Weighing the Week Ahead: Four Risky Hurdles

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is massive, and that is just the start. Earnings season is in full swing. US/China trade talks resume. And finally, the FOMC announces its interest rate decisions. Expect plenty of commentary on the individual news items, but the real question is:

How deftly can the market leap the four hurdles? (Data, Earnings, Fed, and Trade = DEFT).

Investor need a framework to interpret the breaking news.

Last Week Recap

In last week’s installment of WTWA, I drew upon some recent articles from others to address the question of “dumb money.” There were some excellent reader reactions, especially on Seeking Alpha. I hate it when blogs start name calling instead of analyzing data. The authors’ time would be better spent taking a deeper look at their own methods. As I suspected, the pundits embraced the bull/bear debate, but in less colorful fashion.

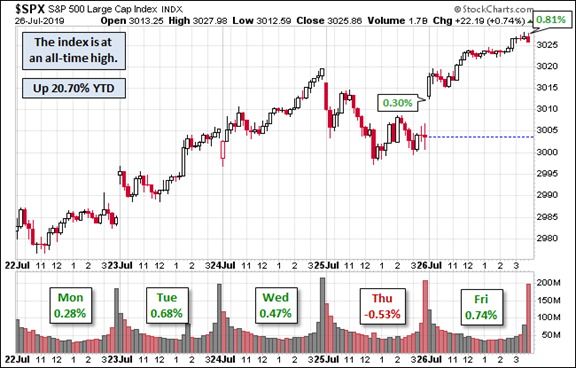

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, which combines a lot of information in one picture. The full article also includes several other interesting takes on price movement.

The market gained 1.6% for the week. The trading range was only 1.7%. This erased last week’s losses in a quiet, low-volatility continuation of the rally. My weekly Quant Corner translates this into a volatility calculation which you can compare both to VIX and to past readings.

Personal Note

I missed my regular summer challenge at the North American Bridge Championships. Instead, Mrs. OldProf sent me on a scouting mission to Arkansas, as we continue our search for a semi-retirement home. When my Arkansas breakfast was served, I asked what the bowl of white stuff was. My server said, “Those are your grits.” I asked how one consumed them. She patiently explained alternative methods and affirmed that a spoon was the right utensil.

No WTWA next week (or perhaps a light version) as our search continues. So far, we have visited Covington, Ky (Cincinnati), Knoxville, Asheville, Charlotte, Raleigh/Durham, and Central Florida. Still on the program are Florida’s West Coast and Phoenix.

