“You pay a high price for a cheery consensus.”

—Warren Buffett

The stock market has a history of torturing highly-valued knowledge. About every seven years a consensus forms around the fastest growing sector of the stock market, or the fastest growing country, or the fastest growing industry. Do you remember how excited everyone was about investing in China and other Asia-growth economies seven or eight years ago? Where did those 500 million new middle-class citizens go which many of us “knew” were going to make companies rich? History shows that themes of popularity are an invitation for poor forward returns.

Simultaneously to the over-pricing of well-known facts, is the underpricing of the futures of meritorious companies which are suffering temporary forms of tribulation. History shows that the stock picker can add alpha by wading into fear when certain qualitative characteristics exist. The underpricing of good quality shares with positive futures is a regular phenomenon in the stock market but has reached a crescendo recently.

We will hypothesize on knowledge we believe is well known/over-priced and on what isn’t well known or well believed and could be underpriced.

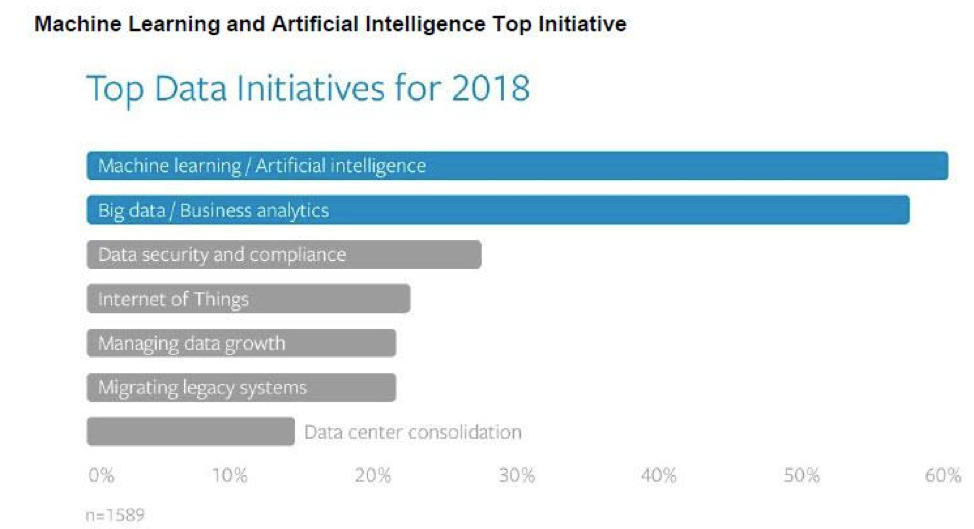

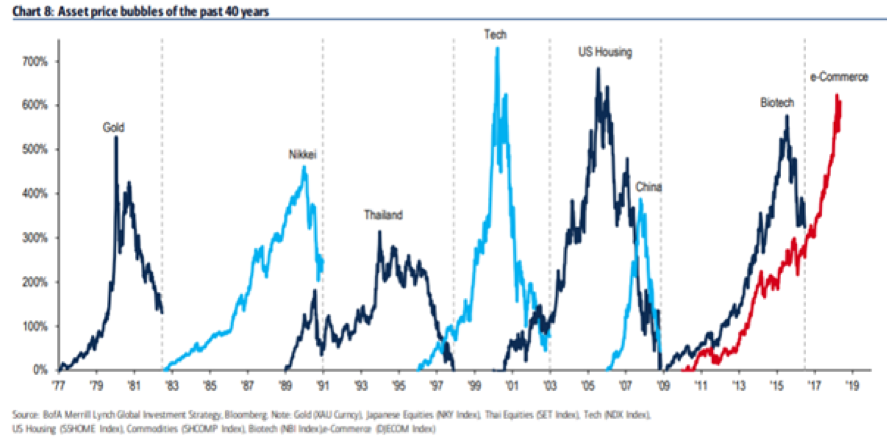

Everyone thinks they know that artificial intelligence (AI) and big data are the future

We go to industry conferences and AI/data analytics seems to be all anybody talks or thinks about. In 1999, it was “the internet will change our life.” They were correct about the internet and investors got slaughtered investing in internet darlings. Will artificial intelligence and data analytics be any different?

The chart below shows the biggest parabolic moves in price in the past 45 years. We believe investors have expressed their excitement about AI and data analytics first through the most successful e-Commerce companies.

