Weighing the Week Ahead: Have the Facts Changed Your Mind?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is one of the smallest of the year. With last week’s market decline and increased volatility, pundits who are not on a summer vacation can do some navel-gazing and reconsider their conclusions. Or not. Most will be highlighting evidence that makes them seem smart, of course. What they should be asking is:

Did any of the new information change your mind?

Last Week Recap

In last week’s installment of WTWA, I described the four risky hurdles facing the market. My purpose was to provide a framework for analyzing the avalanche of news and data we would see in a very short time. The market did well with the early hurdles but failed to jump all four. I found last week’s matrix table helpful as I watched events, and I hope you did, too.

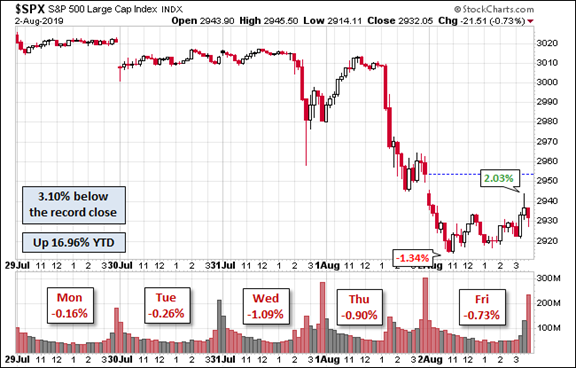

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, which combines a lot of information in one picture. The full article also includes several other interesting takes on price movement.

The market lost 3.1% for the week. The trading range was 3.8%. My weekly Quant Corner translates this into a volatility calculation which you can compare both to VIX and to past readings.

Personal Note

I will probably wind up in Mrs. OldProf’s doghouse for writing instead of taking the week off as promised. I’ll try to make it up with some downtime soon.

Thanks to readers for the many suggestions about the best places to live. Many have clearly found their ideal locations. We are looking at each, but we have some pretty restrictive criteria. I really enjoyed my trip to Northwest Arkansas, finding it quite attractive. But I am supposed to keep that secret.

Thanks also for the advice and great stories about grits. Another list of recipes to try, but probably not at home. Mrs. OldProf is an excellent cook, but the grits menu is not really in her wheelhouse.

