Summary

Small cap stocks within emerging markets have outperformed large cap stocks (i.e., MSCI EM) by around 0.5% annualized since January 2000. However, Illiquid stocks (regardless of capitalization) have outperformed large cap stocks by around 3%. This illiquidity premium is related to, but not the same as, the small cap premium. This opportunity is all the more enticing as it sits atop emerging markets, an already attractive asset class, and offers active managers a large selection universe of approximately 2000 firms.

Serendipity

We have been investing in emerging market (EM) stocks across the capitalization spectrum since 1993. As is typical in quantitative processes, stocks have been chosen based on a trade-off between returns, risk, and transaction costs. Over this period, the contribution from small cap stocks has been additive, perhaps unsurprising as a long tail of over 2000 lesser-known under-followed securities offered plenty of opportunities for an active manager to add value. But, for every stock with a high expected return, there were other stocks with an even higher expected return that the optimizer would bypass because the transaction costs were too high. We viewed these high returns as a mirage because the extra return was outweighed by the prohibitive expense – after all, that is the precise purpose of a trade-off function. But what if there were a way to tap into these missed opportunities without incurring the corresponding costs?

We undertook a project to study this tail of stocks intensively and in doing so uncovered a notable finding – the premium in emerging lies not in size, but in illiquidity.

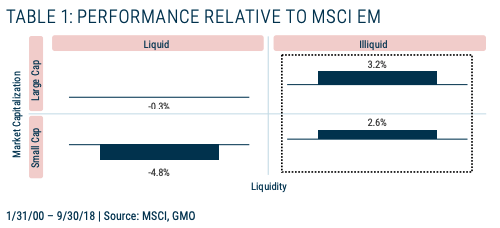

Small cap stocks within emerging have outperformed large cap stocks (i.e., MSCI EM) by around 0.5% annualized since January 2000. However, illiquid stocks (regardless of capitalization) have outperformed large cap stocks by around 3%.

The matrix shown in Table 1 makes the contrast clear. Note that the return premium has been in illiquid space (right column) and not in small cap (bottom row). In fact, note that investing in the liquid part of small cap (bottom left box) has actually cost approximately 4.8% relative to MSCI EM annualized since 2000. Of course, active management in this space can identify large alpha opportunities, but that’s a rather large hole to dig out of.

Why Should We Expect a Premium for Illiquidity?

There is no free lunch. Investors are only compensated for risks that others are not willing to bear. The well-documented value premium stems from, among other things, the willingness to own companies that are growing more slowly than the market. An investor purchasing something illiquid, by definition, gives up the ability to quickly dispose of the asset. This is the term premium in bonds and illiquidity premium in equities. And an inability to quickly sell a position should arguably drive more of a premium in equities than bonds because the potential change in prices during the time the investor takes to unload his or her investment is higher for equities.

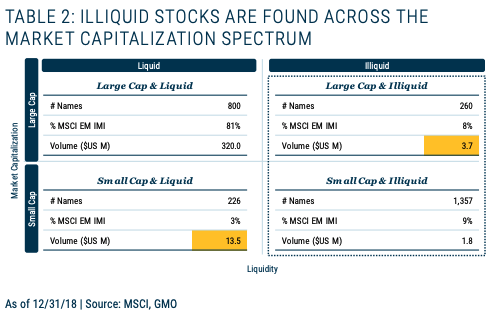

The illiquidity premium is related to but not the same as the small cap premium. The small cap premium arises from a dearth of knowledge about a firm in addition to low coverage by analysts. The range of possible outcomes is therefore larger, and this uncertainty leads to a higher expected return. However, this is not the same as illiquidity. There are several small cap firms that are not illiquid (bottom left in Table 2) and, conversely, several large cap firms that are illiquid (top right in Table 2).

Empirical Evidence

As we want to study illiquidity, we screen purely for illiquidity and select all illiquid firms regardless of their size. There are multiple ways to measure illiquidity. The classic measure is daily traded dollar volume. Another is stock turnover (shares traded daily divided by total outstanding shares). An interesting twist comes from Professor Yakov Amihud. In a 2002 paper,1 he defined illiquidity as the ratio of the change in price to the dollar volume of shares traded. An illiquid stock according to Amihud is one for which the price jumps a lot with a relatively small trade. There is high correlation across these measures. In fact, our analysis shows that our two favorite measures, daily volume traded and Amihud, have a 0.9 correlation.

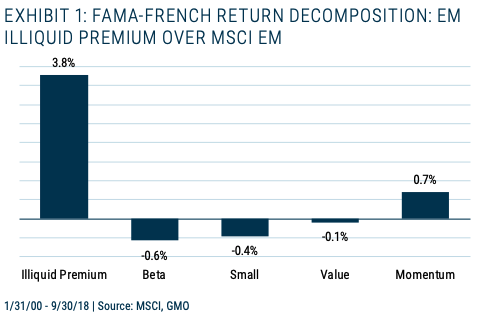

We have empirically tested that illiquidity is not a proxy for size, value, momentum, or beta by regressing the returns against illiquidity and these other factors. The return accruing to illiquidity is quite high (see Exhibit 1).

A natural concern with regressions over a long period such as that above is that they display the averages and do not shed light on the worst-case scenarios. In the case of an investment in illiquid stocks, that would presumably be the impact of an extended drawdown. Fortunately, we have such a period in our dataset. The Global Financial Crisis spanned about 16 months (November 2007 to February 2009) from peak to trough. Surely, this is long enough for investors to recognize and appropriately mark down illiquid firms. The figures are reassuring. The drawdown in illiquid was slightly better (around 60%) than that suffered by the liquid part of the market (around 65%) over this period.

So, There Are $20 Bills on the Sidewalk?

Not quite. The illiquidity premium cannot be captured by the standard quantitative investing/trading regimen. In fact, our estimates suggest that if done this way, the cost effectively cancels the premium offered.

The only way to capture the premium is by tailoring an approach specifically for illiquid stocks. Each of the investment components – product structure, alpha signals, and trading style – need to be designed to leave as light a footprint on the liquidity surface as possible.

Importantly, such a strategy should carefully monitor capacity and require considerable advance notice for any shareholder transaction activity.

The alpha signals should ideally have a long horizon, low turnover, and encompass many names.

A thoughtful trading approach is another critical component. Harvesting the illiquidity premium requires the skill of a trading team that has deep experience operating in emerging markets and plenty of patience. Ideally, traders should be given a long list of buys/sells and have flexibility along both dimensions: time to completion and which names to trade. This will allow them to fully tap into their knowledge of the sources of liquidity (which could vary by stock) and play the waiting game to the limit.

We believe an approach that incorporates all these components can successfully capture some of the elusive illiquidity premium.

A Winning Combination

Most of the arguments presented thus far have more to do with illiquid stocks generally than with EM illiquid stocks specifically. Having said that, EM illiquid has some additional advantages that are specific to the asset class.

Based on our analysis, emerging markets, specifically EM Value, is one of the cheapest asset classes we see today. As of May-end 2019, the GMO Asset Allocation team’s 7-Year Asset Class forecasts for EM and EM Value are 5.0% and 9.5% real, respectively. For reference, this compares to a U.S. Large Cap forecast of -2.7% real.

Emerging markets encompass roughly 2800 companies, of which approximately 2000, very impressively, are illiquid by our definition.

EM Small Cap is at the periphery of equity investing for most clients. EM illiquid is a step further removed in awareness and comfort.

So, for investors who are willing to look deeper into this opportunity and be more long term in their horizon, we believe the payoff is manifold – a sizable illiquidity premium added on to the enticing beta of EM Value, all wrapped up with the alpha of a huge opportunity set – in a space that is unlikely to be crowded out.

Binu George Mr. George is a portfolio strategist for GMO’s Emerging Markets Equity team. Prior to joining GMO in 2009, he was a portfolio manager with AXA Rosenberg. Previously, Mr. George worked in several roles encompassing research and investment strategy at Barclays Global Investors. Mr. George earned his B.Tech. in Civil Engineering from Indian Institute of Technology, Madras and his MBA in Finance from University of Rochester. He is a CFA charterholder.

GMO’s 7-Year Asset Class Forecasts represent real return forecasts for the above-named asset classes and not for any GMO fund or strategy. The forecasts above are forward‐looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward‐ looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward‐ looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from the forecasts above.

Disclaimer

The views expressed are the views of Binu George through the period ending August 2019, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2019 by GMO LLC. All rights reserved.

© GMO

More Fixed Income Topics >