In my role as the head of Research for SPDR® Americas, I am often asked to debunk myths about ETFs and their influence on the market. Fixed income ETFs had a record month of inflows this June, and an old myth has resurfaced that index-based investment strategies—both mutual funds and ETFs—had an outsized impact on the fixed income market, distorting bond prices and producing a passive bubble.

Let me be clear: this myth is simply not true. But saying that and debunking it are two different things. So in this blog, I am taking a deep data dive, using facts and figures to explain why global fixed income funds—and ETFs in particular—are not distorting the bond market.

Putting the size of the global fixed income ETF market in perspective

Flows into global fixed income ETFs have increased every year over the past five years, totaling a cumulative $597 billion throughout that period.1 But fund flows are not just an ETF story. Index-based strategies, both global mutual funds and ETFs, account for $1.7 trillion in assets under management (AUM), up from $247 billion in 2007.2 Meanwhile, the actively managed global mutual fund and ETF marketplace has jumped from $3.6 trillion in 2007 to $6.9 trillion.3 Global ETFs now represent 33% of the total $1.7 trillion of index-based fixed income market.4

These numbers, while significant, pale in comparison to the overall size of the entire fixed income market. Even with sizeable inflows over the past few years, index-based assets equate to only 2% to 3% of the overall global bond market.

Good index-based data in, good index-based data out

How did I arrive at the 2-3% figure above? Well, there are two ways to measure the global bond market.

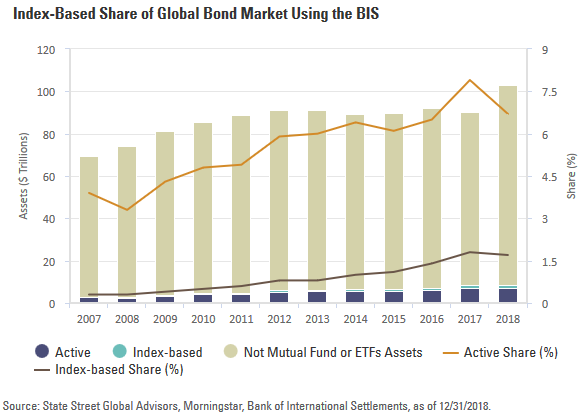

First, you can use the Bank of International Settlements (“BIS”) data, which captures all debt securities issued by residents in all markets. BIS figures, displayed in the below chart, show the index-based share of the global bond market is just below 2%.5

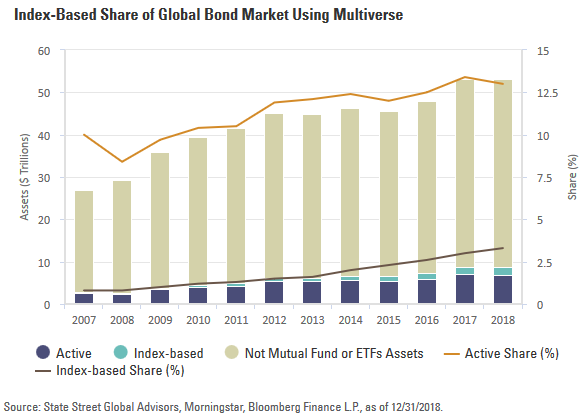

A second way to assess the size of the index-based market is to use a measure of investable debt securities as identified by the total market value in the Bloomberg Barclays Multiverse Index (“Multiverse”). This index is a broad measure of global fixed income markets including investment grade and high yield bonds. Multiverse data, shown below, calculates the index-based share of the global bond market at just barely above 3%.6

I would be hard-pressed to think an asset class that accounts for just 2% or 3% of any market can be responsible for a systemic impact that influences bond prices, or creates distortion and dislocation. A bubble is hardly forming from global index-based strategies, much less ETFs. If we hone in on ETFs alone and strip mutual funds out of the 2% to 3% market share data, ETFs would account for just 0.7% to 1.1% of the market.

Debunking the trading volume myth

Skeptics point to trading volume as more data indicating ETFs’ outsized impact on bond prices, but this argument doesn’t hold water either. To understand why, let’s use the high yield market. The median high yield ETF primary market notional activity over the last five years was $307 million. That represents just 2.9% of all cash bond trading volume, which has a five-year median of $11.2 billion.7 Again, I can hardly believe such a small figure would have such an outsized market impact.

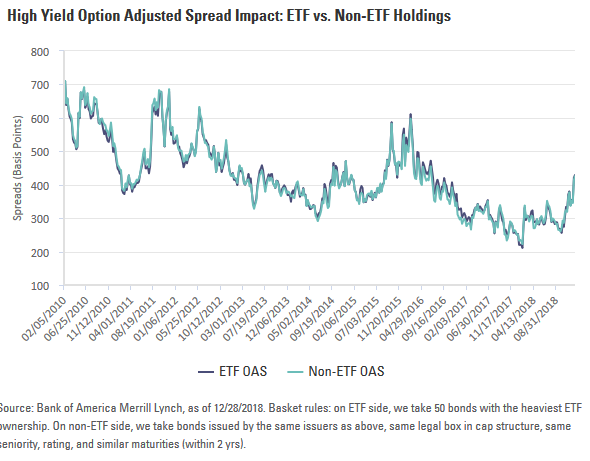

Fixed income ETF trading volumes and the ETF wrapper do not influence bond prices; it is the issuing company’s fundamentals and the prevailing market risk that do. Let’s look at the chart below. It depicts the differences in credit risk as measured by the option adjusted spread (OAS) on the top 50 most owned bonds by an ETF vs. the OAS on the bonds from the same issuer that are not included in an ETF. As shown, there is no discernable difference in the behavior of the bonds from an issuer—whether they are included in an ETF or not.

Index-based share of corporate bonds is less than you think

Another piece of ambiguous data clouding the debate around the influence of index-based strategies is the share of assets held in corporate and foreign bonds by mutual funds and ETFs. Unfortunately, I believe some of this confusion stems from a popular measure for determining corporate bond ownership—The Federal Reserve's Financial Accounts of the United States.

This Fed report includes data on fund flows and the levels of financial assets and liabilities by sector and instrument. Every quarter, the Fed states the amount of corporate bonds held by money market funds, mutual funds, closed-end funds and ETFs. The Fed's most recent report finds that $2.5 trillion worth of corporate bonds are held by these funds and ETFs, meaning that both active and index-based strategies represent a 21% share of the total value of the $12.1 trillion corporate bond market.8

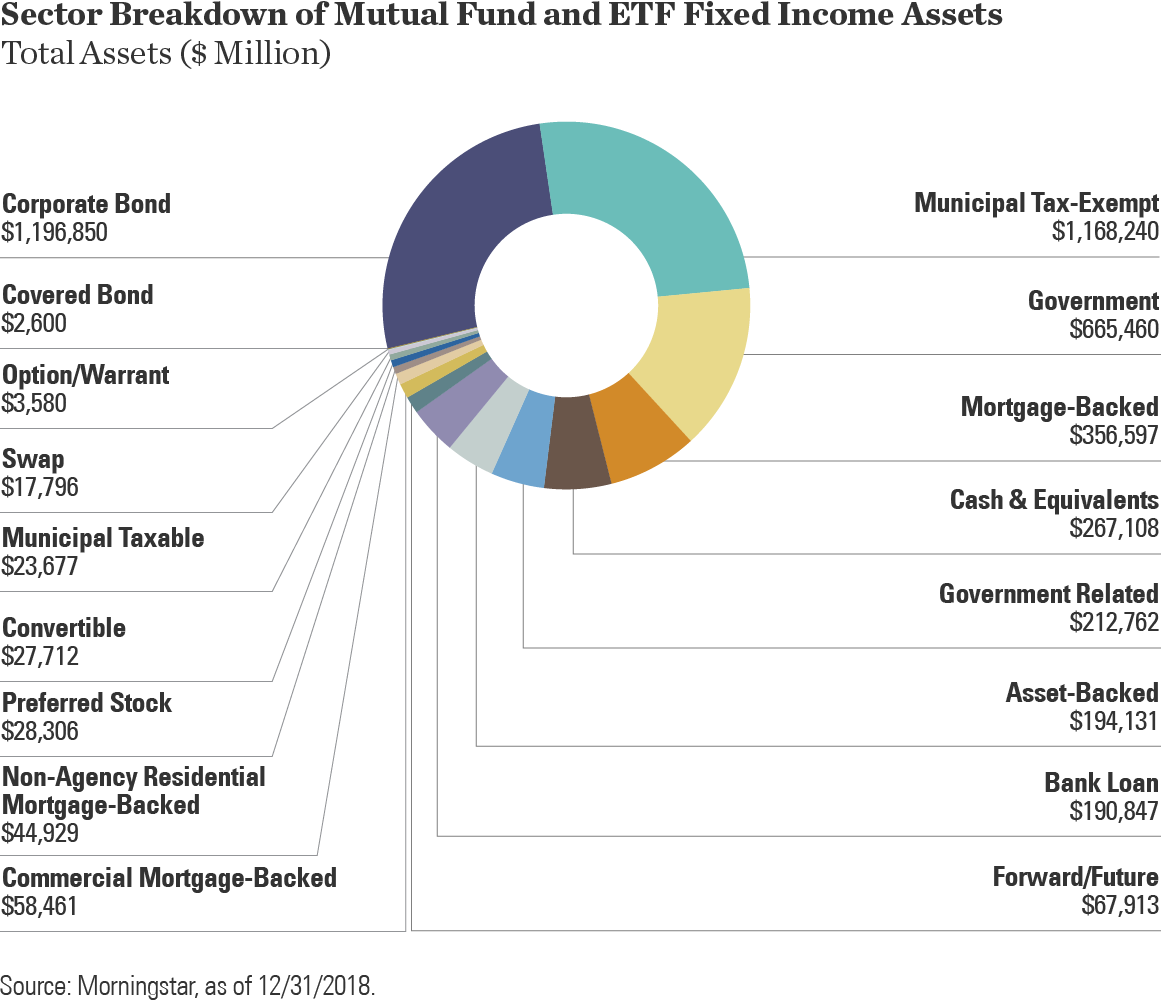

While the Fed aims to inform, and its report is full of useful fund flow data, I believe this 21% figure is confusing for the market, overstates the amount of debt held by fund strategies, and needs additional context. To provide this context, I broke out every bond held by a mutual fund or ETF into its sub-asset class category, as defined by Morningstar, to determine its exact ownership. The analysis primarily created one portfolio, building up the entire mutual fund and ETF universe to identify what type of fixed income security is held by the fund, essentially creating a very large master portfolio.

The analysis’ major finding, illustrated below, is that out of the $4.5 trillion total US-listed mutual fund and ETF fixed income assets under management, there are only $1 trillion of assets (both active and index-based) invested in corporate bonds.

View Larger

This $1 trillion figure represents only 9.9% of the global market value of corporate debt, as measured by the market value of the Bloomberg Barclays Multiverse Corporate Index.9 This is far less than the 20% figure cited by the Federal Reserve. The reason why the Federal Reserve reports a higher number is a result of its more blunt approach to categorization, which only breaks down debt type classifications into five types. The more granular approach we have used results in a lower figure. Lastly, with index-based funds representing a 26% market share in US mutual fund and ETF assets, a significant portion of those corporate bonds are actively managed. This further discredits the myth that a bond bubble is being fueled by autopilot, robot-like index exposures.

Using data to build confidence in fixed income ETFs

A lot of myths and #FakeNews percolate throughout the investing landscape, creating confusion for investors. All of the above data shows there is no passive bond bubble, and investors should seek fixed income ETFs with confidence to build better bond portfolios.

The proliferation of ETF exposures into non-traditional asset classes like bank loans, emerging market debt and convertibles, has widened the scope of tools at investors’ disposal. So has the ability to use ETFs to separate out the entire credit curve and yield curve. When investors expand their toolkit to consider the full spectrum of fixed income ETFs, they may realize the full power of fixed income ETFs to efficiently construct customized portfolios.

To learn more about fixed income ETFs, check out some of our recent blog posts.

© State Street Global Advisors

Read more commentaries by State Street Global Advisors