Noteworthy

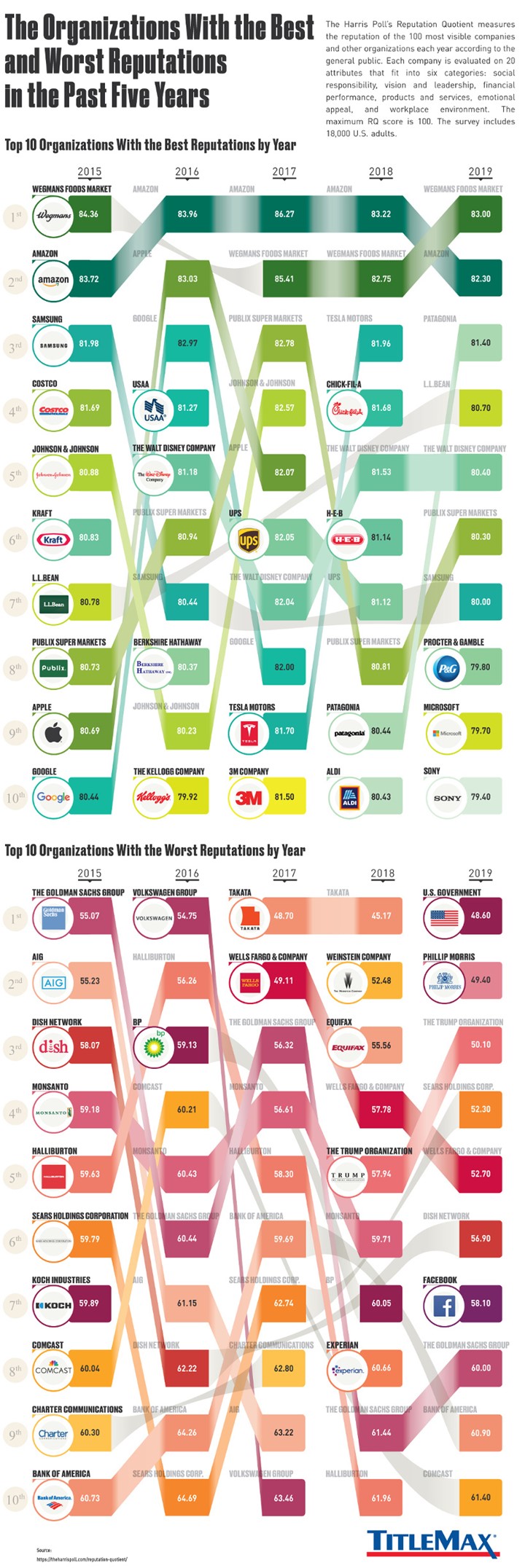

The Visual Capitalist draws upon data from TitleMax to create “top ten” and “worst ten” lists of organizations. The basis is a survey of 18,000 people considering twenty factors for each organization. You can also track the changes in each group over a five-year period. The worst organizations for 2019 include some that had not made the list before.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. There are three different groups corresponding to different time frames. Long-leading indicators continue to improve as does the nowcast. The short-term forecast has shown a lot of volatility. NDD has laid out criteria for going off “recession watch” setting a good example for everyone.

Much of this week’s news is better interpreted via my proposed framework. For this reason, I will depart this week from calling everything “good” or “bad” and instead putting it in the more nuanced expectations described last week. I’ll do this below in my analysis of the theme for the week ahead.

The Ugly

El Paso. No one thinks that needless deaths are acceptable. No one wants to be afraid when going shopping or sending kids to school. Despite repeated instances of violence like this, the US is making no progress in limiting these risks. I hope I do not (once again) hear the line that if a few “good guy” Walmart shoppers had been armed, this would have had a better outcome.

Part of our polarized society puts single-issue voters with intense interests on one side of an issue and a diffused group of voters on the other side. We get poor policies because our political system is broken. I don’t know the comprehensive answer to this issue, but surely, we can do better than we are.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

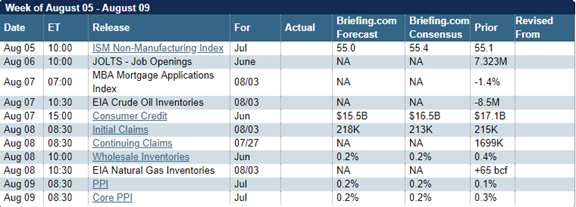

The Calendar

The economic calendar is very light. ISM non-manufacturing is probably the most important. Most use the JOLTs report as a lamer version of Friday’s employment report, instead of for its valuable insight into labor market structure. PPI is the least interesting of the inflation measure, and little change is expected.

This leaves plenty of time for any pundits who are not taking the month off to provide interpretations of last week’s news.

And of course, tweets abound.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

Last week’s jam-packed calendar included more fresh information than we have seen all year. With a light summer calendar next week, and many on vacation, I expect financial media to take up the question of interpreting the fresh news. We can sharpen up the analysis by asking the right question:

Did any of the new information change your mind?

This is a version of a famous quotation usually attributed to John Maynard Keynes, although the original source is in some doubt. Regardless of the source, it is an excellent way to maintain critical thinking and to keep your mind open.

Since we went into the week with a framework, we have a stake in the ground for our own analysis as well as a way of checking on pundit opinion. I suggested a DEFT matrix – Data, Earnings, the Fed, and Trade. I am taking last week’s table and adding what we learned.

|

Hurdle |

Mainstream |

Bearish |

Bullish |

Expert Edge |

|

Data |

Mixed and confusing, as we have seen in recent weeks. |

Widespread weakness, especially in employment and ISM manufacturing |

Stability in employment growth trends. Improvement in manufacturing Continuing high levels of confidence. |

Watch business investment in ISM – a weak spot in GDP. Also consumer outlook on employment, a good check on the regular data. |

Verdict: Bullish case supported. The weakest report was the ISM index of 51.2. They report that this corresponds to GDP of 2.5% (if annualized). Remember that the role of manufacturing in the economy is in a long-term decline, so it is less important than services. The weak spots were inventories, customer inventories, prices, and exports/imports.

