The “inconvenient truth” of equity market pullbacks is that investors tend to want them in order to invest at more favorable prices, but when they actually occur, investors get nervous, question their conviction and postpone their purchases. As we have mentioned in recent Weekly Headings, we had grown more cautious on the equity market as the S&P 500 matched our year-end target of 2946 on April 30. We believed the S&P 500 had gotten ahead of itself and suggested that the combination of investor complacency and weak seasonality would likely lead to a modest pullback. As a result, we had targeted the 2800 (5% upside) and 2700 (~10% upside) levels for the S&P 500 as potential buying opportunities. As we wrote last week, despite the vacation and summer fun between the Memorial Day and Labor Day holidays, investors need to remain engaged and patient with the market as a pullback would likely provide an “inconvenient opportunity.” Some of the reasons we believe weakness should be bought include:

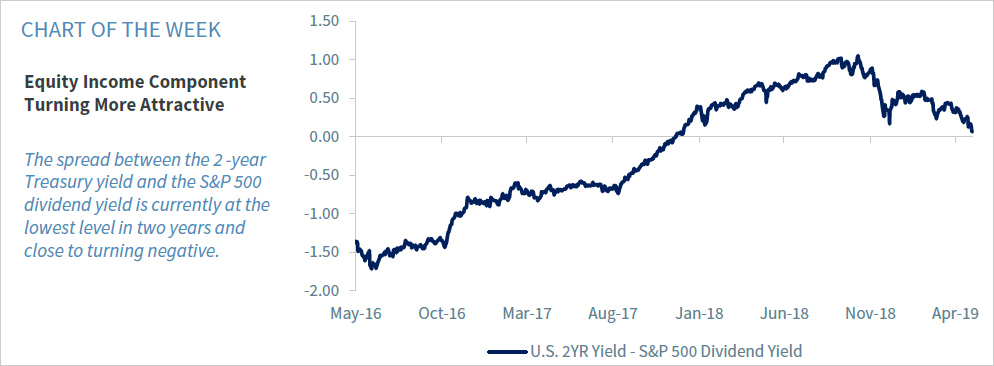

- Bottoming Bond Yields? | The 10-year Treasury yield fell to year-to-date (YTD) lows (2.17%). There is no doubt that Treasuries have served their purpose as a portfolio diversifier amidst the recent uptick in volatility as longer duration Treasuries have significantly outperformed equities by ~800 basis points (bps) since April 30. However, bonds are not without risk as low interest rates (and high duration) make them susceptible to unfavorable performance if interest rates bounce from current levels. While we are not suggesting selling your bond exposure and violating your asset allocation strategy, we would note that the 5.8% upside for the equity market to our year-end target is better than the –5% performance if rates rise 50 bps (consistent with our 2.75% 10-year Treasury forecast) between now and year end. Equities are now particularly attractive relative to bonds as the spread between the S&P 500 dividend yield (+1.9%) and the 2-year Treasury yield is at the narrowest spread (~6 bps) in two years.

- Earnings Valuations | S&P 500 earnings forecasts have stabilized and the consensus has slowly come down to our once considered conservative estimate of $166/EPS for 2019 S&P 500 earnings. More importantly, 2020 earnings are expected to be even better than 2019’s as they notch another record high (current consensus $186). Given our fair market P/E estimate of 17.75x against the current economic, interest rate and risk environment backdrop, the current P/E (on 2019 earnings) of 16.75x is relatively attractive.

- Cash Firepower | The amount of cash in money market accounts is $3.13 trillion, the highest level YTD and the highest since 2010. As that money is deployed and finds its way into the equity market, it should support higher equity prices.

- Changing Temperament | The American Association of Individual Investors’ Bullish Sentiment indicator has fallen to its lowest level since December and the second lowest level over the last two years. Meanwhile, the Bearish Sentiment indicator has skyrocketed to its highest level since January. Historically, sentiment indicators are a contrarian indicator.

- Shifting Fed | While we still believe it is too early to pencil in a Fed rate cut by year end, the bigger story is that the Fed is mindful of the burgeoning risk to the economy from the protracted trade friction and stands ready to cut rates, if necessary. More importantly, by our metrics, while growth is likely to slow in the second quarter (Atlanta Fed GDPNow 1.26% and NY Fed Nowcast 1.41%), there remains a low probability of a recession over the next 12 months.