Source: DoubleLine Funds, BofA Merrill Lynch Global Investment Strategy, Bloomberg.

Everyone thinks they know that interest rates will remain low

Everyone thinks they know that inflation is dead and that interest rates are permanently going to stay near historic lows. However, long-time bond market watcher and veteran financial writer and historian, James Grant, thinks otherwise!

Interest rates tend to change course only once or twice a generation. In 1981, investors could look back on 35 years of generally rising rates. In 2016, a different generation of investors could look back on 35 years of generally falling rates. In bonds, you can profitably spend a whole career not changing your mind.

Humans eat, sleep, and extrapolate. What we think we can foresee is often nothing more than what we have recently seen. “More of the same” is the sensible default prediction in politics, baseball, and interest rates alike. In rates, it actually tends to work.1

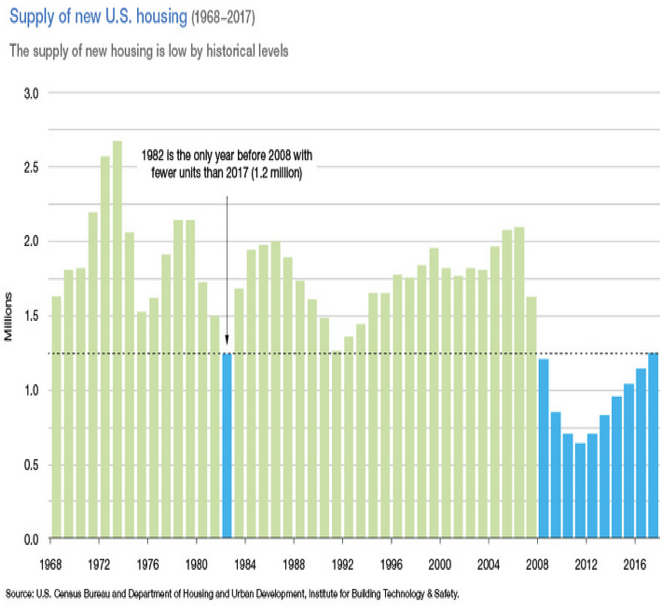

The Federal Reserve Board flooded the U.S. economy with liquidity in the aftermath of the financial crisis to help us recover. They have succeeded in getting past the crisis, but they have not withdrawn the liquidity. If 89 million millennials get married in large numbers, have kids and buy houses like polls show they will, there could be an inflation surge like we haven’t seen for years! If interest rates normalize in the next ten years, capital markets will get re-priced and risk premiums could adjust extensively.

Source: Freddie Mac, The Major Challenge of Inadequate US Housing Supply (http://www.freddiemac.com/research/insight/20181205_major_challenge_to_u.s._housing_supply.html), December 5, 2018.

As the chart above shows, the U.S. might be the most underbuilt on single family residences as any time since 1960.

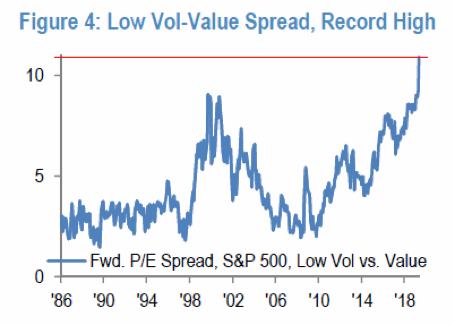

Everyone thinks they know all you need to do is invest in the consistent growers

Source: JPMorgan, The Value Conundrum, 06 June 2019.

Mature and slower-growing growth stocks are opening investors up to large risks. Paying 30-times profits for established growth companies like Nike, Costco, Visa, Mastercard, Starbucks and others could be a ticket to misery when the price of money rises and price multiples contract when risk premiums return to the levels of the past. If and when price multiples return to their historical norms (15 to 20 times earnings), heartache and incrimination could ensue.

Everyone thinks they know millennials will attempt to keep their adolescence

While the deep recession and more years devoted to four-year college degrees have pushed maturity back five-plus years in the U.S., our research shows that 25-year old women want very similar things to women in prior generations. Their favorite cable channel is HGTV and one of their favorite shows is TLC’s “90-day Fiancé’.”

