Abraham Lincoln said, “Discipline is choosing between what you want now and what you want most.” Alas, investors have indicated in recent weeks that what they want now is safety. From the beginning of May through the end of the first week in June, investors withdrew $36 billion from equity funds and poured $32 billion into bond strategies.1 Admittedly, it would be irresponsible of me to render an opinion on these investors’ all-too-predictable reactions to the recent news flow and market gyrations. I would need to better understand what each of them and their families want most.

If what they truly want most is to avoid all market drawdowns at any cost, then they probably wouldn’t have been invested in equities to start. I’m willing to speculate that many of these equity-selling investors had been targeting growth in their portfolios to fund the things they really want most: to finance their children’s education, to support and enhance their children’s true skills, to fund philanthropic efforts, to build comfortable lifestyles in retirement, and more.

If that’s the case, then in recent weeks many families have likely been breaking from their long-term plans because of a few bad trade headlines. That’s unfortunate for a few reasons.

Three reasons to maintain a long-term view

First, in the first 11 trading days of June, the market, as represented by the S&P 500 Index, was up 5.11%.2 May’s price losses have almost entirely been recouped, at least for those investors who stuck around for the near-term recovery. This should come as little surprise to investors. Historically, the best days and weeks in the market (example, June 2019) have tended to group with the worst days and weeks in the market (example, May 2019), making it a fool’s errand to attempt to time the market.

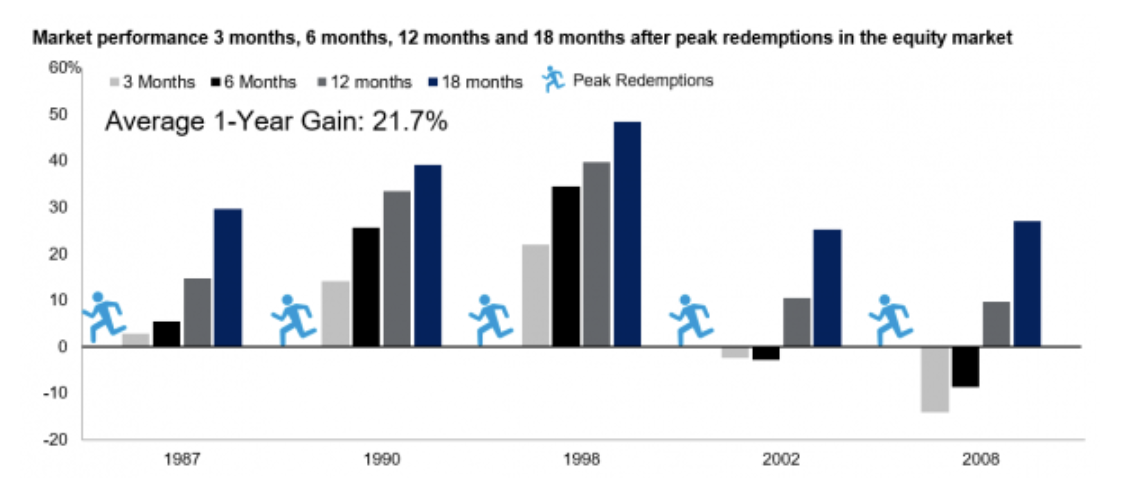

Second, markets have tended to perform well after peak redemptions. Typically, by the time most investors attempt to get defensive, it is often too late. Case in point, the average one-year S&P 500 Index gain following peak equity fund redemptions after the 1987 crash, the early 1990s recession, the 1998 Asian currency crisis, the early 2000s recession, and the 2008 financial crisis is 21.7%.3

Markets have tended to perform well after peak redemptions

Source: FactSet Research Systems. Peak redemption months for equity flows are 10/31/87, 10/31/90, 8/31/98, 7/31/02, and 10/31/08. All returns are total return and calculated cumulatively on a monthly basis. Past performance does not guarantee future results.

Third, a primary underpinning of this elongated cycle has been accommodative monetary policy by the world’s central banks, designed to reflate the economy and global financial markets. I believe the ongoing “trade war” and May’s coincident tightening of financial conditions likely serves to extend the Federal Reserve’s more-dovish monetary policy stance indefinitely, thereby likely extending the cycle. Already this is the longest cycle on record dating back to 1854 (when Lincoln began his failed Senate campaign). To call it the “unloved cycle” may be understatement. Each passing year has brought yet another event that worries investors — European debt crisis, fiscal cliffs, debt ceiling debates, elections, Brexit, and more — only for markets to reach new heights. The same US macroeconomic backdrop of slow growth, benign inflation, and accommodative monetary policy that propelled markets higher to this point has not changed.

Define what you want most from your portfolio

I believe investors would be well-served to define what they want most. They should work with their financial advisors to define the purposes of their money, to articulate their missions, and to allocate their capital in manners that are aligned with their well-articulated long-term goals.

If investors are truly targeting growth in their portfolios, then they should be prepared to cope with inevitable gyrations in the market and not break from their well-structured plans. Or as Lincoln said, “Be sure to put your feet in the right place, then stand firm.”

Learn more about strategies that can help investors target growth in their portfolios.

1 Source: Investment Company Institute. Data includes mutual funds and exchange-traded funds.

2 Source: Standard & Poor’s, Bloomberg, L.P. as of June 17, 2019

3 Source: FactSet Research Systems, Dec. 31, 2016. Peak redemption months for equity flows are 10/31/87, 10/31/90, 8/31/98, 7/31/02, and 10/31/08. All returns are total return and calculated cumulatively on a monthly basis. Past performance does not guarantee future results.

Important information

Blog header image: Josh Calabrese/unsplash.com

The opinions referenced above are those of Brian Levitt as of June 21, 2019. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

Brian Levitt is the Global Market Strategist, North America, for Invesco. He is responsible for the development and communication of the firm’s investment outlooks and insights.

Mr. Levitt has two decades of investment experience in the asset management industry. In April 2000, he joined OppenheimerFunds, starting in fixed income product management and then transitioning into the macro and investment strategy group in 2005. Mr. Levitt co-hosted the OppenheimerFunds World Financial Podcast, which explored global long-term investing trends. He joined Invesco when the firm combined with Oppenheimer Funds in 2019.

Mr. Levitt earned a BA degree in economics from the University of Michigan and an MBA with honors in finance and international business from Fordham University. He is frequently quoted in the press, including Barron’s, Financial Times and The Wall Street Journal. He appears regularly on CNBC, Bloomberg and PBS’s Nightly Business Report.

Read more commentaries by Invesco