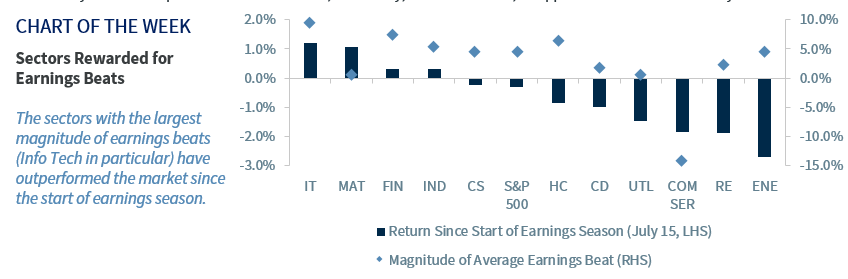

Key Takeaways

- The S&P 500 is off to its best start to a year (19.9%) since 1996.

- A budget deal and earnings have been recent catalysts.

- The fed, earnings, and data are key items to watch next week.

In my travels this week to Dallas, I discovered that the 2019 Horseshoe Pitching World Championship was underway in Wichita Falls, TX, running from July 22 through August 3. I wish I could have stayed to participate (they have all levels) as horseshoes is a great game of skill (and a little luck)! The game involves two individuals throwing two horseshoes (also called ‘pitches’) each in a series of innings with the first to reach 40 points winning the match. Three points can be scored by notching a ‘ringer’ (horseshoe surrounds the stake) and one point is earned by throwing a ‘leaner’ (horseshoe within six inches of the stake). Avoiding ‘dead shoes’ (horseshoes that are not eligible to score) is paramount. Given the record level of equity prices, with the S&P 500 posting its best start to a year (19.9% through July 23) since 1996, the below four catalysts (‘pitches’) need to continue to score if the market is to maintain its upward momentum. We remain cautious in the near term as the ‘tosses’ next week get more challenging as the stakes grow at such elevated levels.