Most of them ultimately want a husband and a home they can call their own. These are college-educated women and the best educated group of people we’ve ever had. Even Warren Buffett, who owns the second largest real estate brokerage company, mentioned at the Berkshire Hathaway annual meeting that he has become bewildered by the slow pace of home buying and residential construction. We advise Mr. Buffett to strap himself in for a good ten-year ride.

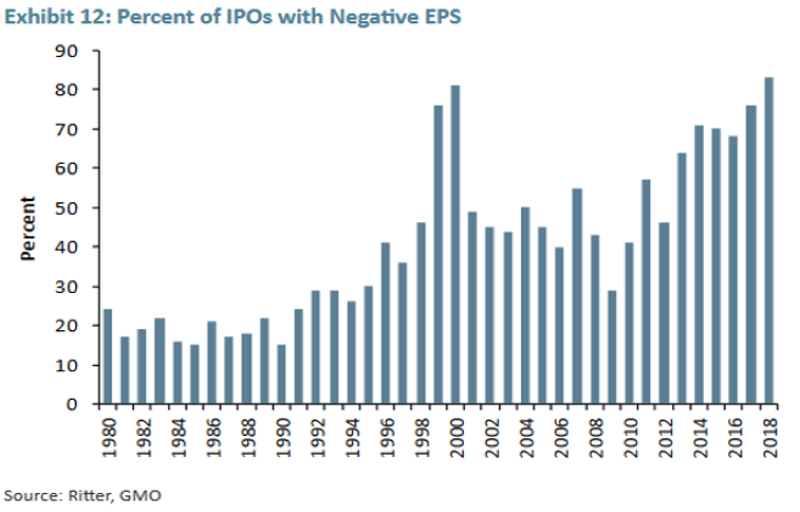

Everybody doesn’t know we are in the “crazy stage” in growth stocks

Source: The Wall Street Journal (https://www.wsj.com/articles/red-ink-floods-ipo-market-1538388000)

Source: GMO White Paper “The Late Cycle Lament” Dec 2018.

A rash of explosive initial public offerings of common stock has punctuated every historical growth stock binge. Fortunately, we don’t have to wonder if we have entered this crazy stage. Every week Wall Street brings a new series of exciting growth stocks public and many of them are tied to the most exciting and well-known themes (AI, data analytics, healthy eating, delivery via technology, etc.). Historically, you can anticipate the bloodshed within a few years when the over-supply of new growth stocks overwhelms existing supply and crushes prices for growth stocks.

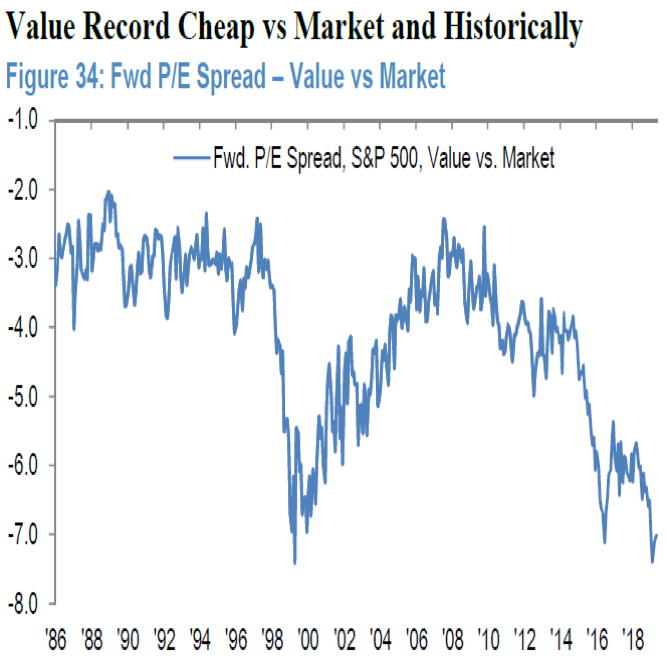

Everybody thinks they know that value investing is dead

Source: JP Morgan “The Value Conundrum” June 6, 2019

In a low turnover discipline like ours it is hard to do, but we must tack away from some winners of the past decade and gravitate toward companies which meet our eight criteria for common stock selection and are deep in the investor dog house. We are finding bargains in energy, 5G cellular technology, real estate, banks and old media. This forces us to make some hard choices which are made easier by the fact that we have created a great deal of wealth in our portfolios in the last three, five and ten years. We believe these adjustments will justify some capital gains taxes when value investing makes its historically-normal comeback.

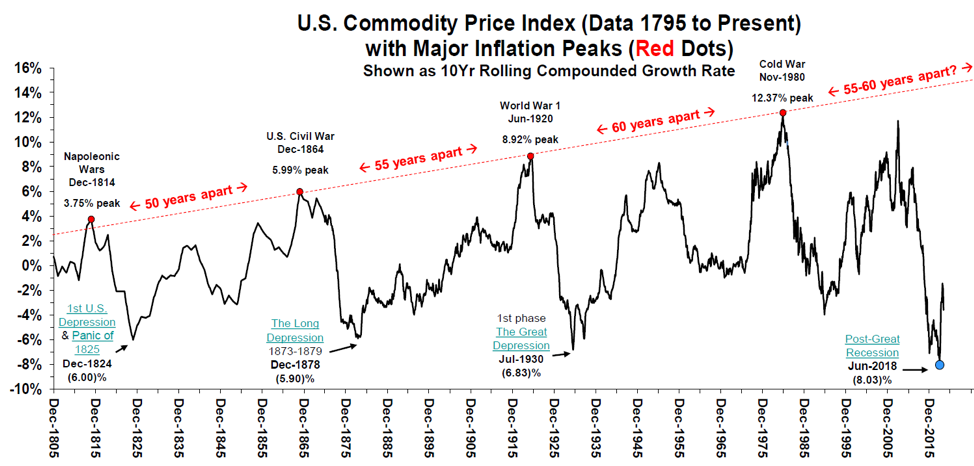

Everyone thinks commodity prices will stay lower for longer

Source: Bloomberg (https://www.bloomberg.com/opinion/articles/2019-05-30/oil-stock-share-of-s-p-500-at-30-year-low-for-good-reason).

Rarely does the index get this under-invested in the energy business. As the chart below shows, it could pay going forward to bet on a rebound in commodity prices and inflation.

Source: Stifel, Macro & Portfolio Strategy, dated June 6, 2019. Data for the time period 1/1/1805 – 12/31/2018.

Occidental Petroleum (OXY) is new to our portfolio and deserves an explanation. They are buying Anadarko Petroleum to create one of the world’s largest oil companies. Berkshire Hathaway (BRK.B) has pledged to invest $10 billion into preferred shares attached to eight million warrants to buy OXY at $62.50. Officers and directors have been backing up the truck to buy shares of Occidental. The stock is very depressed, the industry is undervalued, and we get a juicy dividend to wait for the companies to combine, sell unneeded assets and hopefully gush free cash flow over the next ten years.

In conclusion, we are very comfortable stacking long-term probabilities in our favor by being very contrary to today’s popular and unpopular knowledge. We are getting very favorable prices on the unknown futures of our value stocks and are avoiding getting caught in over-priced and well-known trends with loads of momentum attached. We think we have a handle on the price of knowledge. We thank you for trusting us with your capital and believe you will get well rewarded over the next five to ten years.

1Source: Barron’s (https://www.barrons.com/articles/jim-grant-low-interest-rates-forever-dont-count-on-it-51559904301).

Smead Capital Management, Inc.(“SCM”) is an SEC registered investment adviser with its principal place of business in the State of Washington. SCM and its representatives are in compliance with the current registration and notice filing requirements imposed upon registered investment advisers by those states in which SCM maintains clients. SCM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Registered investment adviser does not imply a certain level of skill or training.

This newsletter contains general information that is not suitable for everyone. Any information contained in this newsletter represents SCM’s opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves gains and losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. SCM cannot assess, verify or guarantee the suitability of any particular investment to any particular situation and the reader of this newsletter bears complete responsibility for its own investment research and should seek the advice of a qualified investment professional that provides individualized advice prior to making any investment decisions. All opinions expressed and information and data provided therein are subject to change without notice. SCM, its officers, directors, employees and/or affiliates, may have positions in, and may, from time-to-time make purchases or sales of the securities discussed or mentioned in the publications.

For additional information about SCM, including fees and services, send for our disclosure statement as set forth on Form ADV from SCM using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

© 2019 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap