Weighing the Week Ahead: Get Out, Hide Out, or Ride It Out?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is normal, featuring housing starts, retail sales, and Michigan sentiment. The CPI will be important someday, but only when it breaks the recent path of gentle increases. With summer vacations in full swing (even Congress is on a five-week recess) the punditry turns to tried and true topics – the spike in volatility, mistakes by the Fed, how near is the next recession, and how the bull market will end. Whatever the subject, the answer is often a call to action. Expect the pundits to be looking at the week behind to find material for the week ahead, asking:

Should you get out, hide out, or ride it out?

Last Week Recap

In last week’s installment of WTWA, I summarized what we learned from an especially jam-packed week of news, and then asked whether the facts changed your mind? That was a good question, but for most the answer was a firm “no.” People have the motivation and ability to use facts to confirm their existing biases.

I also warned individual investors about using volatility as a risk measure. Monday’s trading and the result for the week provided a perfect example of why this is a mistake.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, which combines a lot of information in one picture. The full article also includes several other interesting takes on price movement.

The market lost 0.4% for the week, but this tame result misses the big story. The trading range was 4.1% including 2.7% in a single day. My weekly Quant Corner translates this into a volatility calculation which you can compare both to VIX and to past readings.

Noteworthy

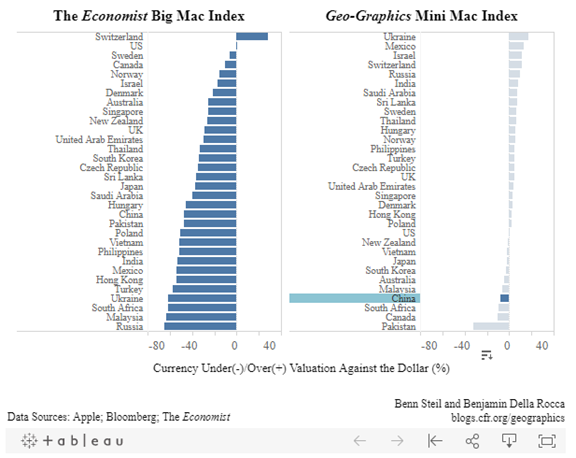

The Council on Foreign Relations has responded to The Economist’s “Big Mac” indicator, which uses prices around the world to see which currencies are over-valued. If the market is efficient, the prices should be the same. As they note, however, Big Macs do not “travel well.” They suggest the “Mini Mac” index as an alternative. This index compares the price of iPad minis across countries. Read the full post for some amusing comparisons, which might actually make sense.

As shown in the graphic at the top, the Mini Mac Index suggests that the law of one price holds far better than does the Big Mac Index. The Big Mac shows the dollar overvalued against most currencies, by an average of 35 percent (a whopper). By contrast, the Mini Mac shows the dollar slightly undervalued—two percent on average (small fries).

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. He reports that long-term indicators are now even more positive while short-term indicators, highly volatile of late, remain slightly negative. The biggest positive he sees is the new low in corporate bond yields:

It can hardly be overstated how positive it’s that corporate bonds have made a new low. On the cusp of a recession, corporate bonds get riskier, and their yield rises. They don’t make new lows. This indicator has a 100-year history with only three false positives, one of which was the 1945 WW2 demobilization, and one of which was the 1938 fiscal tightening. Also, the lack of inflation gives the Fed wide latitude to cut rates.

Part of the NDD list of high frequency indicators is the money supply. Stable growth is a good sign of activity in borrowing and bank lending. Here is a look at recent growth, rebounding from the two-year decline but still modest.

The Good

- Initial jobless claims declined to 209K. This was lower than the prior week’s 217K and expectations of 213K.

- PPI increased the expected 0.2% but declined 0.1% on the core. This is significantly lower than last month’s 0.3% increase or the expected 0.2%. I score this as good news because it means there is little pressure for rate increases. Some emphasize that it is missing the Fed’s target of 2% increases, but there are better gauges of economic growth.

-

Earnings expectations remain strong. It is normal for estimates to decline between 1.2% (last five years) and 1.8% (last fifteen years). The current 1.6% decline is nothing special. (John Butters, FactSet).

Brian Gilmartin describes the increase in expectations for 2020, providing a sector focus. The increase in industrials, energy, and basic materials suggest that the analyst community, at least for now, sees stronger global growth. [Jeff – The added value I see from analyst estimates comes mostly from their close analysis of the stocks they follow. I think of them as experts reviewing what the company is saying. I do not expect analysts to make macroeconomic forecasts, and their work is less helpful when they do]. - The JOLTs report shows continuing labor market strength with some tightening. Most news reports emphasize the number of job openings rather than the most important aspects of the data. Taken from the BLS site, here are two of the key points.

