Key Takeaways

- Positive fundamentals are driving growth in cash flows

- Companies are embracing capital discipline and improving governance

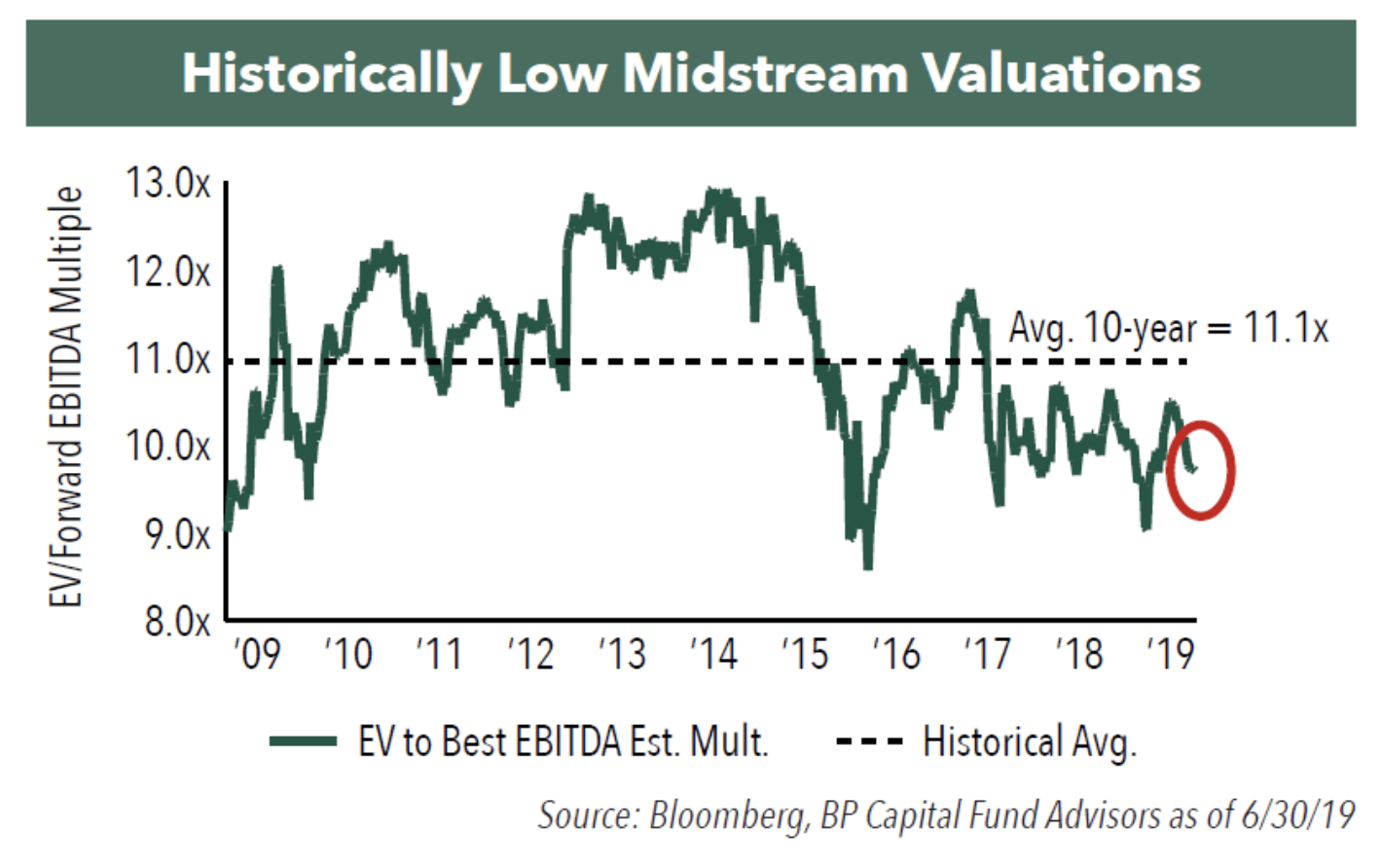

- Stock valuations are at historically low levels

- Payouts are projected to rise, which should drive stock prices higher

Background

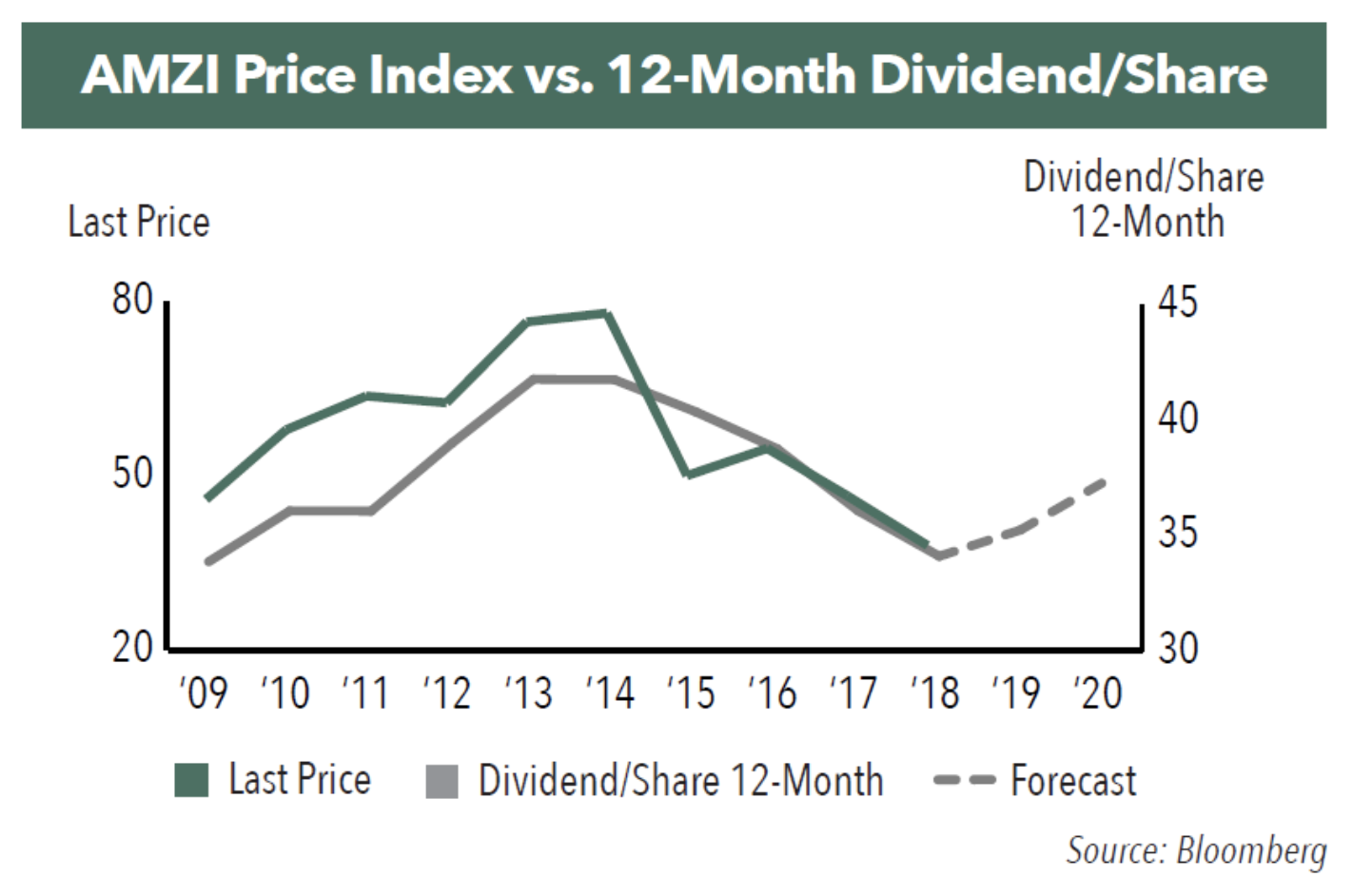

The decline in the price of oil from 2014 to 2016 hurt midstream companies’ cash flow growth, and as a result, many cut their capital spending budgets and their distributions. The Alerian MLP Infrastructure Index (AMZI) saw its trailing twelve-month distribution per share fall from a high of $43 in October 2014 to $33 in June 2019. The stock prices of midstream companies retreated also, following the decline in distributions.

Today - Improved Fundamentals, But Low Valuations

There have been many significant, positive changes for midstream energy companies over the last few years:

Return to Growth in Cash Flow. Midstream companies are benefiting from the rapid growth in production of crude oil and natural gas in the U.S., with higher volumes flowing through their gathering, processing, pipeline, and storage assets. This has, in turn, led to higher revenue and cash flows. Cash flows have been rising steadily since the beginning of 2017, and the first quarter of 2019 marked the eighth consecutive quarterly increase in cash flow generation for midstream companies.1

Improved Capital Discipline and Stronger Balance Sheets. Management teams have shifted away from “growth at all costs” towards a more disciplined approach to growth focused on stronger balance sheets and more self-funded capital spending. Through a combination of moderated spending programs and higher cash flows, midstream companies have successfully increased the portion of capital spending funded with company cash flow from 7% in 2015 to 29% in 2018, with a further increase to 42% projected for 2019.1 Lower capital spending has meant less reliance on equity issuance to fund growth and the potential for more cash to be paid out in distributions. Balance sheets have also become stronger, with midstream company-level debt to earnings before interest, tax, depreciation, and amortization (EBITDA), moving steadily lower over the last few years as management teams have used cash to pay down debt.

Elimination of IDRs. A majority of midstream MLPs have addressed a major investor concern by eliminating Incentive Distribution Rights (IDRs). IDRs had diverted distributable cash flow away from limited partnership unit holders in favor of the GP, or general partner. In March of 2014, 70% of the AMZI was comprised of companies with IDRs, and by March of 2019, this figure had fallen to just 16%.2 As a result, we believe midstream companies are now better positioned to increase cash payouts to investors as company cash flow generation has continued to rise.