Personal income reached a record high. “Davidson” (via Todd Sullivan) writes:

The typical recessionary signs are not present even with many still discussing “Recession’. Previous recessionary periods have been forecasted by slowing Retail Sales and slowing Real Personal Income trends. That trends are continuing nearly guarantees that a recessionary environment is not ahead of us. While trade disputes have slowed global trade with China and its financial system suffering declines, US economic activity remains strong and on trend.

At some point, market psychology will shake off its pessimism and US equity markets to benefit.

Employment growth remains solid but has slowed. Fiscal stimulus from the tax cut did not provide a supply side effect. (Tim Duy).

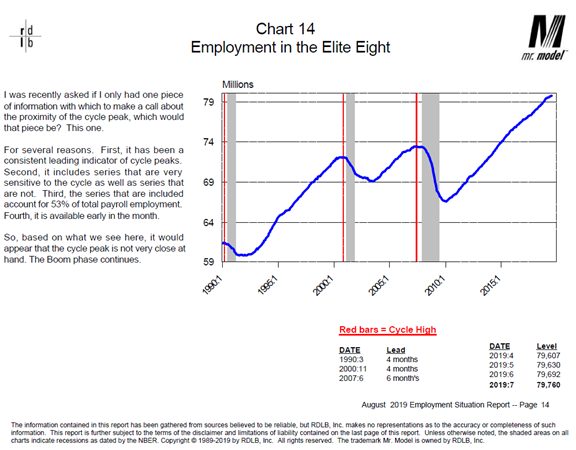

Each month the best employment situation analysis I see comes from Dr. Robert F. Dieli’s No Spin Forecast. This week he has made the entire report available for download as a sample for non-subscribers. I urge you to take advantage of this valuable offer. Each month he looks at both the payroll and household surveys, placing them in context and linking to the state of the business cycle. He carefully refrains from any political commentary in this fact- and-chart packed analysis. This allows him to do plenty of myth busting on topics like part-time employment.

He also skillfully extracts key indicators from the mass of data. Unlike analysts on a mission, Bob is consistent in these choices. When the indicators change, so do his conclusions. Here is an example we will watch with him.

|

Hurdle |

Mainstream |

Bearish |

Bullish |

Expert Edge |

|

Earnings |

Small decline |

Start of earnings recession. |

Enough earnings beats to avoid a quarter of declines. |

Watch changes in forward earnings, the basis for stock pricing. Current results provide a foundation. |

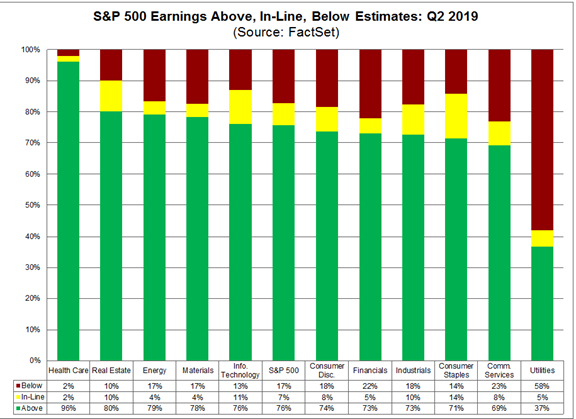

Verdict: Leaning bullish on Q2 reports and bullish on our Expert Edge. John Butters (FactSet) reports that earnings are beating expectations more often and by a larger amount than the five-year average. The sales beat rate (59%) is below the five-year average but the size is above. The blended result for the quarter is on track for a decline of -1.0%, better than last week’s -2.7%. 77% of S&P 500 companies have reported. Brian Gilmartin highlights strong growth in earnings expectations for economically sensitive sectors. Charts for all are below.