Unemployed persons per job opening is steady and remains below 1.

The quit rate, a measure of employee confidence in finding another job, remains stable at record levels.

- Home prices increased 3.4% year-over-year in June. Calculated Risk reports the CoreLogic index for June.

- Mortgage applications are increasing in what the WSJ calls “a frenzy.” Applications were up 5.3% versus a decline of 1.4% in the prior week.

The Bad

-

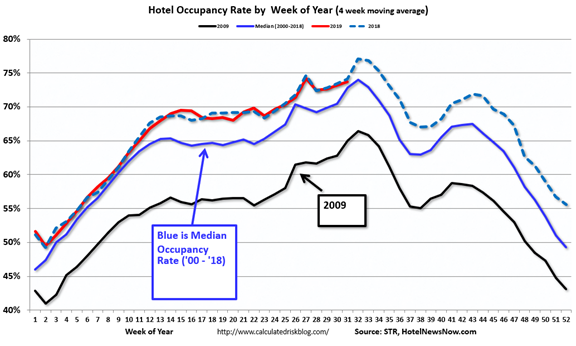

Hotel occupancy decreased 0.8% on a year-over-year basis. Calculated Risk notes that current levels are still near last year’s highs as we enter a seasonally strong period.

-

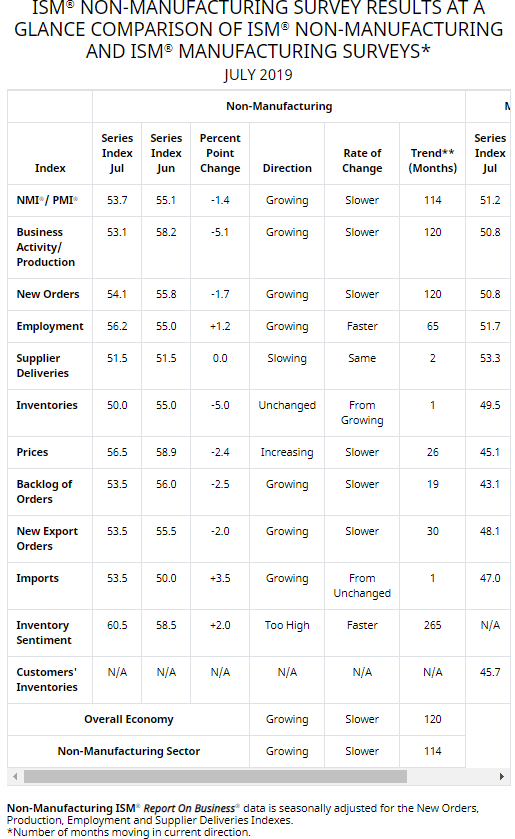

ISM Non-Manufacturing registered 53.7, lower than expectations of 55.4 and last month’s 55.1. The ISM reports that based upon past relationships and annualized, this implies a 1.8% increase in GDP. Here is their helpful table of subcomponents. The full report provides additional detail on each.

-

Light vehicle sales in July decreased to a SAAR of 16.8 million, down 1.8% from June and slightly worse than last year at this time. Calculated Risk sees sideways movement at these near-record levels, but notes, “This means the economic boost from increasing auto sales is over.”

-

The U.S./China trade war worsened. Trump’s frustration with China boils over, reports POLITICO. China responded by allowing the Yuan to devalue. This is a sign of a weakening economy as well as a discouraging message about the negotiations. (WSJ).

The Ugly

Threats to the food supply. (NYT).

The world’s land and water resources are being exploited at “unprecedented rates,” a new United Nations report warns, which combined with climate change is putting dire pressure on the ability of humanity to feed itself.

The report, prepared by more than 100 experts from 52 countries and released in summary form in Geneva on Thursday, found that the window to address the threat is closing rapidly. A half-billion people already live in places turning into desert, and soil is being lost between 10 and 100 times faster than it is forming, according to the report.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

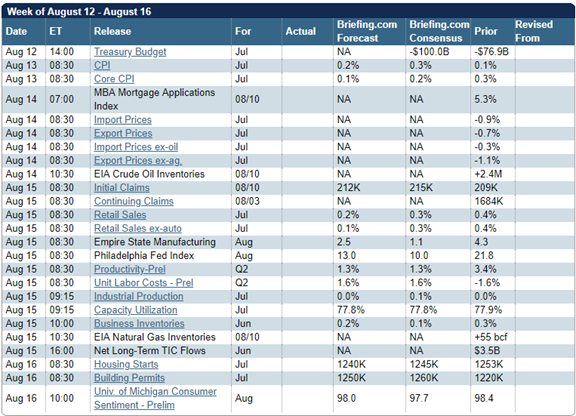

The economic calendar is normal. The most important reports are retail sales (expected to decelerate), industrial production, and housing starts. I am also interested in Michigan sentiment. The CPI will make news only if a big change from the recent modest increase.

Small business optimism from the NFIB does not get preliminary estimates, but it has gained more attention in the Trump era. There are still some important earnings reports.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

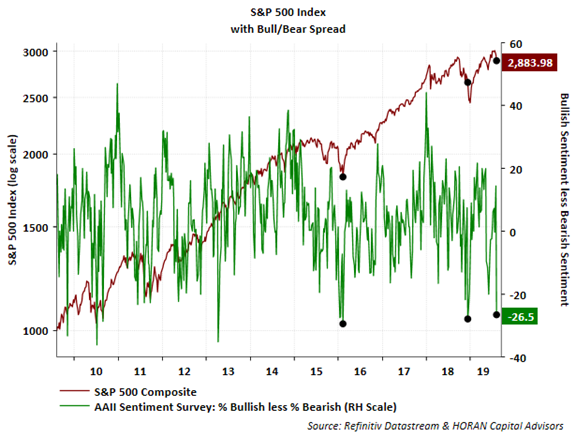

While this is a normal week for economic reports, there seems to be little attention paid to them lately. The slow days of summer invite the punditry to search for excitement, wherever it might be. Are times any more threatening than they were a year ago? Regardless of your answer, the news and daily market gyrations have gotten the attention of average investors. David Templeton (HORAN) describes the extreme reaction. Bullish sentiment is now at the lowest point since the recession scare in December 2018. He notes that these extreme levels have corresponded to buying opportunities in the last ten years.

How can this be? Most investors are inexperienced and reactive. They are unable to determine which news events are important and when to ignore volatility. The field is open for the pundits, who will be asking:

Should you get out, hide out, or ride it out?

Background

Why is it so challenging to interpret the news? The arcane topics require deep analysis. The news versions tend to be slogans, tweets, and one-liners. I cannot write about each of these topics as part of WTWA, but I’ll take them up in more detail if there is interest. For those who want more background for their own thinking (probably most of my readers), I am providing links for several key topics.

- Dollar strength? Traditionally this has been a key economic goal. President Trump has been on both sides of this topic and made the unusual move of placing responsibility on the Fed. In an accurate and accessible explanation of the key issues, Michael Klein and Maurice Obstfeld ask, Should the United States Try to Weaken the Dollar?

- Trade war beneficiaries?

Clay Chandler and Naomi Elegant, writing in Fortune’s excellent CEO Daily column explain how China and the U.S. are both big losers. James Picerno worries that this is a high-stakes gamble relying on the President’s own intuition and analysis, not the advice of aides. He is also concerned that it might be getting out of control.

-

Chinese currency manipulation? Timothy Taylor’s clear explanation provides context and a deeper look.

And also recent history with notes from The Daily Shot.

The Choices

Get out! This advice is so pervasive (and long-running) that no single link does it justice. You can find plenty of choices from my Twitter account lists (@dashofinsight) under “reliably bearish comments.”

Hide out. Barron’s is happy to offer suggestions. If this is your choice, pick up the current issue.

Ride it out. This is the advice of most professional investment advisors. Many sent calming messages to clients on Tuesday warning that volatility was not risk. (Maybe they read my column from last Sunday. Advice is always more important before an event happens, which is why I call this WTWA). One firm suggested that if your personal needs haven’t changed, neither should your portfolio. That is basically correct, but I’ll add my own conclusions in today’s Final Thought.

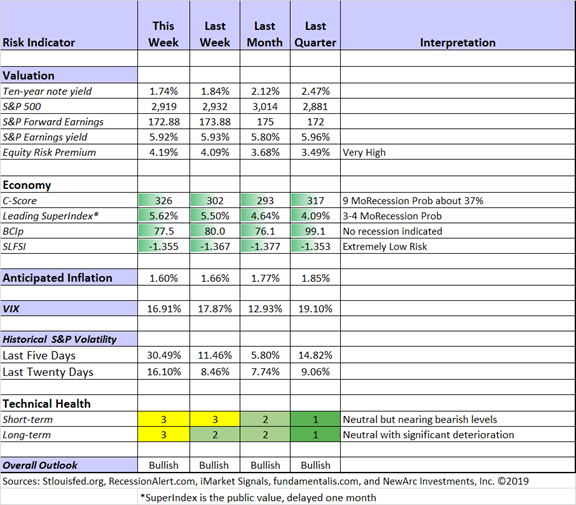

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term technicals remain neutral but are trending worse. Long-term technicals deteriorated to neutral. Recession risk is still in the “watchful” area despite the increase in the C-Score.

Considering all factors, my overall outlook for investors remains bullish.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Guest Sources

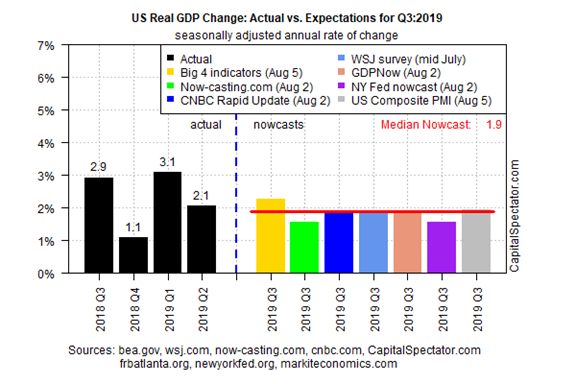

James Picerno reports the early Q3 GDP estimates, an extension of Q2’s modest growth.

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I try to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades described are certainly not suitable for everyone.

This week’s edition describes how fear can lead to trading mistakes. We begin with some expert advice from Dr. Brett Steenbarger and then share some recent picks from the trading models. Pulling it all together and providing counterpoint drawn from fundamental analysis is our regular series editor, Blue Harbinger.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Alan Steel’s description of wisdom gained over fifty years, including 46 in the business. The entire post is so helpful and entertaining that I am having trouble finding the right quotation to summarize. After recounting the decades of economic commentators obsessed with problems. He provides several key examples before observing as follows:

But the truth is most the time the index is “below water”. Since 1969 the facts are that 16% of the time the stock market is in a drawdown of between 5% and 10%. A further 20% of the time it’s in drawdown of 10% to 20%. And a remarkable 27% of the time it’s in drawdown of more than 20%. No wonder investors who insist on looking at their portfolios every day end up as gibbering basket cases.

He also cites some commentary from Charlie Munger, asked about Berkshire Hathaway’s current underperformance.

He replied that they just kept doing what they always did. Buy great businesses as cheaply as they could and kept them as long as they could. Over time their share price fell by at least 50%, and six times they underperformed the main index by at least 30%. Sometimes the inmates run the asylum. But reversion to sense eventually happens.

There is more of course, written in Alan’s engaging style.

Stock Ideas

Chuck Carnevale revisits his past work on Microsoft (MSFT). He “sold too soon” according to market prices, leading him to make a careful explanation of valuation and the importance of choosing the right time frame. He has another great post describing The Worst Reasons To Sell A Stock. This includes a great example as well as the lesson we expect.

Want REITs? Double Dividend stocks suggest some closed-end funds that are a bit different. They also suggest Procter & Gamble (PG).

Small cap value stocks? The best long-term returns and now very cheap. Larry Swedroe explains that this happens when investing in any risk asset class. Small cap value stocks have underperformed for ten years. He looks at large-cap history and points out, “The three long periods when the equity risk premium was negative (i.e., bonds outperformed stocks) also demonstrates that even 10 years of underperformance of a risky asset class is likely nothing but noise. They also explain why investors demand a large equity risk premium!”

Ploutos suggests a small cap ETF that might fit the bill.

D.M. Martins Research still likes Azul (AZUL). They take a deep look at this Brazilian airline.

Stone Fox Capital advises on the Celgene merger with Bristol-Myers, explaining how to handle the non-stock portion of the deal. The post covers the important considerations. [Jeff – we already sold our position and moved on. The upside is limited compared to other opportunities we saw].

Personal Finance

Abnormal Returns is the go-to source for anyone serious about the investment business. The Wednesday edition has a special focus on personal finance, with plenty of ideas for the individual investor. As always there are many good links. Since I can’t pick a favorite, I’ll suggest these two.

- 4 Financial Worries to Cross Off Your List, by Christine Benz. Check out the extremely unlikely problems.

- 3 Signs Your Finances Aren’t Ready for Retirement from Pete the Planner. [Jeff – these are good ideas, but not the only ones. See today’s Final Thought].

Watch out for…

Chinese corporate data. The Wall Street Journal reports on issues with auditors violating securities commission rules.

Duke Energy. Generously Valued and Burdened by Debt reports Valuentum.

Bogus causal inferences. So many Economic variables move in apparent unison that it is easy to assert misleading relationships. This is important because understanding is the foundation of good decisions. My recent brief introduction to causal inferences includes some examples from last week. Beware! You must be willing to learn something.

Bitcoin as an inflation hedge. Nick Maggiulli relates his own Bitcoin experience. He then offers good advice about price versus value, and future purchasing power.

Final Thought

The right asset allocation is a very personal choice. It depends upon your circumstances, aspirations, and volatility tolerance (a better term than risk tolerance). Keeping this in mind, here are some observations on each of the three.

Getting Out

It is rarely wise to go “all in” or “all out.” The record of market timing is not good. You need to make a timely exit and a timely re-entry. If the President tweeted about a friendly exchange with Xi and the market spiked, would you re-enter? Wait for a dip? What if it kept going? Would you know how to interpret the news?

This choice might be correct for those who are in full wealth preservation mode. Always have enough in safe assets so that your lifestyle is not at risk.

Hide Out

I hate this alternative. Most of the suggestions for hiding out are already crowded trades, providing a different set of dangers. If you are troubled by world events and volatility in markets it is a sign that you should do one of two things:

- Turn off your news! Don’t look at your account balances all the time.

- If you cannot follow #1, then you need to reallocate your asset distribution. Life is too short to waste your time on worries. The recent market action was minor. The worries are different, but not worse than those of the past. If you are troubled by what it meant for your retirement account, you need a portfolio review.

Ride it Out

This advice, assuming your personal needs have not changed, is the best of the three choices. That is why it is so popular with the big institutional investment managers. As with the “hide out” alternative, you need to address the psychology of market volatility. Those frightened out of sound investment positions because of market variations are making the worst choice. Get perceived risk within your personal limits.

You can also watch for the actual risks using our Indicator Snapshot.

Hedging

I did not include this in the main theme, because it is very dangerous for the average investor. The SEC has (unwisely in my opinion) made it easy for individual investors to choose exotic products that seem clever. Some people with strong opinions about market direction want to “invest” in leveraged inverse ETFs. If your holding period is more than a few days, this is a terrible idea. The compounding and tracking errors are so great that you can suffer substantial losses even when you are right about the market direction.

The Real Danger Signs

Most would be surprised that a personal portfolio that has beaten the market in recent years may be a sign of danger. I see many of these. They are generally chock-full of FAANG stocks, tech-laden ETFs, utilities, and bond funds. If you have done well with a portfolio like this, take a victory lap, pat yourself on the back, and think about reallocating into under-valued stocks.

Taking these steps is easier if you have some experience. Dr. Brett Steenbarger explains this in a post that is just as relevant for investors as it is for traders. He points out that professionals learn from experience. There is no substitute for practice and analysis. Few investors have this experience. Most make decisions based upon recent performance of stocks, funds, and managers. Since we know that the last decade has embraced a near-record bull market and attractive interest rates, it is not very typical – a poor test period for our decisions.

Many (most?) investment professionals have never seen a real bear market or a crash. This leaves them constantly on watch for something they cannot really recognize.

Some other items on my radar

I’m more worried about:

- Hong Kong confrontations. The Economist describes the escalation of the protests and the dangers of China sending in the army. China claims the U.S. is involved. (WSJ)

- Trade war escalation into actions against individual companies. Most of the trade war effects are reflected in the lower worldwide growth estimates, but direct attacks on companies is not.

I’m less worried about

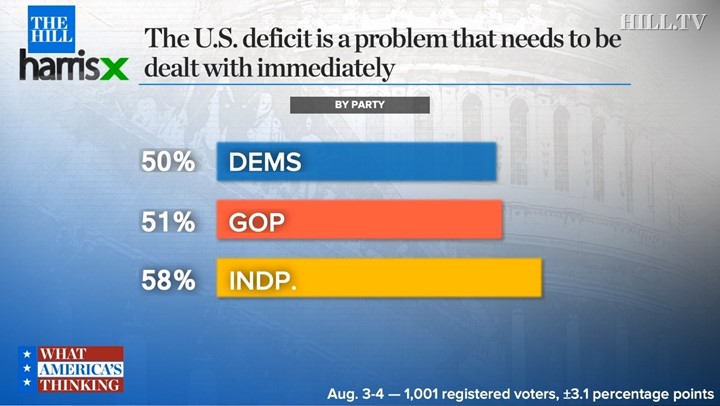

- The debt ceiling increase. I have written that the debt ceiling is a poor way to control spending and investors should be glad to see a deal. I have also written that it is the typical expansion of spending to go along with last year’s tax cuts. Most people, regardless of party, think that this should be a priority. Good luck with that. (The Hill)

- The yield curve. It is reacting indirectly to trade issues and European bonds, providing a somewhat skewed picture. It is worth watching (as I am), while keeping the context in mind.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits