Key Takeaways

- Macro trade and monetary policy optimism have lifted the U.S. equity market to record levels

- Second quarter earnings growth likely to be lifted from negative to positive territory

- With elevated equity valuations, positive forward guidance needed to maintain momentum

For the next several weeks, we will go from talking about the proverbial forest (macro headlines) to focusing on the trees (corporate earnings). The forest has grown to record levels (S&P 500 crossing the 3,000 level for the first time and notching its ninth record close of the year) on the back of policy “fertilization.” The thaw in trade tensions between the U.S. and China following the Trump/Xi G-20 meeting and a growing synchronized global central bank dovish tone (highlighted by Fed Chair Powell in his testimony this week) have increased optimism that the U.S. (and global) economic expansion will gain momentum. In fact, the S&P 500 P/E (LTM) has soared to ~18x to reflect a market priced close to perfection. However, outside of the strong June U.S. employment data, other U.S. economic data (manufacturing, housing) and global data (Europe PMIs in contraction) suggest “clouds” of weakness forming. As earnings are the fundamental driver of the equity market, 2Q earnings season will give us a picture of how healthy the “trees” are as many of the big banks kick-off the reporting season next week. Below are some of the key dynamics to monitor throughout the upcoming earnings season:

-

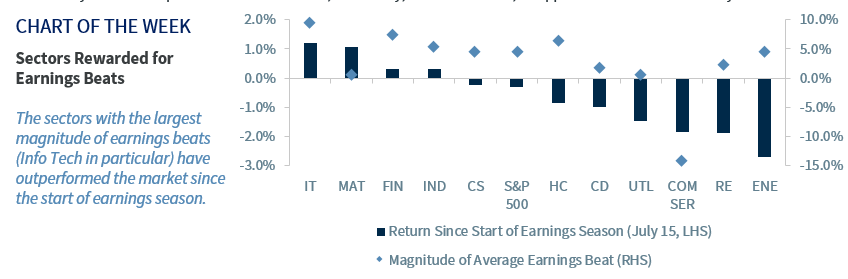

- Avoiding Negative Earnings Growth | After being revised down 2.4% since the start of the second quarter and the largest number of negative earnings pre-announcements since 2016, consensus earnings forecasts currently reflect an earnings decline of 1.4% on a year-over-year (YoY) basis. Based on history, our expectation is that companies will beat their lowered earnings forecasts (which they have done for five consecutive quarters) by ~3% to 5% and lift earnings growth back into positive territory. Early indications suggest we will be correct because of the 24 S&P 500 companies that have reported, 84% of companies have beaten earnings estimates by an average of 8.8%. The bigger question is whether the second quarter in a row of sub-2% earnings growth (with the prospects of a third consecutive quarter next quarter—3Q earnings growth estimate is currently +0.1%) can serve as a catalyst to take equity prices higher from current levels. Similar to earnings, revenue growth is also expected to be fairly muted as top-line sales growth is expected to rise 5.3%, which would be the lowest pace since 3Q16 if this forecast holds.