Noteworthy

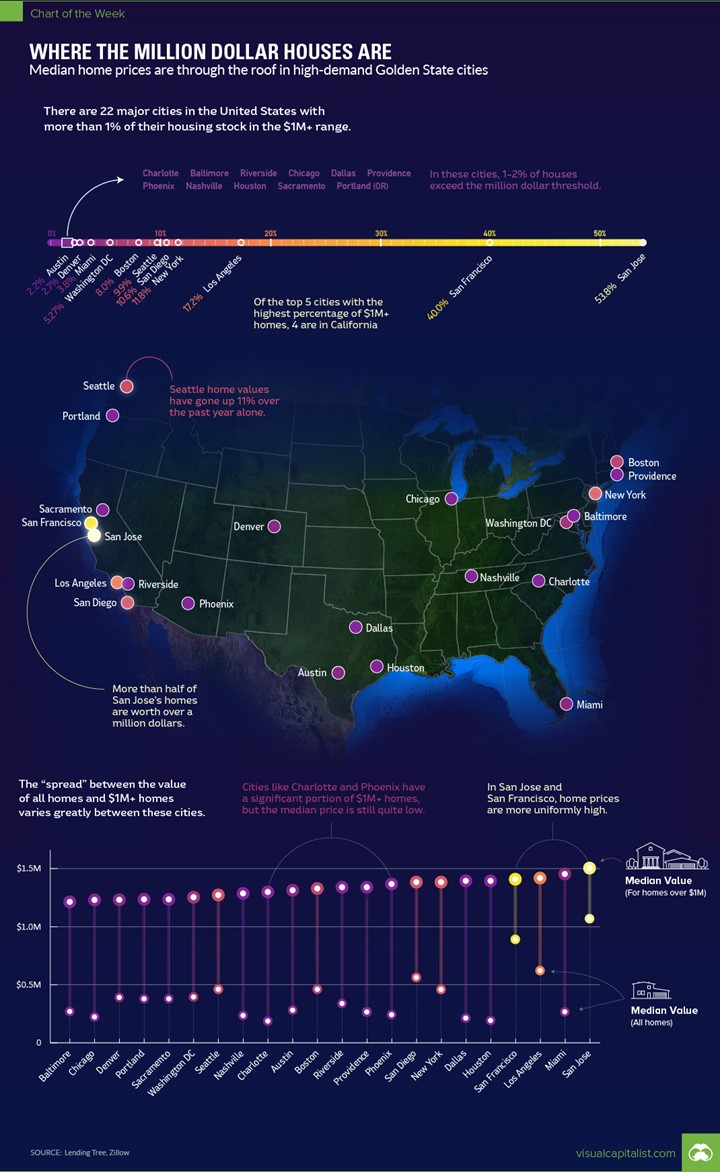

The Visual Capitalist looks at the increase in million-dollar homes, city-by-city. The full post has other interesting charts. In this one, I especially like the comparison between the median for $1 million + homes and all homes.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. There are three different groups corresponding to different time frames. The unanimously positive picture from a week ago did not last long. Short-term indicators are now slightly negative. NDD is concerned about some of the components of the long-leading indicators. He compiles useful data and is honest about his own interpretation.

The Good

-

Durable goods orders for June Brian Wesbury

Orders for durable goods surged in June, rising for every major category. Yes, the volatile transportation category rose 3.8% in June, but orders outside the transportation sector increased 1.2%, easily beating expectations. Machinery orders led the way outside transportation, rising 2.4%, the largest single-month increase for the category since early 2018, when the new tax law added incentives for investment in the form of accelerated depreciation. Primary metals and fabricated metal products also had the largest monthly gains in 2019, rising 0.8% and 2.1%, respectively. While the pouting pundits may point to the deceleration in durable goods orders over recent quarters as a sign the economy is slowing down and reason for the Fed to cut rates, the slowdown is almost entirely due to aircraft.

- Initial jobless claims declined to 206K versus expectations and prior of 215K and 216K.

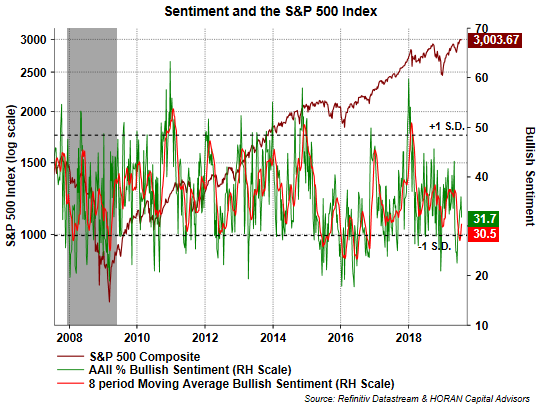

- Market sentiment is still negative as measured by the AAII index or ETF fund flows. David Templeton (HORAN) provides his usual solid analysis.

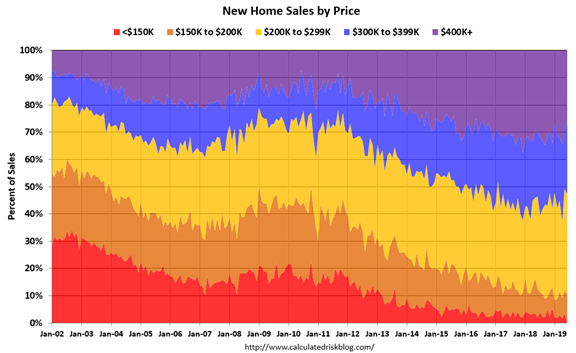

- New home sales for June registered 646K (SAAR) higher than the downwardly revised 604K and slightly missing expectations of 660K. Calculated Risk analyzes the data, noting that falling prices represent good news. No longer forced to compete with distressed sales, builders are increasing homes to meet first-buyer demand.

- Q2 GDP for the first estimate was an increase of 2.1% beating expectations of 1.8% but weaker than Q1’s 3.1%. There were also revisions to past years making this report into a political football (pre-season). As I noted at the time, Q1 was not as good as it seemed – too much inventory and trade effects. I’ll take a deeper look at the competing claims pundit and political clais in the near future. Scott Grannis has an interesting take on the revisions and trends. Bob Dieli’s report will also be available soon.

