It was an eventful week. The Fed lowered short-term interest rates, as expected, and ended the unwinding of the balance sheet two months early, but Chair Powell disappointed stock market participants by describing the move as “a mid-cycle adjustment” rather than the start of a series of rate cuts. In his press conference, Powell repeatedly noted that the Fed’s move was taken to insure against the downside risks from trade policy uncertainty and slower global growth, to counter the impact these factors are already having on the economy, and to help boost inflation back toward the 2% goal. Powell did not make a judgement on whether tariffs were ill-advised – that’s not the Fed’s job. President Trump expressed disappointment on the size of the Fed’s move, but then further escalated the trade war the next day, imposing a 10% tariff on the remaining $300 billion in imports from China. Unlike previous tariffs, which applied mostly to manufacturing inputs and intermediate goods, this latest round hits finished goods – consumer goods, in particular.

The shorter version. Powell: “tariffs, tariffs, tariffs.” Trump: “hold my beer.”

Readers should be aware that tariffs are a misguided way to deal with bilateral trade deficits and misbehavior on the part of certain trading partners. Tariffs are a tax on U.S. consumers and businesses. Tariffs raise costs, invite retaliation, disrupt supply chains, and dampen business fixed investment. Much of this is now showing through in the economic data. The May 10th escalation in the trade war imposed a more significant drag on U.S. growth, but nowhere near enough to push us into a recession. However, as we’ve seen repeatedly this year, there are important psychological effects of the trade war on businesses and the financial markets.

Nonfarm payrolls rose by 164,000 in the initial estimate for July – a relatively strong pace, but there is a fair amount of statistical noise (the headline figure is reported accurate to ±110,000) and seasonal adjustment is often difficult (education and auto manufacturing posted gains, as unadjusted figures fell less than usual). Retail employment continued to decline. In the past, this has often coincided with weakness in consumer spending. However, courier jobs (including package delivery) continued to rise, consistent with the ongoing move to online shopping.

One month does not make a trend. Payroll growth has clearly slowed this year. As Powell noted in his press conference, that was expected. However, “the pace is above what we believe is required to hold the unemployment rate steady.” Payrolls growth of a little less than 100,000 per month is enough to absorb new entrants into the workforce. One of the key questions is whether job growth has slowed due to a weaker economy or due to reduced slack in the labor market.

Click here to enlarge

The unemployment rate held steady at 3.7% in July, but the percentage of workers involuntarily working part time fell further. Details in the report also showed a sharper rise in summer jobs for teenagers and young adults this year. That is consistent with strong labor demand, and a bigger hiring challenge may come in the fall, when they go back to school.

So far, the data suggest a limited impact on the overall economy from tariff, although we have probably not seen the full impact of the May 10th escalation. Factory activity has slumped (and had weakened well before May 10). Manufacturing firms note a negative impact from supply chain disruptions, but one that is more or less manageable. Tariffs on materials and industrial inputs can be offset partly by tightening other parts of the production and distribution process. Tariffs on finished goods, which is where the latest round will hit, are going to be more difficult. Still, it could be a lot worse. A 10% tariffs can be partly offset. You can’t hide from a 25% tariff.

The stock market has remained hyper-sensitive to the Fed policy outlook, but also to the trade war, which has gone from boiling, to a slow simmer, and back again. Consumer and business attitudes have also been driven by trade tensions, and as Fed Chair Powell noted in his press conference, that channel may have a bigger impact than the simple mechanics of tariffs on manufacturing and trade. Going forward, the Fed will continue to monitor trade policy developments, global growth, and inflation dynamics at home.

Data Recap – The FOMC lowered short-term interest rates, but the stock market was unhappy with Chair Powell’s characterization of the move as “a mid-cycle adjustment” (not the start of a series of rate cuts. Trade policy uncertainty and slower global growth has been a key issue for the Fed. President Trump expressed disapproval with the size of the Fed’s move, and escalated the trade war a day later.

The Federal Open Market Committee lowered short-term interest rates by 25 basis points and voted to end the unwinding of the balance sheet two months early (in August rather than October), citing “the implications of global developments for the economic outlook as well as muted inflation pressures.” Two FOMC members, St. Louis Fed President Esther George and Boston Fed President Eric Rosengren formally dissented in favor of keeping rates steady.

In his press conference following the FOMC meeting, Fed Chair Powell said the move was intended “to insure against downside risks from weak global growth and trade policy uncertainty; to help offset the effects these factors are currently having on the economy; and to promote a faster return of inflation to our symmetric 2% objective.”

The day after the FOMC meeting, President Trump tweeted that he would impose a 10% tariffs on the remaining $300 billion of Chinese goods imported into the U.S. Unlike previous tariffs, which applied largely to intermediate goods and materials (components for manufacturing), this latest round hits finished goods, especially consumer goods.

