As we celebrate the long Memorial Day weekend, Investment Strategy would like to take the opportunity to remember, honor and thank all of the members of our armed forces who gave their lives in service to our country. We hope everyone is able to spend quality time with loved ones and we wish you and your family a healthy and restful holiday.

Memorial Day is also the “unofficial” start to summer as the temperature heats up, school ends, and vacation season begins. In fact, the volume of miles driven in the U.S. moves up dramatically between Memorial Day and September’s Labor Day (the “unofficial” end to the summer). With more people on vacation there is a tendency for investors to lose focus on the financial markets. However, this particular summer presents numerous events, deadlines, and potential headlines that we believe investors cannot ignore as they could lead to increased volatility, both to the upside and downside. Some of these include:

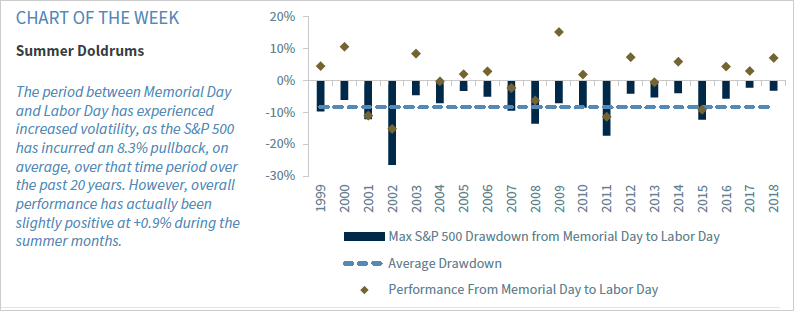

- Summer Softness | Historically, the summer months have not exhibited the strongest seasonal performance. In fact, they have suffered an average drawdown (e.g., peak to trough) of 8.3% and at least a 5% pullback ~70% of the time over the last 20 years. However, pullbacks are expected as the S&P 500 sits ~3% off its record high and the market has yet to experience a 5% pullback year-to-date (YTD). Keep in mind the S&P 500 historically experiences at least two 5% pullbacks, on average, in a given year. Most of these pullbacks represented a buying opportunity as the average return over these summer months has been +0.9%.

- “Deal” or “No Deal” Trade Agreement | Daily headlines and dramatic statements continue to dictate market movements. But that talk may potentially turn into concrete action in June with three key dates: June 1 (the day Chinese tariffs are implemented on $60 billion of U.S. exports); June 24 (when the U.S. could outline an additional $325 billion worth of Chinese imports to be tariffed); June 28-29 (the potential face-to-face meeting between Presidents Trump and Xi at the G-20 summit in Japan). The recent muted equity response to the trade escalation suggests to us the market is in a wait-and-see mode, with the outcome binary. A trade truce would likely send equities, especially emerging market (EM), higher whereas disappointment could lead to an additional 5% to 10% decline.

- Follow the Dot: Fed Meeting | The next Federal Open Market Committee (FOMC) meeting will be held June 18-19, which will include an interest rate decision, updated economic forecasts (including the dot plot) and the chairman’s press conference following the meeting. The previous dot plots suggested that the Federal Reserve (Fed) expects to remain on hold through year end. However, the market is currently pricing in an 81% probability of a rate cut by year end. As the Fed continues to reiterate (as evidenced through the minutes from the May FOMC meeting released this week) that it expects the moderation in inflation pressures to be ‘transitory’, the market may come under pressure if the Fed does not lower its inflation forecast or if it leaves its interest rate forecast unchanged (e.g., no rate cut). Given the ongoing debate about inflation and the direction of interest rates, the Fed’s Symposium in Jackson Hole (late August) may provide additional insight (especially if European Central Bank President Mario Draghi’s successor is in attendance).

- Earnings Downside or Déjà Vu | Similar to the first quarter, second quarter earnings are flirting with negative territory as 2Q19 S&P 500 earnings are expected to decline 0.6% year-over-year (YoY). As earnings are historically revised lower an additional 1% from now until the start of the earnings season, consensus forecasts could be in solidly negative territory when we begin 2Q19 season in early July. However, assuming the average “beat” rate, the S&P 500 should once again avoid a negative quarter. But as trade uncertainty has increased and multiple multi-national companies have expressed concerns over the tariffs, negative forward guidance or commentary from management could result in equities moving lower from current levels.

- No Shortage of Domestic and International Risks | While Congress may be on recess, the presidential race will heat up with the first Democratic primary debate on June 26-27. In addition to the festering tensions with Iran and Venezuela, the OPEC meeting on June 25-26 could prove to be a positive catalyst for oil prices if current quotas are maintained by OPEC members.