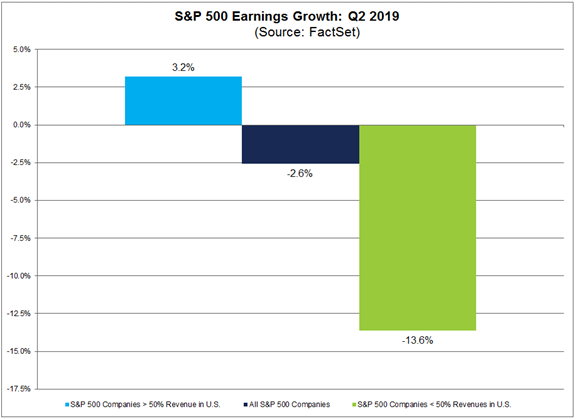

Companies with higher non U.S. sales exposure are doing much worse.

|

Hurdle |

Mainstream |

Bearish |

Bullish |

Expert Edge |

|

FOMC |

25 bps cut |

No cut |

50 bps or strong signal for 25 more |

Any dissents. There is some genuine disagreement. The dot plots. Phrases that suggest dependence on data. |

Verdict: Mainstream, but our Expert Edge showed why some observers were disappointed. The dissents and Chairman Powell’s press conference both showed that this was not a decision for a new easing cycle. During the press conference the market declined two percent based on a few words that suggested “one and done” was the right interpretation. Later in the conference the “data dependent” refrain re-emerged. Since Wall Street types continue to see a weaker economy than the Fed, their inference is that the FOMC will come around with more rate cuts. The Fed futures markets reflected this conclusion.

Tim Duy emphasized the main market complaint – the lack of certainty about future policy. Many of the press conference questions asked, “What should we be watching?” Prof Duy writes:

Powell did leave plenty of clues to guide markets, though the ride won’t likely be smooth. He specifically discussed a variety of factors such as global growth, trade policy, manufacturing activity, job growth and unemployment, inflation, and business confidence and investment. The problem here is that some of these factors are subjective and collectively offer no clear policy path. For instance, Powell said job growth remains sufficient to put downward pressure on unemployment. He also cited faltering business confidence and weak business investment. At the same time, trade tensions have gone from “boiling” to “simmering.”

The President was unhappy with the decision. Some cynical traders believe that his trade threats the next day were an attempt to play on this list of possible concerns.

|

Hurdle |

Mainstream |

Bearish |

Bullish |

Expert Edge |

|

Trade |

“Ceremonial” progress announced |

Another walkaway, with hardline attitudes on Intellectal Property, bleeding into threats. |

Some substantive progress on rules, future agenda, possible compromises. A few specific details. |

Do the US & China announcements match on specifics like agricultural purchases. No threats to specific companies. |

Verdict: Bearish. Without even a symbolic statement, the U.S. reps returned to report no progress. It was not quite a walkaway, but the announced decision for new tariffs on consumer goods was the next worst thing. The Expert Edge showed up again. The announcements about purchases of US agricultural products, made with confidence by Trump after his meeting with Xi, were never confirmed by the Chinese and seem to have disappeared. The threats to specific companies are starting once again.

What I have called the real time lesson in economics gets more legs. Most believe that the new round of tariffs will boost prices for US consumers. Oxford Economics estimatesplace the effect of the announced 10% tariffs at $700 per household. This moves to $900 at the threatened 25% level. The Peterson Institute estimate for the 25% tariff is $1270 per household.

Farmers are already up in arms. Some markets may be permanently lost.

The second-level effects are the uncertainty for business and reduced investment.

Overall Assessment

David Templeton (HORAN) contrasts the improvement of economic and company data with the headwinds from trade issues. In another post, he highlights the continuing contrast between consumer and investor confidence.

Eddy Elfenbein: “What happens from here? I think there’s a good chance that the Fed will cut rates again at its meeting next month. After that, it gets a little murky. It really depends on how well the economy does.”

I’ll add a few more conclusions in today’s Final Thought.