The July Employment Report was generally not far from expectations. Nonfarm payrolls rose 164,000, with a net downward revision of 41,000 to the two previous months. Private-sector payrolls rose by 148,000, a +136,000 average of the past three months (vs. +215,000 in 2018). Seasonal adjustment (the end of the school year and annual plant closings in the auto industry) appears to have been a minor factor, adding job gains in education and auto production. Average hourly earnings rose 0.3% (+3.2% y/y – a moderate pace). The unemployment rate held steady at 3.7%. Summer employment for teenagers and young adults rose more sharply this year.

Click here to enlarge

The ISM Manufacturing Index fell to 51.2 in July, vs. 51.7 in June and 52.1 in May. Growth in new orders edged up to 50.8 (vs. 50.0 in June). Production and employment growth slowed. Order backlogs fell for the third consecutive month (not good). Input price pressures retreated. Comments from supply managers signaled ongoing concerns about the impact of tariffs, but less worry than in June.

The Chicago Business Barometer sank to 44.4 in July, vs. 49.7 in June and 54.2 in May. New orders, production, and employment contracted.

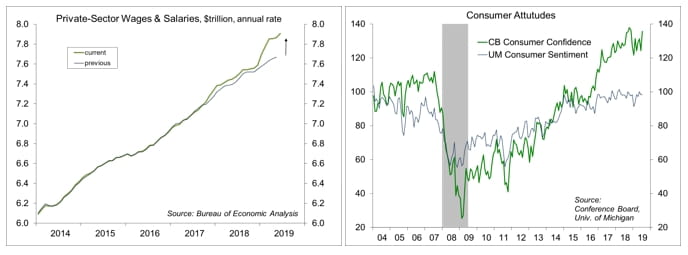

Personal Income rose 0.4% (+4.9% y/y), with private-sector aggregate wage and salary income up 0.5% (+5.8% y/y). Benchmark revisions showed a sharp pickup in income growth in the first quarter. Personal Spending rose 0.3% (+3.9% y/y), up 0.2% (+2.5% y/y) adjusting for inflation. The PCE Price Index rose 0.1% (+1.4% y/y), up 0.2% (+0.248% before rounding, +1.6% y/y).

Click here to enlarge

The Conference Board’s Consumer Confidence Index rebounded to 135.7 in the advance estimate for July, vs. 124.3 in June and 131.3 in May. The rebound likely reflects a retreat in tariff concerns, which had heated up in May and early June.

The University of Michigan’s Consumer Sentiment Index was little changed, at 98.4, in the full-month assessment for July (vs. 97.9 at mid-month and 98.2 in June). The figures have been in a relatively narrow range for the last several months.

Unit Motor Vehicle Sales slowed to a 16.8 million seasonally adjusted annual rate in July, vs. 17.1 million in June and 17.4 million in May.

The ADP Estimate of private-sector payrolls rose by 156,000 in the initial estimate for June, a +104,000 average over the last three months.

The Employment Cost Index rose 0.6% over the three months ending in June, up 2.7% from a year earlier.

Jobless Claims rose to 215,000 in the week ending July 27, leaving the four-week average at 211,500 – a low trend, partly reflecting more muted seasonal layoffs in the auto industry.

The Challenger Job-Cut Report recorded 38,845 announced corporate layoffs in July (figures are not seasonally adjusted), vs. 41,977 in June and 27,122 a year ago. Layoff intentions are still trending low, but the total for the first seven months of 2019 was 36% higher than the same period in 2018.

Factory Orders rose 0.6% in June (-1.2% y/y), boosted by a 75.1% rebound in civilian aircraft (-51.9% y/y). Orders for nondefense capital goods ex-aircraft rose 1.9%, slightly lower than the advance estimate, with shipments up 0.3% (revised lower).

The Pending Home Sales Index for existing single-family homes rose 2.8% in July (+1.6% y/y).

Construction Spending fell 1.3% in the initial estimate for June (-2.1% y/y), with a continued downtrend in single-family construction spending (-0.7% m/m and -8.5% y/y).

The U.S. Trade Deficit was little changed at $55.2 billion in June, vs. $55.3 billion in May. Exports fell 2.1% (-2.2% y/y), while imports slipped 1.7% (+1.2% y/y). The June figure was slightly higher than assumed in the advance GDP report (implying, all else equal, a bit more of a drag on the 2Q19 GDP growth estimate).

The Bank of England’s Governing Council left short-term interest rates unchanged, highlighted continuing uncertainty about Brexit, but retained a tightening bias (if everything works out okay).

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

More Fixed Income Topics >