The eurozone economy has experienced a sharp slowdown since the second half of 2018 in a reversal from the mini-boom enjoyed in 2017. This downturn has been most pronounced in the manufacturing sector and in Germany, due to its heavy exposure to weakening foreign demand and temporary setbacks that stalled its auto sector. While uncertainty relating to global trade tensions, Brexit and other European political headwinds will likely continue to take their toll in the near term, we at Invesco Fixed Income believe the eurozone economy will recover, growing toward trend level in the second half of this year.

Although we do not predict an imminent surge in global demand, we believe a gradual recovery in foreign trade on the back of accommodative policies and loose financial conditions abroad should eventually benefit European industry. Adding to that, resilient private consumption, easy monetary policy in Europe and the resolution of Germany’s temporary production bottlenecks are likely to support the eurozone economy through the rest of the year.

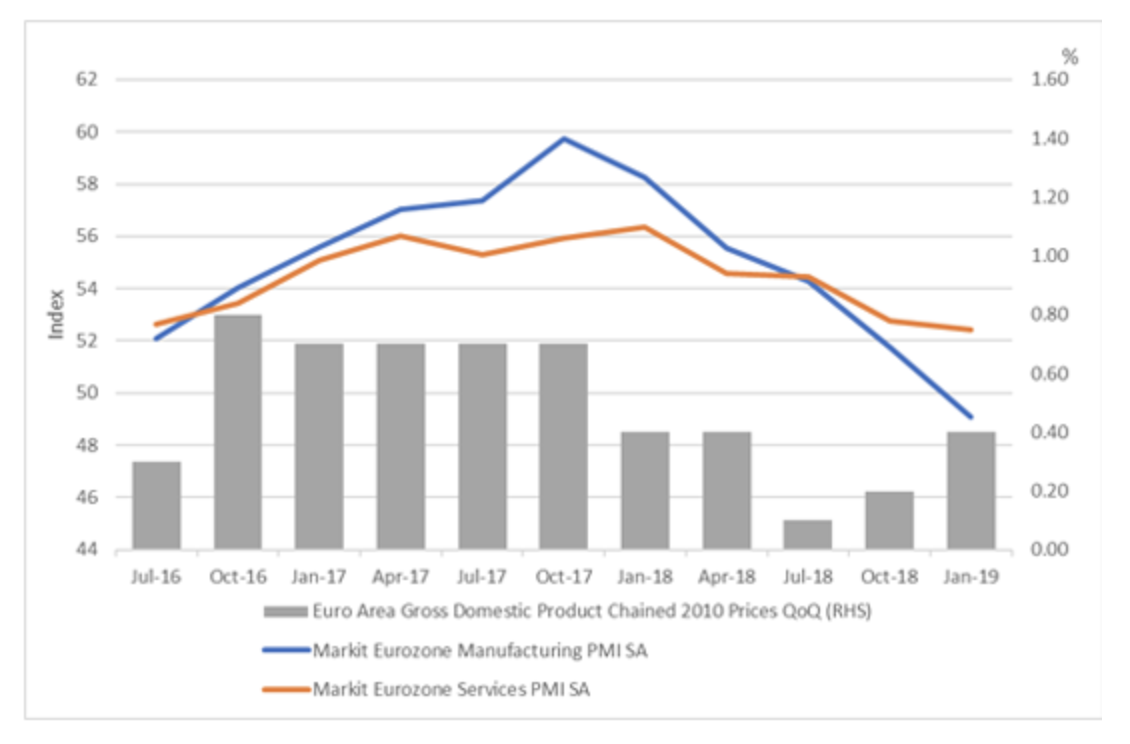

Figure 1: Eurozone real GDP growth and PMI surveys

Source: Eurostat, Markit, data from May 20, 2019. The Index label on the left axis refers to the Markit Eurozone indexes shown (SA stands for seasonally adjusted). GDP refers to gross domestic product. PMI refers to purchasing managers index. RHS means right hand series and QoQ means quarter on quarter — the change in value at the close of each three-month period.

Domestic demand continues to be supportive

Economic data have continued to show a stark contrast between a strong services sector and struggling industry. We expect employment and wage growth to support private consumption in the near term as labor scarcity seems to be translating into moderately higher wages. With continued low inflation, these developments should improve disposable income and support consumption growth.

Chinese green shoots not yet showing in European manufacturing data

With China’s improved growth momentum in the first quarter of this year, the question now is when will this improvement feed into eurozone manufacturing performance? Eurozone growth was higher than expected in the first quarter of 2019 (0.4% quarter-on-quarter, up from 0.2% at the end of 2018).1 However, continued weakness in second quarter European survey data has diminished hopes of a major turnaround in the European economy. Recent Chinese stimulus has been smaller relative to previous rounds and has focused more on infrastructure than credit policy — this could be leading to smaller (and slower) spillover to other economies. Nevertheless, we expect Chinese stimulus to provide some boost to the eurozone economy with a lag of three to six months.

Escalating trade tensions between the US and China could also weigh on the production decisions of European manufacturers, and the risk of increased US tariffs on European cars and parts (a decision now delayed to November 2019) could further dampen sentiment. On the other hand, the weaker trade-weighted euro and overall stronger global growth are bright spots for Europe’s manufacturing outlook. We believe a modest recovery still seems possible over the course of this year.

Drags on “bellwether” European industrials will likely dissipate, but trade and Brexit concerns remain

Based on management commentaries, it appears that issues with the European Union’s (EU) new testing standard for vehicle emissions, the Worldwide Harmonised Light Vehicle Test Procedure (WLTP), created a notable drag on sales and production in the first quarter of 2019. Most of these issues have now been resolved, and the next step of the WLTP process (due to go live in September 2019) should have far less impact on original equipment manufacturers (OEMs). A potential second half recovery among German OEMs is also supported by company-specific product cycles, including new product launches expected from major auto producers.

A re-escalation of trade concerns and turbulence surrounding Brexit are clear risks going forward, in our view. Companies probably expected clarity on these issues in the first half of 2019 and a resulting boost to demand in the second half. But these issues remain unresolved as reflected in recent data — April Chinese auto sales fell 17% year-over-year despite a significant value-added tax (VAT) cut. We may continue to see soft demand as industrial sentiment remains muted.2

Eurozone has limited room for policy response

The European Central Bank (ECB) acknowledged weaker eurozone growth momentum at its March meeting. It significantly downgraded its 2019 projections for growth and inflation and extended forward guidance on interest rates, suggesting key rates would remain unchanged through at least the end of 2019. It also announced a new series of targeted longer-term refinancing operations that will begin this September.

Compared to the US and China, the euro area has limited room to further loosen monetary policy in the face of a pronounced economic slowdown. So far, Germany does not view the manufacturing downturn as deep enough to warrant significant fiscal stimulus and remains seemingly dedicated to “black zero” (the requirement to maintain a balanced budget). Therefore, with Europe divided between countries that would like to implement more accommodative fiscal policy but have limited ability to do so, and those who are able to but less willing, the ECB may have to support a revival of the European economy on its own for now.

Trade wars, Italy and Brexit pose mounting risk to a eurozone recovery

Stronger eurozone growth in the first quarter of 2019 may suggest that concerns around the state of the economy were overdone, reinforcing our forecast for some stabilization of growth later in the year. But numerous headwinds pose mounting risks in the months ahead.

The escalation of the US-China trade conflict in May could cause ripple effects in the eurozone. While the timing and extent of additional US tariffs on EU goods remains uncertain, these could materially dent the macro outlook if they materialize. Continued uncertainty could also damage business confidence and capital expenditure growth, leading to weaker consumer confidence and private spending down the road.

In Italy, risks of a fresh clash with Brussels over Rome’s spending commitments have recently increased. The European Commission has warned that Italy’s policies could push its budget deficit to 3.5% of GDP in 2020 (above the 3% EU ceiling) without the planned VAT hike.3 However, Italy’s government seems confident that the European Parliament elections will shift the political landscape, giving it some breathing room. Italy’s League and Five Star Movement parties won more than 51% of the votes in the European Parliament election at the end of May.4

Brexit uncertainty has already weighed on eurozone growth and taken a toll on exports to the UK, with Germany again bearing most of the brunt. An extended period of uncertainty could continue to damage European industry sentiment and business investment, and the lingering risk of a disruptive “no-deal” scenario threatens to weaken Europe’s economic prospects.

Outlook

Despite these uncertainties, we believe eurozone growth can still recover, supported by a modest recovery in the manufacturing sector along with continued solid private consumption and accommodative monetary policy. We expect eurozone growth to show signs of improvement and revert towards trend in the second half of this year.

1 Source: Eurostat, May 15, 2019.

2 Source: China Automotive Information Net, May 15, 2019.

3 Source: European Commission, Spring Forecast, May 7, 2019.

4 Source: European Parliament, 2019 European election results, June 4, 2019.

Important information

Blog header image: Elisa Bonomini/Shutterstock.com

The Eurozone (also known as the euro area or euroland) is an economic and monetary union of 18 European Union member states that have adopted the euro (€) as their common currency.

Brexit refers to the scheduled exit of the UK from the European Union.

Gross domestic product is a broad indicator of a region’s economic activity, measuring the monetary value of all the finished goods and services produced in that region over a specified period of time.

The Markit Eurozone Manufacturing Purchasing Managers Index measures the performance of the manufacturing sector and is derived from a survey of 3,000 manufacturing firms representing an estimated 90% of Eurozone manufacturing activity.

The Eurozone Services Purchasing Managers Index is based on data collected from a representative panel of around 2,000 private service sector firms. National services data are included for Germany, France, Italy, Spain and the Republic of Ireland.

The value-added tax (VAT) is a type of consumption tax added to the price of goods and services.

Macroeconomic (or macro) factors are those related to the economy at a regional or national level. Examples of these factors include unemployment, inflation, fiscal policy and commodity prices.

Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Many countries in the European Union are susceptible to high economic risks associated with high levels of debt, notably due to investments in sovereign debts of European countries such as Greece, Italy and Spain.

Read more commentaries by Invesco