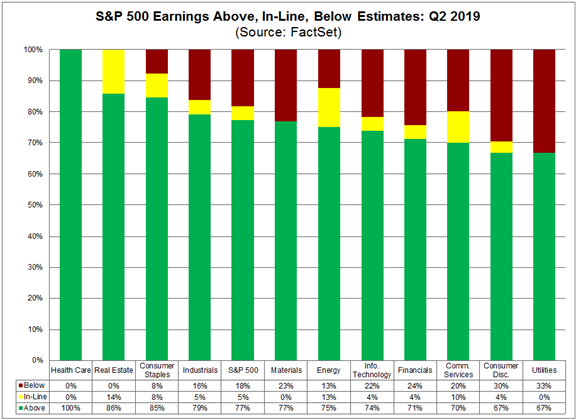

- Corporate earnings are beating estimates. Yes, the estimates have been lowered, but revenues and outlook are also below the five-year average (FactSet).

The Bad

-

Hotel occupancy decreased last week by -0.5%. (Calculated Risk).

-

Rail traffic remains in contraction for Steven Hansen’s “economically intuitive” sectors. (GEI). The four-week rolling average year-over-year comparison is slightly better. He also is negative on trucking, which is still growing, but at a slower pace. (GEI).

-

Existing home sales for June were 5.27M (SAAR), slightly below expectations of 5.3 M and May’s 5.36M.

-

FHFA home prices for May increased 0.1% versus April’s 0.4%.

The Ugly

Your safe deposit box? Really? When is the last time you checked it? (NYT).

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

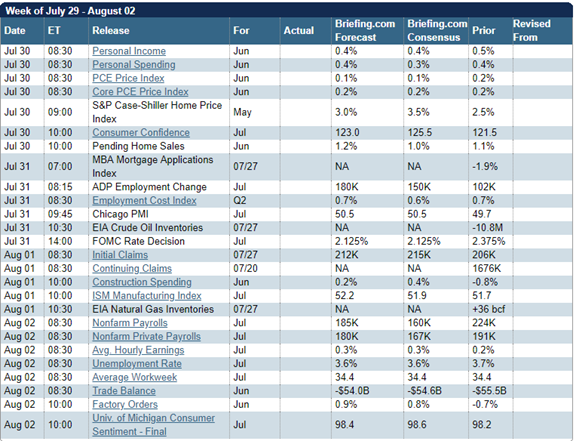

The economic calendar is a big one. Personal income and spending, PCE prices, consumer confidence, and the ISM manufacturing index are all important. And of course, the most significant of all is the monthly employment situation report.

It is also the heart of earnings season. We’ll get the FOMC rate decision on Wednesday and probably some news on the US/China trade meeting right before that. While everything may come in as expected, there is the potential for plenty of action.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

There have been many busy weeks this year, but this one may take the top ranking. There are four types of information, each representing a hurdle for stocks:

- Data – including the most important reports.

- Earnings – of special interest this season.

- Fed decision – many think they know the answer, but these experts are confident of quite different outcomes!

- Trade – where we get the first sign of potential progress between the US and China since the G20 meetings.

The DEFT hurdles. Let’s take a closer look at each. I’ll contrast the likely viewpoints and suggest something the experts will be watching.

|

Hurdle |

Mainstream |

Bearish |

Bullish |

Expert Edge |

|

Data |

Mixed and confusing, as we have seen in recent weeks. |

Widespread weakness, especially in employment and ISM manufacturing |

Stability in employment growth trends. Improvement in manufacturing Continuing high levels of confidence. |

Watch business investment in ISM – a weak spot in GDP. Also consumer outlook on employment, a good check on the regular data. |

|

Earnings |

Small decline |

Start of earnings recession. |

Enough earnings beats to avoid a quarter of declines. |

Watch changes in forward earnings, the basis for stock pricing. Current results provide a foundation. |

|

FOMC |

25 bps cut |

No cut |

50 bps or strong signal for 25 more |

Any dissents. There is some genuine disagreement. The dot plots. Phrases that suggest dependence on data. |

|

Trade |

“Ceremonial” progress announced |

Another walkaway, with hardline attitudes on Intellectal Property, bleeding into threats. |

Some substantive progress on rules, future agenda, possible compromises. A few specific details. |

Do the US & China announcements match on specifics like agricultural purchases. No threats to specific companies. |

Another wild card is the timing. Trade news might come out right before the Fed announcement. The employment data will be released on Friday, two days later.

And no, the Fed does not get a Wednesday look. The Fed Chair, the President, and a few others get an advance report on Thursday afternoon.

I’ll add a few more conclusions in today’s Final Thought.