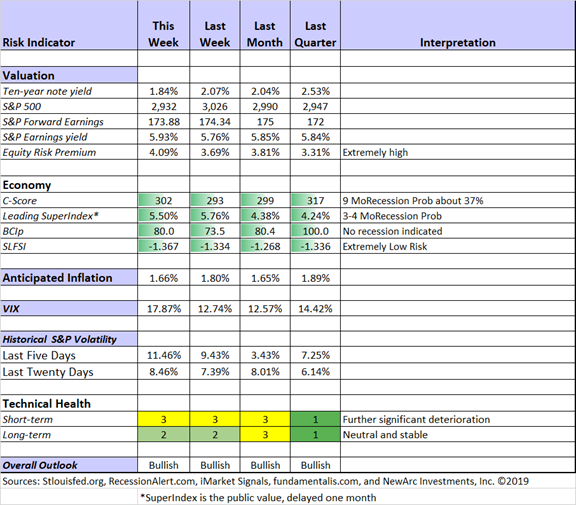

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term technicals weaken but remain neutral. Long-term technical indicators remain mildly bullish. Recession risk is still in the “watchful” area.

Considering all factors, my overall outlook for investors remains bullish.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession, nor does his unemployment indicator.

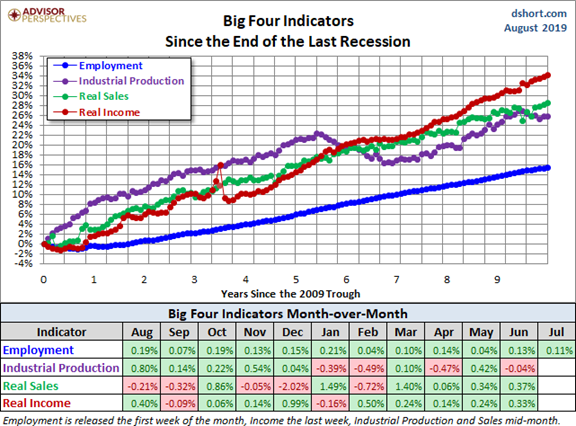

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis. With more major reports, it is time for another look at the Big Four indicatorswatched by the NBER in their recession dating.

Guest Sources

Josh Brown takes up a key issue: “Deceleration.”

He explains that the one-time impact of the tax cuts has distorted the interpretation of economic and earnings effects. His work contrasts recent earnings periods with current expectations for the next few years – lower growth, but solidly positive.

Strong data helps us create more useful indicators. Timothy Taylor takes up an important topic: Administrative Data Moves Toward Center Stage. There is plenty of data collected in the administration of various programs, but it is usually not organized in a way that is useful for analysis. This is changing, so the reliance upon surveys may be reduced. A big challenge in taking this approach is maintaining personal privacy as various sources are linked. This should be carefully considered as these processes are developed.

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I tried to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades are certainly not for everyone.

Stock Exchange has moved to Tuesday publication. As I wrote last week, I am doing this to create more separation between the stocks discussed and our own adjustments. While we warn investors that these are just ideas. They are not intended for readers to follow without research or determining the suitability for their portfolios. We also warn that we may trade out of positions without notice. Even with all of that in mind, a little more separation between publication and trading would be better.

This week’s edition analyzes what should be on your pre-trade checklist. We discuss recent trades from the models and contrast with fundamental analysis. Pulling it all together is our regular series editor, Blue Harbinger.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Ryan Frallich’s How “Resulting” Impacts Your Personal Finances. He begins with some examples of poor decisions that worked out and good ones that didn’t.

All around us people confuse the results of a decision to be completely linked to the decision making process that went in. This is the concept of “resulting”, or drawing a conclusion on the soundness of a decision based on the outcome, rather than whether there was a sound decision making process that gave you the best chance of a favorable outcome. After reading Annie Duke’s “Thinking in Bets”, I see this sort of faulty logic everywhere, particularly in personal finance decisions.

There are many applications for investors, and he has several good examples. Those with mind-game experience like the poker expert Duke, experience this daily. Any time there is an element of chance, a good process can lead to a poor outcome. Learning to develop and remain committed to a sound process may be the most important challenge for investors. You can consider the author’s list of five questions, but it is worth developing your own. I especially like #3. At what point will I change course? “What would have to happen for me to change from this decision down the road?”

Stock Ideas

Chuck Carnevale has another update of his principles for portfolio construction. Curious about how many stocks you need? How to weight them? Chuck describes various choices and analyzes what might work for you.

Utility stocks? Barron’s makes a case underscoring recent outperformance. [Jeff-This idea seems lame and maybe even dangerous, but the article shows the logic of very many investors].

