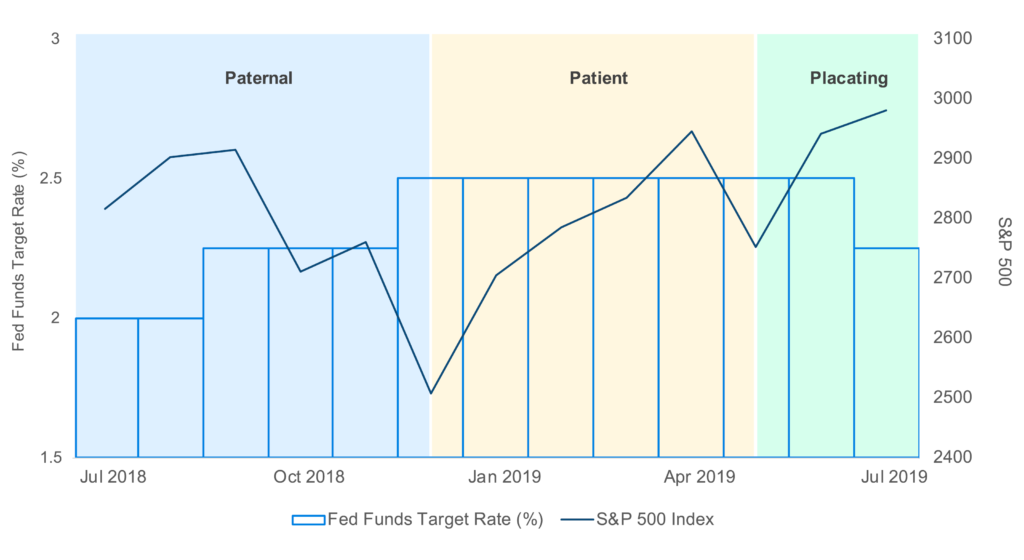

The evolution of a manic market and a fickle Fed

The evolution of the policy stance of Chairman Powell and the Fed over the last nine months has been remarkable, as have the market’s reactions to it. This evolution has been marked by at least three phases that might reasonably be labelled as, parental, patient and placating.

Parental: In early October 2018, in the midst of a succession of rate hikes, Powell noted that rates were still “a long way from neutral,” indicating that more Fed rate increases were warranted and the Fed was committed to staying the course, gradually and responsibly removing the proverbial punchbowl from the party, so to speak. That comment marked the beginning of a 3-month, 19% decline in the S&P 500.

Less than two months later at the end of November, Powell showed the first signs of conceding on rate hikes, hinting that rates were “just below neutral.”

The market seemed to view that response as insufficient and continued to sell off. The Fed increased rates in December.

Patient: In January 2019, the Fed finally relented, indicating it would take a “patient, wait-and-see approach” to further rate hikes, to which the stock market responded positively with a 4-month, 20% rally.

In late May, however, “patient” was no longer adequate and the market began demanding more. Stocks sold off and the yield curve became increasingly inverted.

Placating: At a Fed conference in early June, Powell commented publicly that the Fed would “act as appropriate to sustain the expansion.” Stocks reversed course, logging their best June in more than 60 years, followed by another positive return in July.

After announcing both the first rate cut in more than a decade, and an early end to the balance sheet runoff, Powell commented at his July 31 press conference that this cut did not necessarily mark the beginning of a series of rate cuts. The market was again not satisfied and within an hour stocks were down nearly 2%.

Chairman Powell’s words that the July rate cut won’t turn into an extended series of cuts may prove true, but given his recent track record and the market’s response to his comment, it isn’t unreasonable for investors to suspect otherwise. The market’s appetite for more accommodation seems insatiable, and to date, Chairman Powell and the Fed have exhibited a willingness to give it.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.