Weighing the Week Ahead: Who Really Runs the Fed?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is modest with a focus on monetary policy. Minutes from the last FOMC meeting, Congressional testimony by Fed Chair Powell, more inflation data, and continuing discussion of Friday’s employment report all put the Fed in focus. In addition, President Trump has identified interest rates and Fed policy the “most important problem” facing the nation. Pundits and financial media will follow that lead, raising the question:

Who is really running the Fed?

Last Week Recap

In last week’s installment of WTWA, I predicted that the improvement in the US/China trade debate would spark an initial rally, only to be met by objections. As the rally faded on Monday, you could check off each of the viewpoints I said we would hear. As the week progressed, the emphasis on spinning held true. The employment report looked like pretty good news to almost everyone, but the initial market reaction was negative.

Mike Williams colorfully captured the early action.

Mike’s take?

Now, what’s especially disturbing about this is pretty basic:

Last month, when the jobs report was a “paltry” reading, another batch of experts espoused that most assuredly the Fed needed to be quick to adjust their thinking…and of course, they paraded out all the past times when Fed upticks led to terrible recessions – for the last 473 years.

In other words – low jobs growth is bad – and high jobs growth is bad.

The inimitable Eddy Elfenbein nailed the action with this quip:

The good news is bad news because the previous bad news was seen as an impetus for good news but now that bad news is no longer tenable which is good news and that’s, as I said before, bad news.

All things considered, it was one of my better weeks for both the market action and the commentary.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Investing.com’s chart of S&P futures. This allows us to see the reaction to news when the market was closed. The “N” notations represent news events, which you can identify if you check out the interactive version at the site.

The market posted a quiet, 1.7% gain for the week. The trading range was only 1.5%, smaller than the gain because I do not include the prior week’s close in the range calculation – only prices occurring during the week. My weekly Quant Corner translates this into a volatility calculation which you can compare both to VIX and to past readings.

Personal Note

I am delighted to report that my company, NewArc Investments, Inc. has been acquired by Incline Investment Advisors, LLC. Their talented and experienced team has incorporated the NewArc crew in an expanded firm. This combination, which we have already tested on some joint projects, is showing an exciting synergy. I expect an excellent result both for my clients and also my loyal team.

For me (and of course for Mrs. OldProf) this is my version of “retirement.” I get to focus on the markets, managing portfolios, and writing – all of the things I love. I am relieved of most day-to-day management tasks and paperwork. My estimate is that I can cut my work week in half, to thirty or thirty-five hours. We are seeking a more temperate climate, lower taxes, and a nice view from my new home office.

For readers, I hope you will join in the benefits. Many of the items on my writing agenda will now get some overdue attention.

Noteworthy

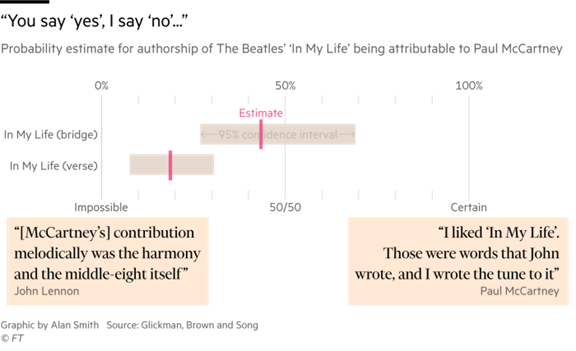

Forget about trading algorithms! Researchers have developed one that helps in solving musical mysteries. Was it John or Sir Paul who was more responsible for some of the great hits without clear authorship? (The FT). One example:

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. There are three different groups. Long-term indicators and the nowcast remain positive. The short-term message is now slightly negative. NDD repeats that the Fed and the trade wars “remain crucial.”

The Good

- ISM manufacturing registered 51.7, slightly beating expectations of 51.5, but slightly missing the May reading of 52.1.