Quant Corner and Risk Analysis

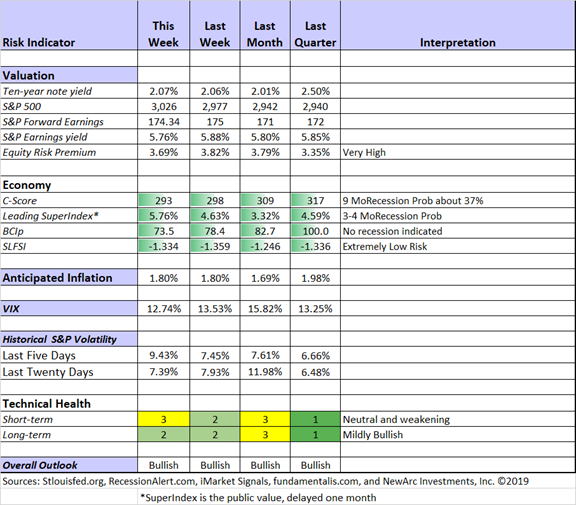

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term technicals deteriorated to neutral, but long-term remain mildly bullish. Recession risk is still in the “watchful” area.

Consider all factors, my overall outlook for investors is bullish.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Guest Sources

James Picerno is concerned, asking, Will Weak Housing And Manufacturing Sectors Lead To Recession?

New Deal Democrat writes, Housing has Bottomed.

Calculated Risk also sees improvement in new home sales, the most important component.

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I tried to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades are certainly not for everyone.

Stock Exchange has moved to Tuesday publication. As I wrote last week, I am doing this to create more separation between the stocks discussed and our own adjustments. While we warn investors that these are just ideas. They are not intended for readers to follow without research or determining the suitability for their portfolios. We also warn that we may trade out of positions without notice. Even with all of that in mind, a little more separation between publication and trading would be better.

This week’s edition analyzes when model’s “go wild” and the issues with human intervention. We share some picks from Athena (now fully invested) and Holmes (only 10% invested). The technical choices are often in sharp contrast to fundamental analysis. Pulling it all together is our regular series editor, Blue Harbinger.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Joe Wiggins Investment Risk is a Behavioural Phenomenon Not Just a Number. It is an excellent discussion about how feelings affect our relationship with risk. It distorts our view of probabilities and outcomes.

An excellent example of this is psychologist Gerd Gigerenzer’s notion of ‘dread risk’, which he defines as a fear of low probability high consequence events. Gigerenzer claims that a reluctance to fly following the terrorist attack in New York on September 11th 2001 meant that more Americans lost their lives on the road due to their desire to avoid flying in the following three months than died as a direct result of the horrific attacks[ii].

Decision-making about insurance is a contradictory treatment.

He provides the excellent example of two identical portfolios, one locked up for five years and the other traded daily. Fundamentally, the overall outcome should be the same, but this is not so.

The listed portfolio will suffer far greater price fluctuations than the private portfolio and offers the investor the ability to react to these variations (they can buy and sell); by contrast, the private equity portfolio will report smoother prices for the underlying securities, and the investor will be unable to trade – the less observable price fluctuations the less opportunity for us to react emotionally to them. The behavioural risk (that we make bad decisions) is significantly greater in the public equity option than the private equity option. This is by no means a validation of private equity structures, rather an example of how risk is about far more than the underlying characteristics of any asset.

[Jeff] This explains why some investors embrace non-traded REITs or BDCs instead of a publicly traded dividend portfolio. It is a belief that what you don’t know can’t hurt you. This is a post well worth reading carefully.

Stock Ideas

Chuck Carnevale has another update of his principles for portfolio construction. Hint: It is a very personal process.

Achilles Research likes the high-yielding Annaly Capital (NLY). Hint: The reduced payout is more sustainable.

The Boeing (BA) battleground has two distinct sides. Peter F. Way’s market-maker behavior ratings signal institutional support. Southwest has adjusted routes due to its grounded 737MAXs and is now seeking compensation from Boeing.

Josh Brown explains why market weakness may be a good thing for younger investors. Maybe so. For those near retirement I prefer avoiding recessions and finding an income program that lets you reinvest when the market declines. After all, 70 is the new 50!

Sure Dividend has four ideas for stocks to buy and hold forever.

Personal Finance

Abnormal Returns is the go-to source for anyone serious about the investment business. The Wednesday edition has a special focus on personal finance, with plenty of ideas for the individual investor. I especially enjoyed Richard Quinn’s discussion of Social Security, where many misperceptions prevail. The many good points are difficult to summarize.

I also placed two other items from the weekly AR personal link in other parts of this post. It is a valuable weekly resource.

Watch out for…

The “romance scam.” Ex-scam artist Frank Abagnale reveals some secrets about modern versions of old scams.

Uncle Sam wants you! The IRS is looking for those who might not have reported income from cryptocurrency trading (Forbes).

