Congratulations to the defending World Cup champion U.S. Women’s National Soccer Team for an impressive opening game victory in this year’s tournament in France. By defeating Thailand 13-0 this past Tuesday, they set the largest margin of victory in Women’s World Cup history. Despite the strong start, we implore the team to remain focused and not become complacent. Upsets are a part of sports as witnessed by Buster Douglas knocking out Mike Tyson, UMBC beating Virginia in the basketball tournament last year, and of course, the Miracle on Ice of the U.S. men’s hockey team. Guarding against overconfidence is paramount not only in sports, but also in managing the economy and portfolios.

- Fed Finesse. As we expect the Women’s National Team to continue pushing for the World Cup, we expect the Federal Reserve (Fed) to take the necessary measures to extend the current record expansion. With the U.S. economy slowing from its robust 3.1% pace in Q1 due to trade headwinds, slowing global economic momentum and the yield curve inverting for the first time since 2008 (the 10-year and 3-month maturities), calls from the “vuvuzelas” to cut rates have grown louder. In fact, the futures market is now pricing in a 99%, 89%, and 56% probability of one, two, and three Fed rate hikes by year end. While the market is on a “break-away” path to multiple rate cuts, next week’s Federal Open Market Committee (FOMC) meeting looms large as market expectations may have gotten too far ahead of the Fed. That meeting includes an official statement on monetary policy, an update to the Fed’s economic forecasts (including the “dot” plot), and a press conference by Chair Powell. Even though recent Fed speeches have turned more “dovish,” the focus will be on whether the Fed’s new verbiage, forecasts, and dot plot match the aggressive downward path in interest rates that the market is anticipating. Unless the Fed markedly lowers its growth forecasts (because of global growth concerns) or changes its “transitory” low inflation expectations, the markets may very well be disappointed by the Fed being more patient and not matching the multiple rate cut expectations. The worst case scenario (unlikely) is that the Fed insinuates there are no interest rate cuts on the horizon.

-

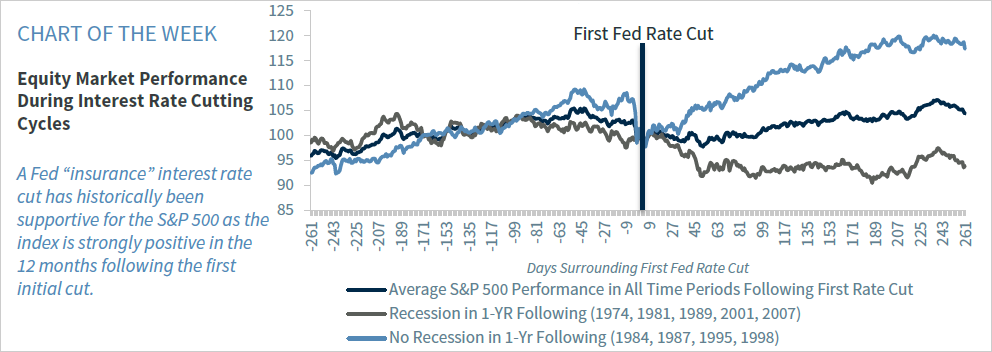

Pragmatic Game Plan. Regardless of the outcome at the Fed meeting, our economist believes the Fed will cut interest rates two times this year, likely in July and October. As a result, our game plan for the equity market remains consistent. As the S&P 500 moves above 2900, we become more cautious and as it falls below 2800, we nibble and get more aggressive as it approaches 2700. As a result, if the Fed finesses a perfect market-friendly message and the market rallies above 2900, we would fade the rally, and, if it falls, we would use it as a buying opportunity. From a historical longer-term perspective, the path of the equity market is dependent on the success or failure of the cuts and whether the economy enters a recession.

- Success: Insurance Policy. If the cuts act as an insurance policy to preserve and extend the expansion, the equity market is likely to continue to move higher. As an example, the Fed cut rates in slowing, yet non-recessionary environments in 1984, 1987, 1995, and 1998 and the economy continued to expand for a number of years. Given our view that U.S. economic fundamentals remain solid (e.g., activity levels are at record highs and consumer and business confidence remain near cyclical highs) with only a modest risk of recession over the next 12 months, our base case is that the current cycle will resemble these time periods. This assumption supports our more optimistic view on equities as it historically has led to an ~8% rally in the one month leading up to the initial cut and more than a 15% rally in the 12 months after the initial cut. Sectors that outperform in these periods are Info Tech, Communication Services, and Consumer Discretionary.

- Failure: Too little, Too Late. The risk factor is that the economy is already on the path to recession and that any interest rate cuts will prove too late or that the negative repercussions from trade frictions will overpower the Fed’s stimulative potential. In those instances where a recession was unavoidable, the equity market has struggled with the S&P 500 falling, on average, 10% in the 12 months following the initial cut. Cyclical sectors such as Info Tech, Financials, and Consumer Discretionary have been the hardest hit during these time periods.