Lyn Alden Schwartzer scooped this week’s Barron’s cover story with her own take on retail stocks. Her data-driven analysis moves beyond the generally known Amazon effects. She looks carefully at valuations via F.A.S.T. Graphs as well as emphasizing returns on capital.

Marc Gerstein analyzes whether Accenture (ACN) is worth a look because of its claimed growth in digital, cloud and security services. Is this management consulting for the 21stCentury?

William Stamm says, Buy Visa: Great Total Return And A Cash Machine. Visa (V) is also an illustration of his “Good Business Portfolio.” These include some very interesting criteria, including the Buffett-like #6. “Would I buy the whole company if I could.”

Personal Finance

Abnormal Returns is the go-to source for anyone serious about the investment business. The Wednesday edition has a special focus on personal finance, with plenty of ideas for the individual investor. I especially recommend Pay Off Debt Or Invest In Stocks: The Leverage Fallacy. The typical thought process of comparing mortgage rates to expected yields may be an inappropriate shortcut.

Watch out for…

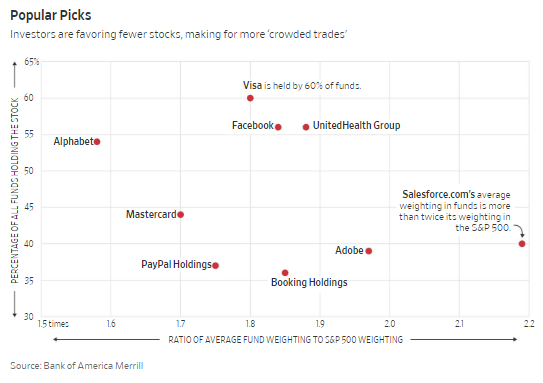

Crowded trades in stocks. With Stocks at Fresh Highs, Investors’ Portfolios Look Alike

Crowded trades in bonds. I like James Picerno’s title, The Bond Market embraces Nirvana.

Economic policy debates aside, there’s no doubt that the bond market’s happy in the extreme. US fixed-income, it’s safe to say, is priced for perfection – and a rate cut or two. Using a pair of measures of the price trend for the funds listed above reminds that the rear-view mirror offers a view of bonds that’s about as good as it gets for the bulls.

Final Thought

The stock market was striding over the hurdles pretty well until the trade tweet. Stocks had regained the highs achieved before the Powell press conference, so let’s not blame the Fed. Economic causation is usually difficult to determine, but this week had a clear sequence of events. There will be plenty of talk about the yield curve and the Fed’s failure to steepen it, but the flattening came after the trade news, not the Fed meeting.

What we are seeing is a repeat of the hot money response spurring a flight to the “safety” of bonds and utility stocks. The concomitant volatility is scary for the average investor. Should it be?

Volatility is not a good measure for risk, especially if you are only worried about the downside. Historical volatility measures the standard deviation of a price series using past data. The VIX represents expected volatility using prices from the options market. Neither shows the kind of risk most of us care about. Options pricing is based upon moves in either direction. That said, the price for this insurance rises when markets decline, particularly in a scary fashion.

When I read a comment that “the VIX should be higher” or “insurance is cheap” it is an opinion that the market price is “wrong.” Such a pundit claims to know better than those trading in the very large and very savvy options market. Investors should consume such advice with great caution, just as they would about overall market direction in assets like stocks, bonds, REITs, or precious metals.

For traders, volatility represents more opportunity – both risk and reward. For investors volatility is a measure of opportunity, not risk. Price gyrations are made to seem scary in financial media but are not predictive of asset price moves. If the trade war gets worse, we will start to see even more pronounced economic effects and impacts on earnings. Those are the facts that would change my mind. Meanwhile the 2.5% growth economy and earnings rebound are still the base case.

Some other items on my radar

I’m more worried about:

- Dollar strength despite the lower interest rates. Currency manipulation as a part of a trade war could have a direct effect on earnings.

- North Korea and Iran. Our style of diplomacy is very different for the two countries, but the results seem similar.

- Brexit brinksmanship.

I’m less worried about

- The yield curve, under the influence of some worldwide effects. When I see confirmation from other economic indicators, I’ll get more worried.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits