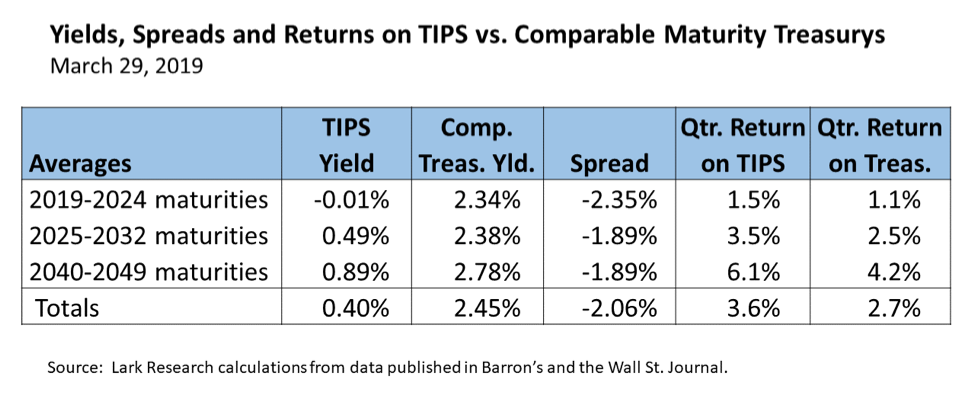

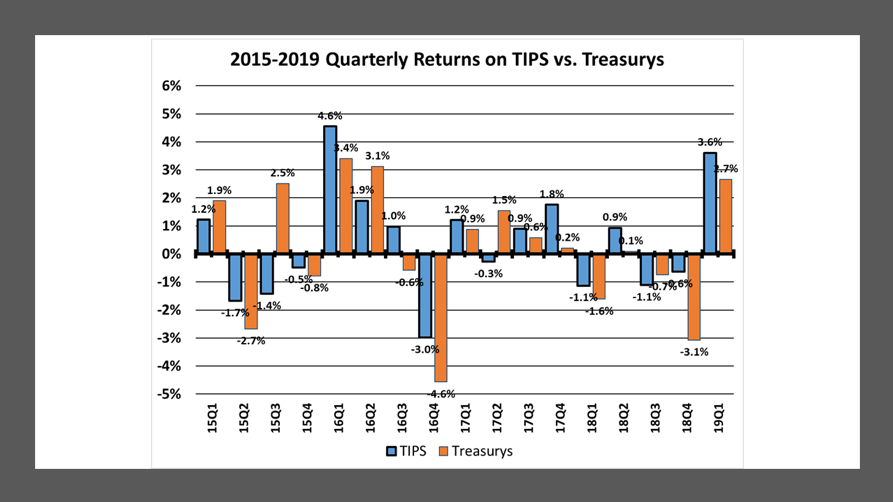

Treasury Inflation-Protected Securities outperformed comparable maturity straight Treasurys to a surprising degree in the 2019 first quarter. On average, TIPS earned an annualized return of 3.6% in the quarter, better than the 2.7% return on straight Treasurys.

The outperformance was achieved despite a negative inflation adjustment – i.e. a reduction in the principal of the bonds due to the decline in headline CPI. The average TIPs bond lost 0.5% of principal or $5 per $1,000 of par value in the quarter. The percentage loss was equal to the change in the CPI from October to January.

During the quarter, the average yield on TIPS bonds declined by 94 basis points (bp) to 0.40%. Short-term TIPS experienced the greatest reversal in yield, falling from 2.07% to -0.01%. Short-term TIPS yields are especially volatile because comparatively small changes in the prices of those bonds usually have an outsized effect on annualized yields. Yields on intermediate- and long-term TIPS decline by 49 bp and 31 bp, respectively (to 0.49% and 0.89%).

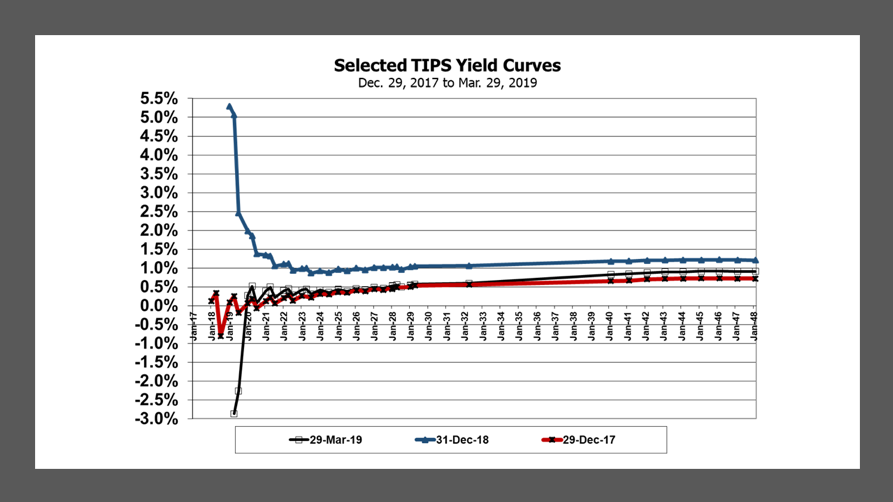

The volatility in short-term TIPS yields is evident from a look at shifts in the TIPS yield curve over time.