Final Thought

The four hurdles are a good test for the market, but we should know what to expect. This week’s table is designed to help with that problem. One additional concept to keep in mind is that 2 – 2.5% GDP growth is acceptable for markets, as long as we get earnings growth as well. Expect plenty of commentary to suggest that any weakening in any indicator is the beginning of the end.

The biggest current mistake from most analysts is predicting the extent of an indicator move from the first change in direction. This is usually accompanied by a chart of past peaks with red semicircles over them and a prediction for the current downturn. Even a cursory study of such charts shows that past potential peaks do not get the semicircles when the indicator once again changes direction.

Indicators do not move smoothly. The switches can be sharp, especially if news driven.

Several of my most astute and successful sources see some confusion in the current data. Bob Dieli reports that this is normal at this point of the business cycle (the “boom” phase). Scott Grannis sees the same, as does New Deal Democrat.

My own take? Much of the action is driven by two factors:

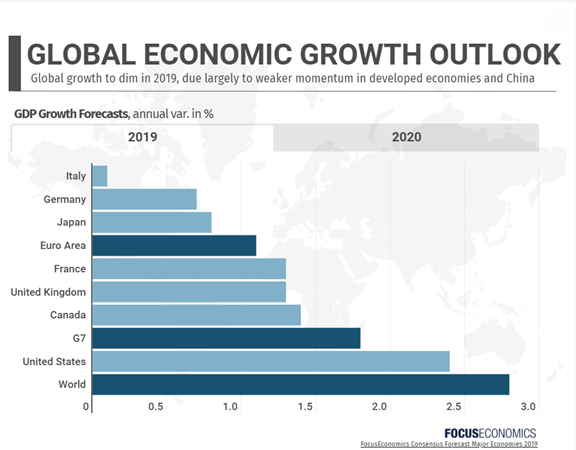

- The ten-year note seems tied to European rates. This is not a false signal, but it is different from past eras. I look to global economic growth analysis. The key growth rates are a bit lower, but all positive. Are we really supposed to panic over 6.2% growth in China. Focus Economics does a detailed analysis of each G7 country. Here is a summary. Please note that the European Central Bank is fighting the weakness. Remember the incessant discussion of the PIIGS?

- Tariff effects are larger than most realize and are therefore not “in the market.” Analysis breaks down for most people when there is the need for a comparison with a counterfactual. Since the economy is still growing, people (including highly-paid analysts) gloss over the drag for costly policies. This warps the perspective for world growth and the upside for stocks.

Most news sources have an incentive to be first in making a big call. Investors are not rewarded for being “early.”

Being early is the euphemism for being wrong.

Some other items on my radar

I’m more worried about:

- A no-deal Brexit. New PM Boris Johnson is a wild card for Brexit and world markets. (The Economist).

I’m less worried about

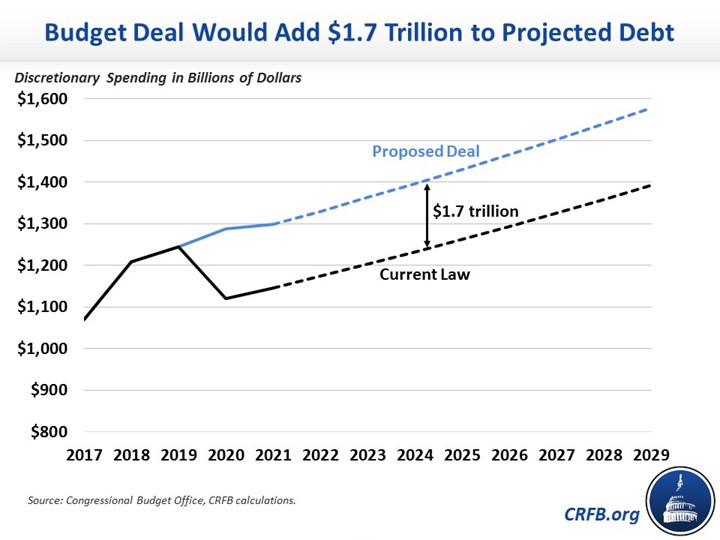

- The debt ceiling increase. Why the debt limit is not the real issue (Econofact). As a citizen, you might hate the budget deal. Five Reasons to Oppose the Budget Deal. As investors, we should hold our noses and be happy that a major problem has been avoided. (Write for my commentary on this if interested).

- FAANG stock weakness. Paul Schatz sees Lots of Sideways Action – Could Lead to Another Leg Higher. I expect and embrace a change in leadership.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All