- Christine Lagarde’s selection as the President of the European Central Bank, succeeding Mario Draghi, got a favorable reaction from observers. She is expected to provide continuity for existing policies. (The Economist).

- Payroll employment showed a net gain of 224K, much better than May’s 72K and beating expectations of 160K. Private payrolls showed similar strength. I did a preview before the report, emphasizing the need for caution in the interpretation. Here are charts from some favorite sources emphasizing the key themes.

While labor force participation remained solid.

And Bob Dieli’s insightful take.

Alas, there were some very, very poor analyses from some of my “reliably bearish” Twitter commentators. I am considering doing a piece each week – perhaps using a chart video – to explain some of the common errors.

The Bad

-

Construction spending declined by -0.8%, lower than the consensus for no change and April’s (upwardly revised) gain of 0.4%.

-

ADP private employment showed a gain of 102K for June. This was an improvement of May’s 41K gain, but missed the consensus forecast of 145K.

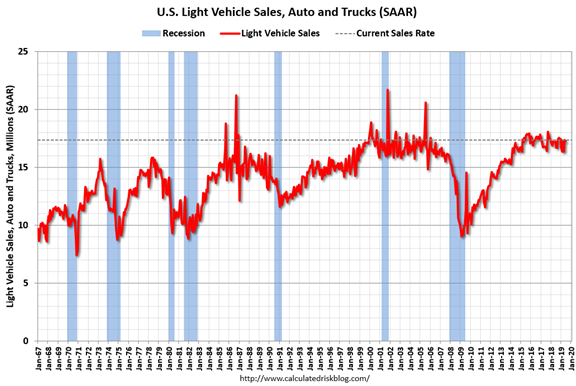

- Light vehicle sales decreased 0.6% from the May sales rate at a pace of 17.29 million (SAAR). This is a slight YoY improvement. Calculated Risk has the story and this chart, showing a “sideways move at near record levels.” Put another way, the economic boost from increasing auto sales seems to have ended.

-

Heavy truck orders are down 69% from last June, partly from slowing freight demands and partly from a tough comparison.

-

Factory orders for May declined -0.7%, better than April’s downwardly revised -1.2%, but slightly worse than expectations of a -0.5% decline. Steven Hansen (GEI) reviews the report showing the data from several different viewpoints. None look very good.

-

ISM non-manufacturing was 55.1, lower than May’s 56.9 and expectations of 55.8. (FT Portfolios).

-

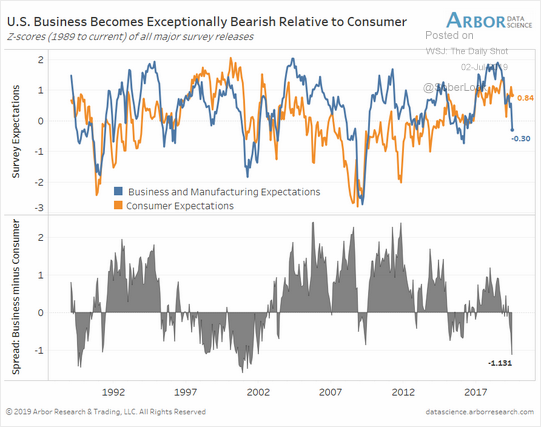

US business is getting more bearish than consumers (Daily Shot).

The Ugly

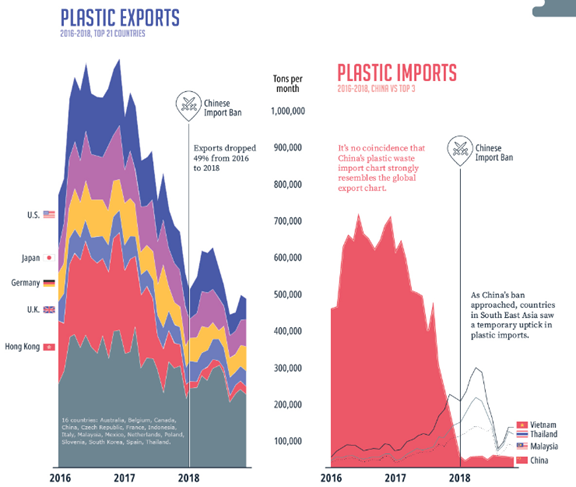

Plastic Waste. Visual Capitalist has its customary great representation of the flow of the world’s plastic waste. I cannot do justice to the post in a small segment, but here is a taste.