The chart above shows the significant shift in the short-end of the TIPS yield curve from Dec. 31, 2018 to Mar. 29, 2019. Over that period, the yield on the shortest-dated TIPS bond fell from 5.29% to -2.87%. (As noted, because the maturity of those bonds was only weeks away, even modest moves in price will have a significant impact on yield.) Nevertheless, the sharp move in the shortest maturity TIPS bonds and other bonds with nearby maturities does reflect a change in investor focus, which I believe is driven by expectations of near-future changes in the CPI.

Farther out on the TIPS yield curve, the changes in yield have been more muted, but still significant. From year-end 2018 to the end of the March 2019 quarter, the yield on four-year TIPS fell 55 bp to 0.44%, while the yield on longest maturity (28-30 year) TIPS declined 30 bp to 0.91%.

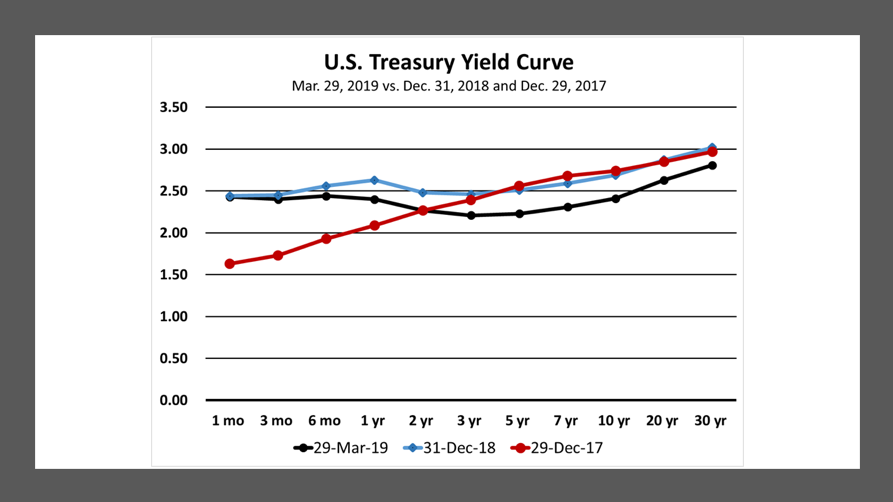

Straight Treasury yields also declined, but much more modestly. The average Treasury yield eased 21 bp to 2.45%. Short-term yields slipped 17 bp, anchored by Federal Reserve policy. Intermediate- and long-term Treasury yields declined 23 bp and 21 bp, respectively.

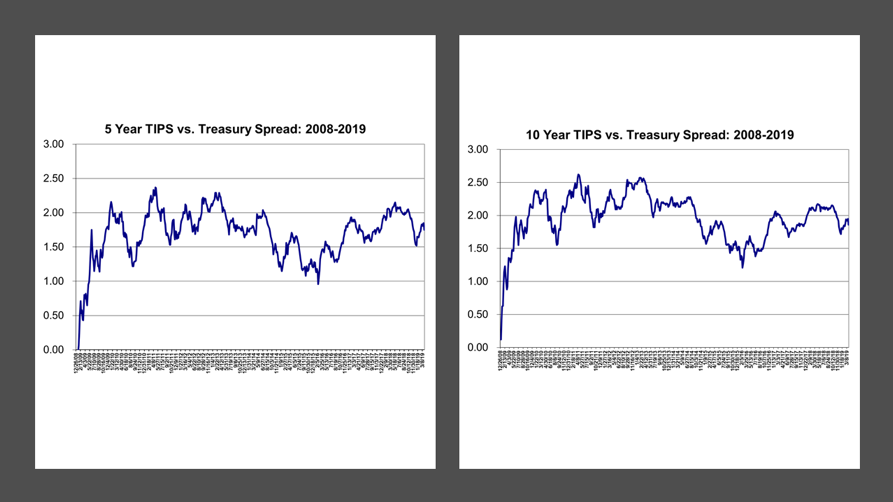

The more muted changes in Treasury yields caused the spread between TIPS yields and Treasury yields to widen by 74 bp from 132 bp in the 2018 fourth quarter to 206 bp in the 2019 first quarter. The spread measures the breakeven or average expected inflation rate. (It is called the breakeven inflation rate because if achieved, investors would be indifferent to owning TIPS or straight Treasurys. If actual inflation turns out to be higher than the spread, investors would prefer to own TIPS. On the other hand, if actual inflation is lower than the spread, they would prefer to own Treasurys.)

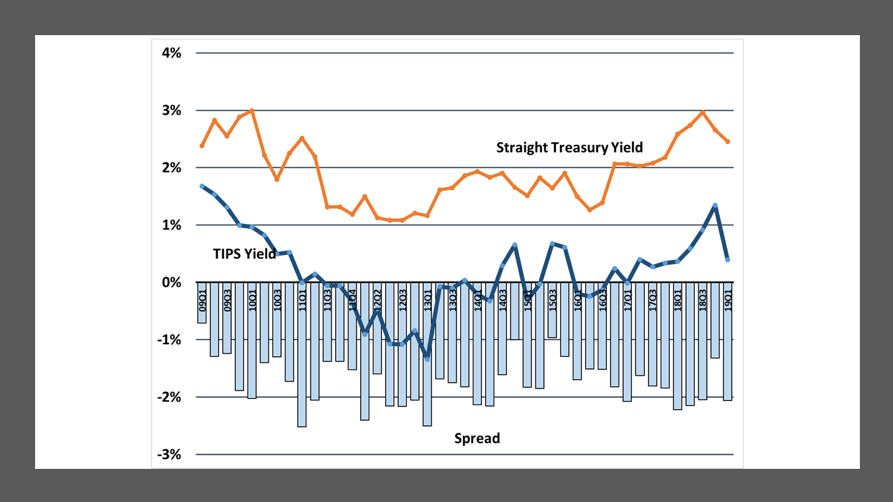

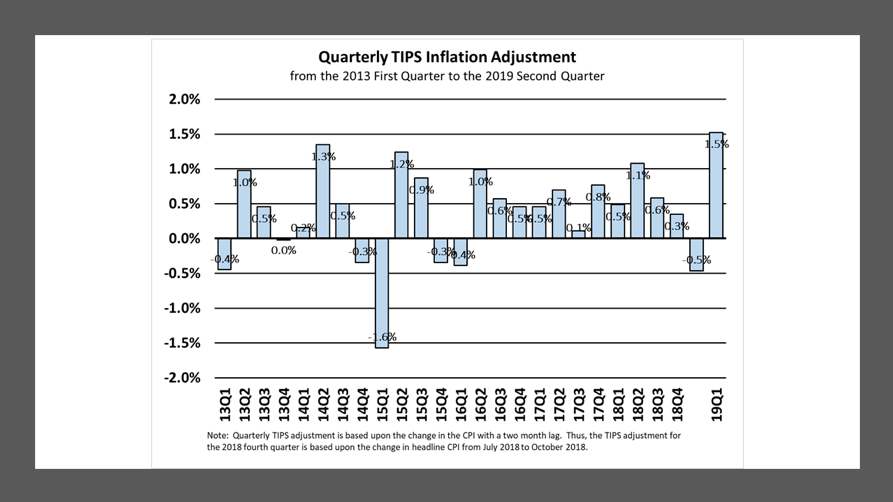

Since 2009, when I began following the TIPS market, the TIPS-Treasury spread has averaged 175 bp. More recently, there has been volatility around that average. The average spread whipsawed from 205 bp at the end of the 2018 third quarter, down to 132 bp in the fourth quarter and back to 206 bp in the first quarter. This volatility has coincided with the change in inflation adjustment on TIPS (which is determined by the change in the benchmark CPI). The inflation adjustment has fluctuated from an increase of 0.58% for the 2018 fourth quarter to a decline of 0.49% in the 2019 first quarter and will rise to an increase of 1.52% for the upcoming 2019 second quarter. (The inflation adjustment is determined by the quarterly change in the non-seasonally adjusted headline CPI with a two-month lag, so the market gets an advance read on the near-term inflation adjustment.)

It seems therefore that TIPS market is reacting quickly to the changes in the inflation adjustment by bidding up or down short-term TIPs. At the end of the 2018 fourth quarter, the average short-term TIPS yield was bid up to 1.34%, the highest level since 2009. (i.e. investors sold short-term TIPS, which caused the increase in the yield). This rise in the TIPS yield coincided with the knowledge that the inflation adjustment would be negative in the 2019 first quarter.

But then by the end of the 2019 first quarter, the average short-term TIPS yield was bid down zero, probably because investors knew that the inflation adjustment would be 1.52% for the upcoming second quarter. (By the way, that 1.52% positive inflation adjustment will be the highest since 2011.) Thus, short-term oriented investors seem to be quick to accept lower TIPS yields when they know that the near-term inflation adjustment will be high, but require higher yields when the upcoming inflation adjustment will be low.

The recent gyrations in the inflation adjustment have been due primarily to the impact of changing energy prices (most notably gasoline) on inflation. The price of West Texas Intermediate crude oil fell from a peak of $77 per barrel in October to a low of $42 in December and has since rebounded to $63. Gasoline prices have followed those moves with a short lag. During this period, so-called core CPI has been well-behaved and has even eased slightly over the past few months. Despite the volatility in headline CPI, there has been no indication of a meaningful change (i.e. increase) in the underlying rate of inflation or in inflation expectations.

Nevertheless, the recent volatility is a potential warning sign. From a technical (analysis) perspective, volatility in a security, stock index or commodity often precedes a major move. While the recent volatility in oil and gasoline prices and short-term TIPS yields has played out over a fairly long, six-month time frame, it could conceivably be a precursor to a change in the market environment, which might be a pick-up in inflation.

Market performance during the 2019 first quarter has changed the value proposition of TIPS versus Treasurys. It is unusual for TIPS yields to fall when TIPS spreads are rising. The widening of the TIPS spread heralds a return of expectations to the longer-term trend of 2% inflation, but the decline in the TIPS yield equates to a decline in the real rate of interest from 1.34% in the 2018 fourth quarter to 0.40% in the 2019 first quarter. As of the end of March, the market was demanding a lower real rate of interest, even though inflation expectations had risen.

The end-of-March TIPS yield is still above the post-financial crisis average of 0.16%. That very low long-term average real rate of interest occurred during a period of very low and stable interest rates, with short-term interest rates hovering near zero. On the other hand, the 2019 first quarter decline in the average TIPS yield comes in the aftermath of Federal Reserve tightening and general expectations that interest rates will or should be returning to normalized levels. Certainly, there is considerable skepticism about whether the Fed will be able to hold the Fed Funds rate at its current level. Futures markets anticipate a high probability of a rate cut by the end of 2019 or the beginning of 2020.

While there are a number of factors that determine the real rate of interest, a chart contained in a 2016 study by the Federal Reserve Bank of Minneapolis1 showed that real interest rates were sharply negative in the late 1970s when inflation was rising and they became significantly positive when inflation was falling. (During that period, changes in nominal interest rates apparently lagged changes in inflation.)

Yet, real rates (and thus TIPS spreads) can also be affected by short-term market dynamics. During the 2008 financial crisis, for example, TIP spreads across the yield curve were driven to zero – i.e. there was essentially no difference between yields on TIPS and straight Treasury – because some investors sold TIPS indiscriminately in order to raise liquidity. Although spreads rebounded quickly in the aftermath of the crisis, it is unclear whether that dynamic will prevail in the next financial crisis (if we should ever have one).

For these reasons, I believe that low implied real rate of interest on TIPS provides very little room for error. In my view, straight Treasurys represent a better relative value than TIPS, even though I recognize that at their current low yields, straight Treasurys are also exposed to potential losses from future increases rate increases.

For the time being, though, calm has returned to the TIPS and the broader Treasury markets. Since the end of March (to May 21), TIPS yields are up 7-10 bp, with short-term yields up 10-15 bp, medium-term TIPS yields up 5 bp and long-term TIPS yields essentially flat. Meanwhile, straight Treasury yields are also little changed, with declines of a few basis points in the short-end of the yield curve and increases of a few basis points in the long-end. Thus, TIPS-Treasury spreads have narrowed slightly across the short maturities but risen by an even smaller amount across the long maturities. For the time being, the TIPS and Treasury markets seem to have found equilibrium.

May 22, 2019

Stephen P. Percoco

Lark Research

839 Dewitt Street

Linden, New Jersey 07036

(908) 448-2246

[email protected]

www.larkresearch.com

Lark Research is an independent investment research provider founded by Stephen P. Percoco in 1991. Research coverage includes stocks and bond in industries such as real estate, utilities, oil & gas, telecommunications, industrials, consumer goods and materials. Prior to founding Lark Research, Steve served as Vice President in High Yield Corporate Bond Research at Salomon Brothers and as an investment officer at Bank of Boston. He is a graduate of Bowdoin College and Harvard Business School.

1 Real Interest Rates over the Long Run, by Kei-Mu Yi and Jing Zhang, published Sept. 19, 2016 and available at https://www.minneapolisfed.org/research/economic-policy-papers/real-interest-rates-over-the-long-run

© Lark Research

More Tax Planning Topics >