and will revert to value’s favor, making this a particularly attractive time to lean into the value style. To be fair, our research suggests some historical value drivers may in fact provide less benefit going forward. This combination leaves us confident that value stands well-positioned over the mid term, but may not be able to match its historical levels of outperformance over the longer run.

This note, in which we analyze the drivers of value’s historical outperformance, is intended to serve as an appetizer to a more comprehensive research paper my colleague John Pease will be publishing soon. John’s work suggests that value’s recent underperformance is not due to an erosion in the fundamental growth of value stocks. Value fundamentals – the group’s historic level of under-growth – have been consistent with history. Instead, value stocks have accrued less benefit from higher relative income and the rebalancing effect. Moreover, value has experienced a negative valuation impact because cheap stocks have not seen their multiples expand as much as the broad market during this recent cycle. As a result, we believe value stocks are priced to outperform across all regions.

First, why does value work?

By definition, value stocks trade at a discount to the market. The value universe comprises companies with lower-than-average fundamental growth, causing investors to demand a discounted valuation. Investors systematically underestimate the ability of weaker and distressed companies to mean revert to profitability and reasonable growth levels. Instead, they overpay for growth by extrapolating relatively strong growth too far into the future. Historically, buying companies with low price multiples has delivered substantially better returns than the overall market, with the added benefit of lower absolute volatility. From the inception of the Russell 3000 Value index through 2006, value stocks outperformed the broad market in the U.S. by 1.1% per year starting in 1978. While value companies did in fact under-grow the market, their cheaper valuations, higher yields, and a number of other factors more than made up for their weaker fundamentals.

Over the past 12 years, however, value stocks have underperformed, leaving many to ask whether the value premium is gone (see Exhibit 1). Let’s answer that question by starting with what we know hasn’t been the issue in the decline.

Fundamental growth continues to lag the market… as it always has

As the chart above indicates, value company fundamentals (sales, gross profit, and book value) have grown 2.3% more slowly than the broad market since 2006.3 This level of undergrowth was to be expected and was in line with the group’s long-term history. As value’s fundamentals were neither better nor worse than history, other return drivers must explain underperformance over the past decade.

Income advantage is lower in an expensive market

One way value stocks have outperformed over the long run is by offering higher than market yields. That advantage diminishes in an expensive market like today’s. If the broad market traded at a 4% yield with value stocks offering a 50% yield premium, the yield on the value universe would be 6%. Cheaper valuations allow the value cohort to offer 2 points of additional yield, a helpful offset to value’s historical undergrowth. If the market doubled (and value retained its 50% yield advantage), the 2% of extra yield from value falls to a less attractive 1% advantage (with the market yield falling to 2% and value to 3%). In an expensive market, value’s yield advantage compresses. This has certainly been the case over the last 12 years, particularly in the U.S., where the market has been quite expensive. The combination of dividends and share repurchases provided 0.8% less relative return for value stocks compared to its longer history. Our base case equity forecasts assume multiples mean revert to long-term historical averages. If, however, markets have in fact entered a new secular paradigm with higher price multiples lasting in perpetuity, the overall value premium would be lessened due to a smaller income effect.

The value universe has benefited less from rebalancing

Value stocks typically benefit when companies with clouds hanging over them improve operations or experience a cyclical recovery, strengthen their fundamentals, and see their multiples expand. As valuations rise, some value stocks graduate from the value to the growth universe. Value investors benefit by selling the more expensive stocks as they leave the group while simultaneously picking up the growth companies that have recently disappointed and thus trade at cheaper levels.4 That turnover, or rebalancing effect, has been a big plus for value over the years, contributing 2.2% of value’s return premium.

Over the past decade, this rate of shift has slowed to 1.3%. This reduction in the dynamism of these groups has been particularly striking within the expensive half of the market, which is a good proxy for growth companies given investors tend to pay higher multiples for faster growth. Of late, expensive stocks have remained expensive for longer than usual. Typically, high growth companies are unable to sustain excessive growth rates for long periods. In the last decade, however, the growth universe has been more retentive than in the past. A handful of companies, including Facebook, Alphabet, and Amazon, have managed to grow at high rates for long periods. The question is whether this will be true going forward. Certainly, for the FAANGs5 themselves, they will eventually hit limitations to growth. Facebook and Google are, after all, advertising companies. Advertising tends to grow in line with GDP. If those two companies captured 100% of advertising spend, they would stop growing faster than GDP. Even for the champions of the last cycle, growth will become harder to come by. There is no question that the FAANGs have defied the historical growth slowdown associated with very large companies to date. Value bears (really growth bulls) would argue that the growth universe has become more concentrated and competitive, leaving value companies at a structural disadvantage. Our best guess is that today’s champions are much closer to the end of their growth than the beginning of it as all things reach limits to growth eventually.

My colleague Ben Inker also points out that the rebalancing effect may be further boosted by a higher incidence of takeover targets within the value universe. However, the recent combination of low interest rates, accommodative debt markets, and sluggish growth has led CEOs and private equity investors to buy more growth companies than in prior cycles, reducing the takeover premium bias in favor of value. Should interest rates and credit spreads normalize, we would expect levering companies with limited to no cash flow will become more difficult. In the long run, more takeovers should come on the value side than on the growth side.

Relative valuations are the final culprit...and much of the opportunity ahead

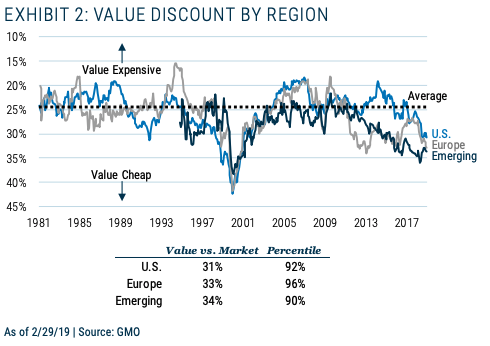

The final puzzle piece behind value’s recent underperformance is valuations: value stocks always trade at a discount to the market, but the magnitude of the discount goes through cycles. Value multiples have not expanded as strongly as those of their growth counterparts since 2006, leaving value meaningfully cheaper than the broad market today. While the length of value’s underperformance in this cycle has been notable, value has experienced similar levels of underperformance in the past. Value spreads are not at the extreme levels of the late 1990s, but they do suggest value is well-positioned across all regions. Per Exhibit 2, value stocks typically trade at a 24% discount to the market; today they are trading at 30-35% discounts across different regions. Even if the normal value premium has compressed, value deserves to outperform at these levels.

Conclusion

We believe that value will continue to exhibit the same characteristics it has historically: lower growth, higher yield, and positive return from multiple expansion and rebalancing. After losing 1% per year over the last 12 years as value stocks cheapened relative to the market, they are currently trading at abnormally wide discounts that should provide helpful tailwinds going forward. The increasing cheapness of value will reach a limit at some point. Given value’s relative growth has not deteriorated, we do not see any fundamental reason value stocks deserve to trade cheaper than they normally have. Even if the relative cheapness of value does not revert but simply stops widening, value stocks should outperform thanks to its other drivers of return. From a cyclical perspective, value globally is priced to win.

Investors should, though, be skeptical of investment strategies based on a rigid and simplistic definition of value like price/book value. Book value is an accounting measure meant to represent capital, but a gap between accounting and true “economic” capital has developed as business models have evolved. While reported book value worked well historically, it no longer reflects the underlying economic reality for many companies. Businesses have become less industrial and comprised of hard assets and more service-oriented with intangible assets, which are more difficult to value. Studious active managers can account for this migration while most passive value approaches fail to do so.

Value investing may be more mature and running at a slower pace than in its youth, but it is far from having one foot, if not both, in the grave. Many of the factors that have hurt value over the last decade or so do not seem likely to have been permanent shifts. It is possible certainly that the average value premium will be lower than history.6 Or just maybe, value’s current attractive relative price will enable it to outperform while facing a combination of helpful and harmful forces.

Rick Friedman

Mr. Friedman is a member of GMO’s Asset Allocation team. Prior to joining GMO in 2013, he was a senior vice president at Alliance Bernstein. Previously, he was a partner at Arrowpath Venture Capital and a principal at Technology Crossover Ventures. Mr. Friedman earned his B.S. in Economics from the University of Pennsylvania and his MBA from Harvard Business School.

1 As measured by the Russell 3000 Value index vs. the Russell 3000 index for the 12 years ended 2/28/19.

2 12/29/78 through 12/29/06. We chose to analyze value’s recent cycle beginning in 2007 to capture a full cycle rather than looking back a decade, which would capture a trough to peak period.

3 Our decomposition of returns analysis above commences in 1987 (rather than 1979 when the Russell 3000 Value index started) due to the prior lack of availability of monthly constituent data.

4 As we will explore in an upcoming note, the reduced rebalancing effect is really a combination of three factors including: 1) stocks rotating less between value and growth; 2) the valuation gap between securities exiting and joining the value group becoming more compressed; and 3) the correlation of rotation volume and valuation spreads dropping.

5 This group includes Facebook, Alphabet, Amazon, Netflix, and Google.

Disclaimer

The views expressed are the views of Rick Friedman through the period ending May 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2019 by GMO LLC. All rights reserved.

© GMO

More Fixed Income Topics >