See also Cleansing Plastic From Oceans: Big Ask for a Country That Loves Wrap.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

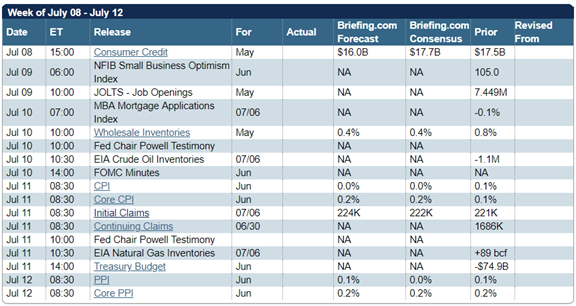

The economic calendar is normal with an emphasis on the Fed and inflation data. Chairman Powell delivers his semi-annual Humphrey-Hawkins testimony on Wednesday and Thursday. We will see little that is new in the prepared remarks, but the questions often raise new points. The FOMC minutes from the last meeting will get careful attention. PPI and CPI inflation measures have been tame, but any hint of a pop in prices will attract attention. The NFIB index has risen in importance as a measure of enthusiasm for the Trump administration and prospects for business investment and employment. Finally, the JOLTs report may provide insight into possible tightening in the labor market.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Market participants will return from a holiday just in time for (even more) spirited discussion about the Fed. The quiet Friday trading signaled that many were missing despite the important employment data. With that to digest, the release of the June FOMC minutes, two days of Congressional testimony by Chairman Powell, new appointees to consider, and fresh inflation data we can expect a week that is all about the Fed.

Recent developments bring a new slant on this familiar topic. Pundits will lead the discussion, asking:

Who really runs the Fed?

Background

The formal structure of the Federal Reserve Board is easily explained (good description here), but often misunderstood. The governing body is the Board of Governors consisting of seven members who are nominated by the President and confirmed by the Senate for staggered 14-year terms, two expiring each year. The Chair and Vice Chair serve four-year terms but may be reappointed. They must be members of the Board of Governors. Congress oversees the Federal Reserve Board.

Financial markets focus on interest rate decisions made by the Federal Open Market Committee (FOMC). This consists of all seven Governors from the Board, the President of the Federal Reserve Bank of New York, and four of the remaining eleven Reserve Bank presidents on a rotating one-year basis. All of the Bank Presidents attend FOMC meetings and join in the discussions, but only those currently on the FOMC have a vote on policy.

The description of the formal structure does little to explain the dynamics behind current policy decisions. Much depends on who asserts authority and how the Fed members respond.

Candidates for Power

Many actors are cited as sources of great influence over the Fed.

- The Chairman. Nearly everyone acts as though decisions are made by the Fed Chair. There is a consensus process led by the Chair, but there is sometimes dissent and occasionally an uprising. We also never really know when the Chair is discovering and following a consensus of the members or leading in a new direction.

- Financial markets. Many believe that the Fed is following the direction of financial markets, confirming the interest rates that have already been determined. Satisfying financial markets is not part of the Fed dual mandate (maximum employment and stable prices within the context of moderate long-term rates). The Fed certainly watches markets, but members react to the information quite differently.

- Congress. Congress has the power to amend the Federal Reserve Act of 1913 and occasionally does so. There have been recent moves to reduce the power of the Fed. Chairman Powell’s testimony this week is and example of a Congressionally mandated oversight process.

- The President. Beyond appointing Governors and the leadership, the President has little formal power. Traditionally Presidents have stayed an arm’s length from the Fed with the goal of preserving Fed independence. President Trump has broken from this approach, frequently commenting on policy. Yesterday he described the Fed as the “most difficult problem” the U.S. faces. (The Hill).

Policy Outcomes

The outcomes we should expect depend upon who is in charge. If the Chairman, we should listen carefully to all public statements. If financial markets, we already know what to expect. If Congress, pending legislation and the tenor of questions at hearings provides needed information.

If the President has power, the dynamic is a bit trickier. Might the Fed balk at Presidential demands, attempting to show independence? Does the President lead market viewpoints, introducing another path for causation? Can the President “stack the Board” with those who share his viewpoint about interest rates? Will Congress approve such candidates? The President has already appointed the Chairman, the Vice-Chairman, and one other member. He is currently appointing candidates for two vacant seats.

As you can see, it is not so easy to figure out who is in charge or what policy results to expect.

I’ll cover my own ideas about the implications in today’s Final Thought.

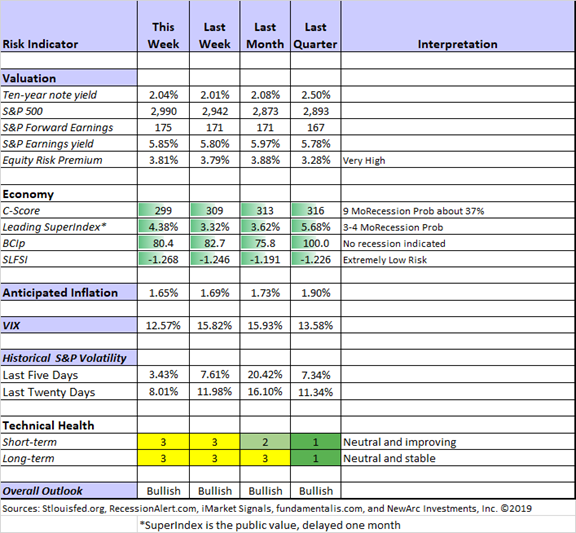

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Both short and long-term technical health have stabilized at neutral.

The C-Score declined along with the flattening yield curve. It still signals the need for watchfulness concerning confirmation from other indicators.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

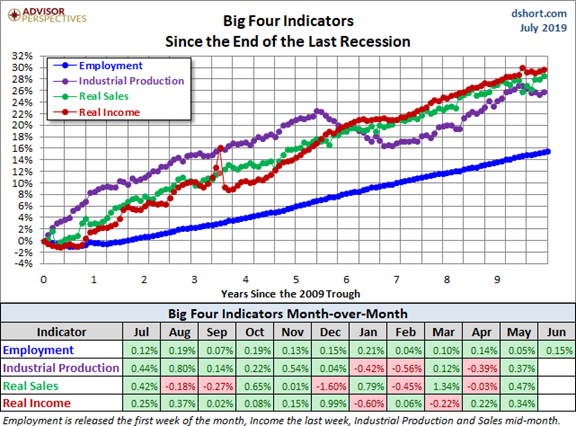

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis, especially the regular updates of the Big Four indicators used by the NBER recession dating committee.

Insight for Traders

Our weekly “Stock Exchange” series took up the incessant fear-mongering, the wall of worry, and new all-time highs. What does this mean for traders? Many seem to be fighting the trend. We also reviewed recent picks from the trading models, showing the frequent contrast with a fundamental analysis. Pulling it all together was our series editor, Blue Harbinger.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Daniel Grioli’s i3 Insights: The Curse of Information. He begins with one of my favorite educational techniques – leading off with an example where the reader will not be locked into a bias. He discusses the excessive cost of “defensive medicine” as well as the risks to the patient.

Unfortunately, risk means different things to the doctor (getting sued or banned from medicine), the healthcare system (overpaying and overcrowding) and the patient (getting sick or dying). Doctors are very well aware that their treatment decisions will be assessed with the benefit of hindsight; jokingly called the retrospectoscope.

He then describes several applications to investing, contrasting expert behavior with those doing an evaluation. The interesting argument is difficult to summarize with a few quotes, but this one about dealing with risk is a good example.

An example of this is a fund manager reducing investment risk. The manager, who we assume has expert knowledge, sees that the risk/return equation is now unfavourable. Consequently, they reduce risk, perhaps allocating part of the portfolio to cash or using derivatives to hedge.

The fund manager imagines that the client would be pleased by their prudence. Instead, the client is really only worried about their returns diverging from peers or the benchmark-relative under-performance created by the fund manager’s actions. This difference in knowledge is then exacerbated by the hindsight bias if the fund manager’s caution proves to be unwarranted.

These are just the first concepts; there is plenty more. And it is not just about fund managers. The thoughtful individual investor will find much to think about.

Stock Ideas

Lyn Alden Schwartzer analyzes the bank stress test results – assumptions, worst cases, and how various banks fared. This is a very nice analysis, highlighting the various types of risk and the profile of the banks. She concludes with a hidden gem – a regional bank. Here is a key quote:

Basically, well-run credit card issuers are cases where the volatility is far worse than the risk of permanent capital loss, which can present buying opportunities in dark times. Opportunistic investors should pay attention to this space when times get tough and see how the fundamentals are doing compared to the stock price.

Need yield? Colorado Wealth Management takes a close look at the preferred shares from Annaly Capital Management. They like the yield in some newly-issued shares, but investors must be careful. One issue was called and the symbol has changed. Read the full post for details.

A (very) few ideas in the consumer defensive sector. (Morningstar).

Housing stocks? The much-hated sector has appeal for me. I explain my reasons in this post (part two of a series).

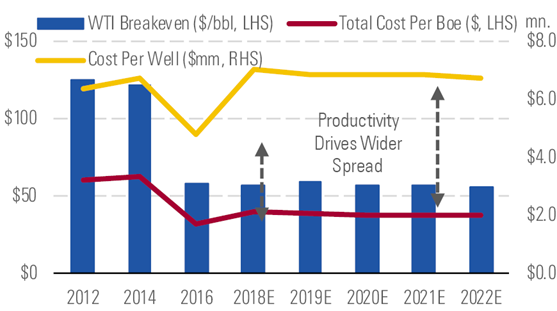

Oil service stock ideas from Morningstar. A key assumption: $55 per barrel as the long-term balancing point for supply and demand.

Personal Finance

Abnormal Returns always provides interesting ideas on a wide variety of topics. I am a subscriber, and I read it daily. Each Wednesday’s edition includes a post focused on personal finance. There are always several interesting and informative choices. My own favorite this week was Michael Batnick’s highlights from the recent Zillow report on home transactions. Of the many facts that might surprise you, here are some to consider:

Buyers

- Millennials, those between the ages of 24 and 38, comprise 42 percent of the nation’s home buyers

- Just over half (52 percent) of buyers put down less than 20 percent on their home.

Millennials are also the largest group of sellers (31%).

Homeowners

- Home equity remains the biggest financial asset for the typical American homeowner, who has 52 percent of their wealth tied up there.

- Nearly half (45 percent) of homeowners still live in the first home they purchased

I also enjoyed Adam. M. Grossman’s advice on how to check out charities before contributing.

Watch out for…

Kodak (KODK). D.M Martins Research warns that you might lose everything if the company goes under again. In Fight To Survive Mode, Kodak Is A Zombie Stock

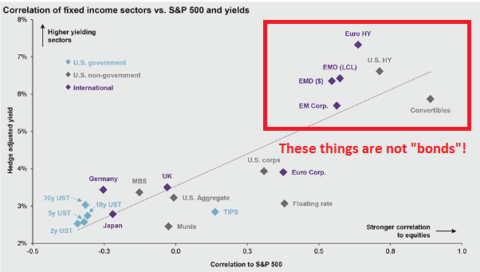

Bonds that behave more like stocks. Cullen Roche explains.

Final Thought

Who’s in charge here? The many different answers depend upon the circumstances.

There are a few instances where Fed action was needed to support financial markets with a burst of liquidity. There is little evidence of an ongoing mission to support asset prices. I have frequently challenged those making such an assertion to find evidence in the transcripts of past meetings. (These are delayed by five years but are comprehensive accounts of the meeting. They are edited only for minor corrections). No one has accepted that challenge.

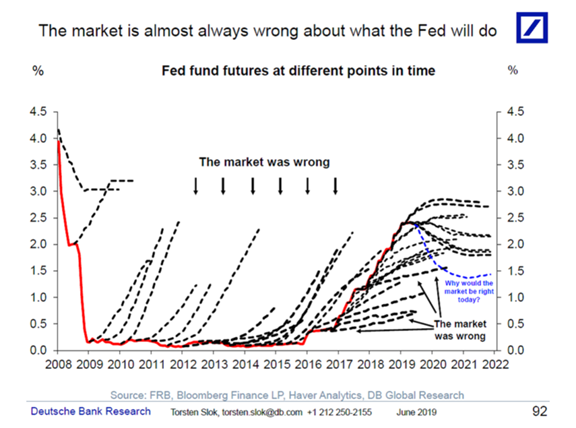

The evidence also shows that markets are poor at forecasting Fed policy. This does not change the mind of anyone steeped in trader lore.

Congress has ultimate power, but usually exercises it judiciously. Powell’s testimony will be interesting to the Fed wonks among us, mostly to learn if he will hint about anything relevant. (Think that can’t happen? You have forgotten about the early years of Ben Bernanke and his comments to Maria Bartiromo over a cocktail).

The internal Fed dynamics often occur quietly in discussions before official meetings. My own approach is to view the Chair as an important leader, but one who is constrained by the viewpoints of colleagues as well as information from the expert economic staff. In the age of Fed transparency we certainly know more about the thinking of individual Fed participants (a term used to include the non-voting Regional Bank Presidents). The Bank Presidents are less likely to be PhD economists and there have been significant policy divisions in recent years.

Most important is the President. One of Trump’s most effective uses of power is defining the national agenda, often with a tweet or offhand comment. My personal viewpoint is that a non-political central bank is essential. Undue control by Congress or the President would simply lead to excessively low interest rates, which politicians generally love.

Turning to current market outlook, people continue to believe that there is an expiration date on a business cycle. The key point is recognizing that we had a deep recession and a slow rebound.

Widespread investor fear has led to a crowded trade in bonds and bond substitutes, and an over-emphasis on FAANG stocks.

This has persisted long enough that some are concluding that value investing is dead. Davidson (via Todd Sullivan) offers a nice contrast, suggesting that many do not accurately define value. Personally, I see many stocks that are inexpensive, have solid earnings growth, and are reasonably priced. I mentioned two of them in my housing article, but there are many more.

And value traps? They are great yield platforms if you repeatedly write near-term calls. But that is a story for another day.

Investors and the Fed?

Near the close of Friday’s trading CNBC interviewed a “Senior Contributor” with a lot of what they call “street cred.” He explained that the market was repricing based upon the expectation of a 25 bps rate cut in July instead of 50 bps. The DJIA was down 18 at the time. This was also the theme on the closing news.

If financial “experts” are satisfied with explanations like this, the individual investor has little to learn from them.

The exact pace of Fed policy makes little long-term difference. Patience is just fine. Negative market reactions remain opportunities to buy.

And also, some longer-term items on my radar

I’m more worried about:

- Business investment. While many have not taken note of the trade war effects, it is a reason for caution by business.

- Government debt. The tax cut effects need to kick in if this is to be reduced.

I’m less worried about

- Market prospects. New highs are bullish, especially when supported by earnings. The bar is set low for the upcoming earnings season.

- The yield curve. I’m watching, but no other confirming recession signals so far.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits