Progress Report on SOFR

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMore than halfway through LIBOR’s planned transition, SOFR’s adoption has lagged

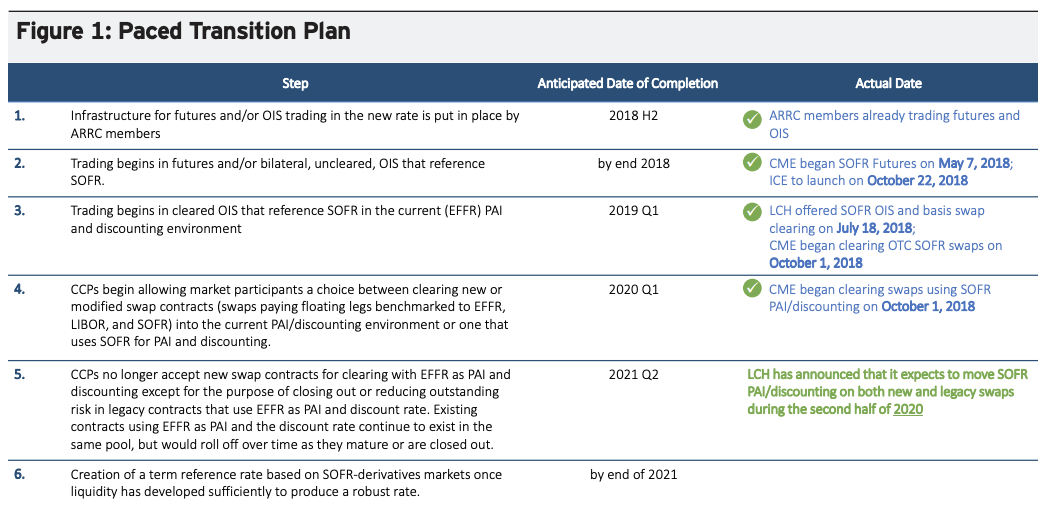

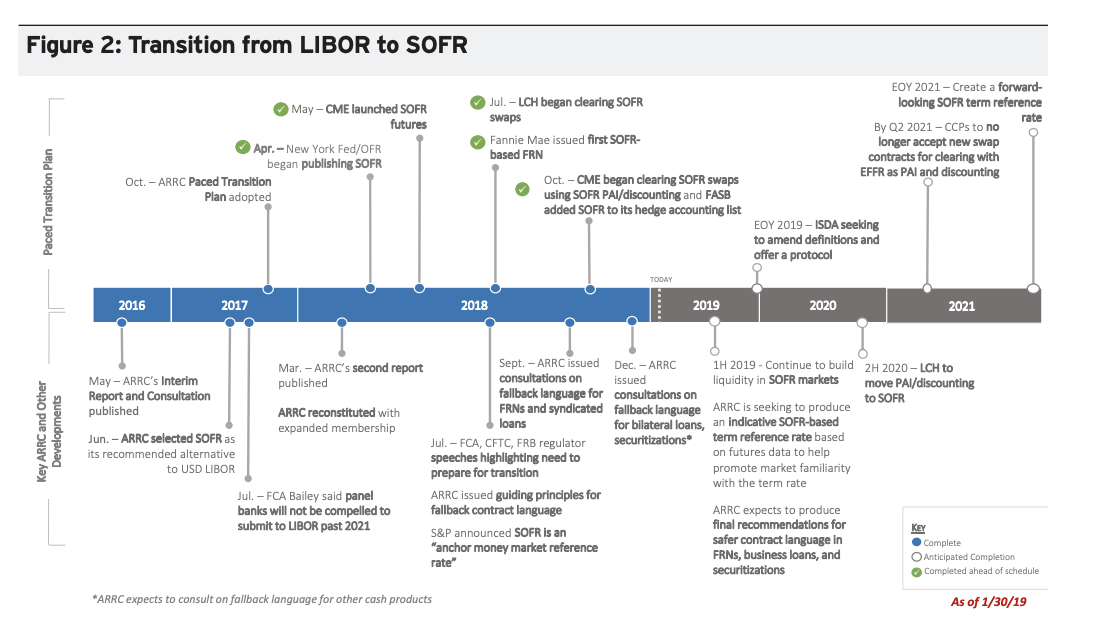

It has been a year since the Federal Reserve Bank of New York launched the Secured Overnight Financing Rate (SOFR) to replace the London Interbank Offered Rate (LIBOR) by the end of 2021. A formal transition plan developed by the Alternative Reference Rate Committee (ARRC) has laid out a timely transition to SOFR with specifics on steps to encourage SOFR’s adoption (Figure 1). The ARRC’s plan aims to promote the use of SOFR-based financial instruments and the development of a forward-looking SOFR term structure to boost the new rate’s usage and market liquidity.

Source: ARRC, Transition from LIBOR, https://www.newyorkfed.org/arrc/sofr-transition, May 2019. OIS is overnight index swap; EFFR is effective federal funds rates; PAI is price alignment interest; CME is a leading derivatives marketplace’ ICE is the Intercontinental Exchange; PAI is price alignment interest; LCH is a leading global clearing house; and CCP is Central counterparty clearing house; H2 is second half; Q1 is first quarter.

But while the market mechanics of the transition have generally followed the Plan’s timeline, the actual adoption of SOFR in terms of transaction volumes remains in its infancy. We believe the delay in SOFR’s adoption can be linked to several factors:

• Delayed development of a term SOFR market

• Delayed development of SOFR-linked derivative products

• Low SOFR-based issuance by corporate and municipal entities

• Slow migration of bank asset and liability hedging to SOFR-based securities

• Uncertainty over the transition of existing LIBOR-based contracts

• Lack of operational readiness of financial institutions to transact in SOFR

Recap – Why is LIBOR being phased out and SOFR phased in?

LIBOR is a short-term interest rate indicating average rates at which banks can obtain wholesale, unsecured funding for certain periods. This benchmark rate became the subject of several well-publicized scandals involving its manipulation when some banks misrepresented their borrowing rates in an attempt to dispel concerns that they were facing funding challenges in the midst of the global financial crisis. UK regulators subsequently made several changes to impose greater oversight of LIBOR, seeking to restore confidence to a reference rate that has been woven into the financial fabric of the financial industry for decades and that underlies a myriad of loans and securities from auto, commercial and residential mortgage loans to interest rate derivatives. But arguably the biggest challenge LIBOR has faced has been the decline in unsecured interbank lending since the global financial crisis. Dodd-Frank banking regulations sought to reduce systemic risk in the US financial system by dramatically reducing the lending exposure that banks have to other banks. This was achieved through onerous capital and liquidity requirements that made interbank lending uneconomical. As a result, average daily interbank lending volume in the US dollar is now extremely thin, leading financial regulators and market participants to reevaluate LIBOR as a representative market rate. The Financial Conduct Authority (FCA), the UK regulator charged with the oversight of LIBOR, has stated it will not compel rate-submitting banks to provide submissions to the Intercontinental Exchange (ICE), the oversight panel in charge of the calculation of LIBOR, beyond 2021. In 2014, concerns over LIBOR’s viability as a benchmark prompted the US Federal Reserve (Fed) to form the ARRC, charging it with the selection of a new benchmark to replace LIBOR. After three years of study, the ARRC recommended the adoption of SOFR, a rate based on three types of overnight repurchase (repo) transactions: tri-party repo, general collateral financing (GCF) repo and bilateral Treasury repo. SOFR is considered one of the most robust indices available since it is based on a high volume (approximately USD850 billion) of daily overnight transactions.2 In addition, it provides market participants with greater transparency into the US Treasury repo market, a vital segment of the US financial system.

Source: Federal Reserve Bank of New York, Jan. 30, 2019. https://www.newyorkfed.org/medialibrary/microsites/ arrc/files/libor-timeline.pdf. FASB is Financial Accounting Standards Board; CFTC is Commodity Futures Trading Commission; FRB is Federal Reserve Board; FRN is floating rate notes; ISDA is International Swaps and Derivatives Association. For Illustrative purposes only.

How has SOFR been received?

The integration of SOFR into broader markets has been slow. Although, the issuance of SOFR-linked floating rate notes continues to grow, it remains relatively limited and issuance by corporate and municipal entities has been especially light. These issuers appear inclined to see the SOFR-linked market develop further, allowing them to gain greater understanding of the pricing of SOFR-linked products. In addition, potential issuers are likely awaiting greater clarity on the following developments:

• Development of SOFR term structure - Market participants are awaiting the creation of an “indicative term structure,” important in the development and issuance of SOFR-based securities. A highly liquid and robust derivatives market is necessary for the build-out of term SOFR rates, in our view.

• LIBOR “fallback language” - LIBOR fallback language identifies benchmark interest rates that would replace LIBOR in LIBOR-based loans in the event of LIBOR’s discontinuation.

• Swap market liquidity - The volume of SOFR swaps transactions remains relatively light, although we anticipate a gradual increase as banks adopt SOFR for hedging purposes.

• Operational readiness - Many market participants are not yet operationally ready to transact in SOFR, hindering its adoption.

Some investors have also challenged the notion that SOFR - a nearly risk-free, secured rate - can successfully replace LIBOR - an unsecured rate with a credit component. A significant design drawback of SOFR versus LIBOR is that it fails to capture the disparity in counterparty risk reflected in funding costs associated with different issuers, which has been an important measure for investors. In January, the ICE Benchmark Administration (IBA) published a white paper discussing the creation of an index similar to LIBOR in terms of its credit component, referred to as the US Dollar ICE Bank Yield Index (BYI), “designed to measure the yields at which investors are willing to invest US dollar funds in large internationally active banks on a wholesale, unsecured basis over one-month, three-month and six-month periods.”3 This index is based entirely on primary and secondary market transactions in certificates of deposit , bank commercial paper and unsecured deposits. Unfortunately, like the LIBOR index, the proposed BYI has some potential drawbacks, namely low transaction volume and the potential inability to generate sufficient data to be a reliable, robust index. Hence, the BYI may lack the necessary support from financial regulators to gain market traction. Nevertheless, this is a development that merits attention, with daily publication of the rate scheduled to begin in the first quarter of 2020.

Supply and demand for SOFR-linked instruments is interrelated

Demand for SOFR-linked floating rate notes currently outpaces supply. To correct this imbalance, greater issuance, or supply, of SOFR-linked securities is needed. Typically, new markets are led by their least risky segments, for example, government-related securities. Indeed, the US Federal Home Loan Bank (FHLB) is currently the largest issuer of floating rate securities benchmarked to SOFR. The FHLB lends to domestic US banks to promote mortgage lending and funds these loans, called “advances,” in US financial markets. But a few factors are holding back the extension of FHLB advances based on SOFR. Banks have been resistant to take on SOFR-based loans due to a lack of operational readiness and computational problems with SOFR-based coupons. This hesitation has simultaneously held back the issuance of SOFR-linked securities to fund these advances, a significant hurdle in the overall development of the SOFR-based market.

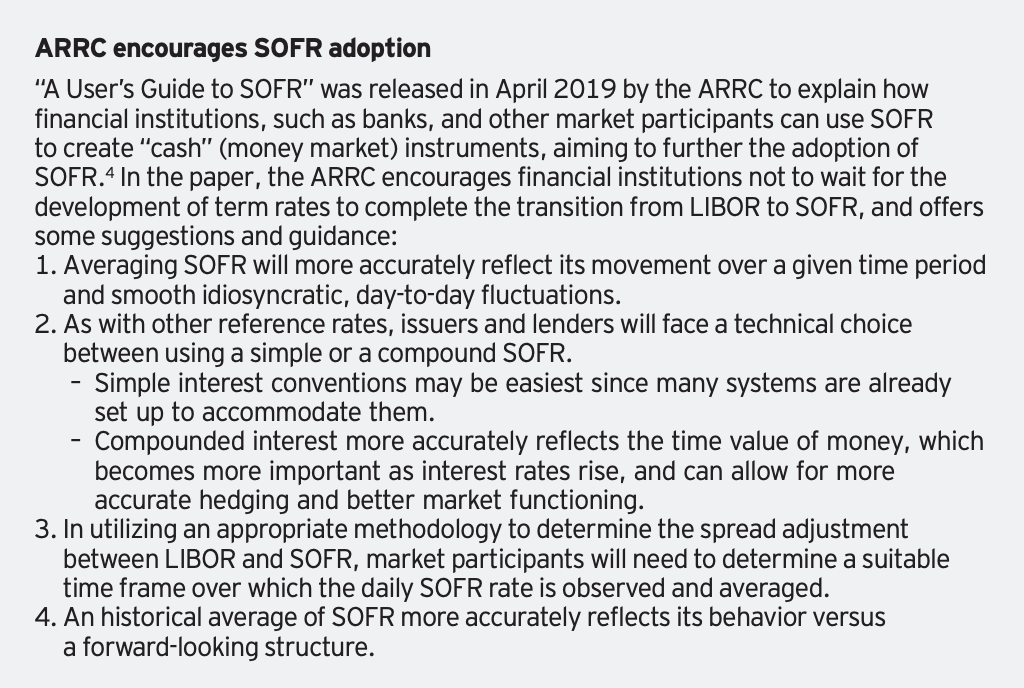

Another challenge facing SOFR is its lack of term interest rates. The development of term SOFR rates is critical to its success, in our view, but is dependent on the generation of significant volumes of SOFR futures and overnight indexed swap (OIS) contracts-i.e. a market for SOFR-based derivatives. In an April 2019 white paper, the “User’s guide to SOFR,” the ARRC encouraged market participants not to wait for the creation of term SOFR rates to make the transition from LIBOR.

The derivatives market, on the other hand—which is often used to hedge certain money market assets and liabilities – is in turn “waiting” for the development of SOFR-based money market instruments for use in the creation of hedges. The interdependency of the money and derivatives markets presents us with a dilemma: Which SOFR-based market will develop first to enable the calculation of term SOFR rates? Until the volume of SOFR-denominated assets and liabilities increases, demand for SOFR-based derivative products will likely also remain low. Ultimately, we believe these markets will need to grow and evolve in tandem for the SOFR index to succeed.

How will this (chicken and egg) situation likely be resolved?

We believe the markets for SOFR-based securities and SOFR-based derivatives will develop together, leading to the ultimate success of the benchmark. But we believe regulatory action will be necessary to promote the transition of LIBOR-based derivative instruments to SOFR. Such changes will likely boost volumes in SOFR-based futures and OIS trading as the use of SOFR-based derivatives grows.

The issue of pricing

The market is also working through the “spread adjustment” necessary for the conversion from LIBOR to SOFR, in other words the differential spread required to equate the interest rates on LIBOR and SOFR-based instruments. Market strategists have cited the work of the International Swaps and Derivatives Association (ISDA) on converting benchmark risk-free rates to their Interbank Offered Rate (IBOR) equivalents as a framework for calculating the spread adjustment in moving from LIBOR to SOFR. ISDA’s proposal focuses on utilizing the historical average spread between the term risk-free rate and IBOR to account for the differences in credit quality and liquidity between the two rates.

ISDA has proposed three spread adjustment methodologies:

• Forward approach -Based on the forward spread between the relevant IBOR and risk-free rate.5

• Historical mean/median approach - Based on the mean or median spot spread between the relevant IBOR and risk-free rate calculated over a significant, historical period (e.g. five or 10 years).6

• Spot-spread approach - Based on the spot spread between the relevant IBOR and riskfree rate on the day preceding the announcement or publication of the event triggering the conversion.

Based on ISDA’s research, we believe the historical mean/median approach to the spread adjustment is the most suitable method. We believe a lookback period of five years would provide sufficient historical data to calculate a spread adjustment between LIBOR and SOFR. In ISDA’s study, proponents of this method highlighted its advantages as being robust and simple, reducing the potential for manipulation, and its resistance to market distortions.

The final decision on the preferred LIBOR-SOFR conversion methodology is still a work in progress, especially given the changing dynamics over the past few years in the secured and unsecured fixed income markets, driven mainly by money market reform and changes in monetary policy. These changes may complicate the mean/median methodology, for example, since these major market events have arguably impacted interest rate performance.

Because the adoption of SOFR has been slower than anticipated, these guidelines appear intended to respond to concerns that market participants have had regarding the transition to SOFR. We believe these concerns have hindered SOFR’s adoption and will likely need to be further addressed and resolved before greater progress can be made in SOFR’s broad integration into markets.

The issue of existing contracts beyond 2021

The transition process away from LIBOR remains challenging due partly to the number of outstanding LIBOR-based contracts that extend beyond 2021. Many contracts for products referencing LIBOR do not adequately account for the possibility that LIBOR may no longer be viable.7 We believe the market needs clear guidance and transparency in the transition process, including fallback contract language for syndicated loans, bilateral loans, floating rate notes and securitizations to ensure that these contracts will continue to be meaningful.8

ISDA has proposed three steps for the transition: 1. Official announcement that LIBOR will no longer be published after a specific date. 2. LIBOR publication ceases and contract fallback rates (Figure 3) are triggered. 3. A one-year transition period after LIBOR replacements have been triggered. We believe this recommended protocol for the transition to SOFR would minimize market disruption, provide a suitable timeframe to facilitate the transition and accelerate the adoption of the new SOFR benchmark.

Source: ISDA, July 12, 2018.

Progress report on SOFR’s adoption by market

The adoption to SOFR is slowly taking place in various markets – most of which have been traditionally tied to LIBOR. Below is an accounting of some recent developments in the transition to SOFR.

US agency floating rate notes

There appears to be robust demand for SOFR-linked floating rate securities, demonstrated by the oversubscription of new issue offerings of SOFR-based US agency floaters. In a few recent US agency floating rate deals, the bonds traded higher compared to initial price indications due to strong interest in the deals. Since July 2018, floating rate notes benchmarked to SOFR have grown to over USD94 billion outstanding, driven primarily by Government Sponsored Enterprises (GSEs) which have issued more than USD84 billion over this time frame.9 The Federal Home Loan Bank (FHLB), has been responsible for 55% of total GSE issuance. 10

Potential US treasury security linked to SOFR

The US Treasury is considering the issuance of a Treasury security indexed to SOFR. This would likely provide a significant boost to the ARRC’s efforts to transition the market from LIBOR to SOFR, but we believe we are more than a year away from the Treasury’s adoption of the SOFR benchmark, as it studies the pricing of such a security.

Bank hedging activity

The Financial Accounting Standards Board (FASB) quickly adopted SOFR as an eligible benchmark for bank hedge accounting. FASB’s push for the adoption of SOFR is part of a broader effort on the part of regulators to encourage the transition from LIBOR to SOFR.

Swaps and derivatives

Activity in SOFR-based swaps and derivatives has picked up. The notional volume of SOFRbased interest rate and basis swaps totaled USD16.8 billion at the end of April 2019, marking a significant increase compared to USD6.9 billion at the end of January.11

The improvement in price discovery, especially in longer tenors, has generated greater interest in this segment of the market. We believe increased volume in the swaps and derivatives markets will help advance the use of SOFR in financial institutions’ hedging activity, aiding in the overall development of the SOFR term market.

The outlook for SOFR: Q&A with Invesco Global Liquidity

Q: What would demonstrate that SOFR adoption is gathering steam? We are looking for increased volumes of SOFR-based derivatives, interest rate and basis swaps and issuance by corporate and municipal entities. We are also focused on the treatment of existing LIBOR-based contracts that will be transitioned to SOFR and are waiting for SOFR to become the standard reference rate for newly issued floating rate securities.

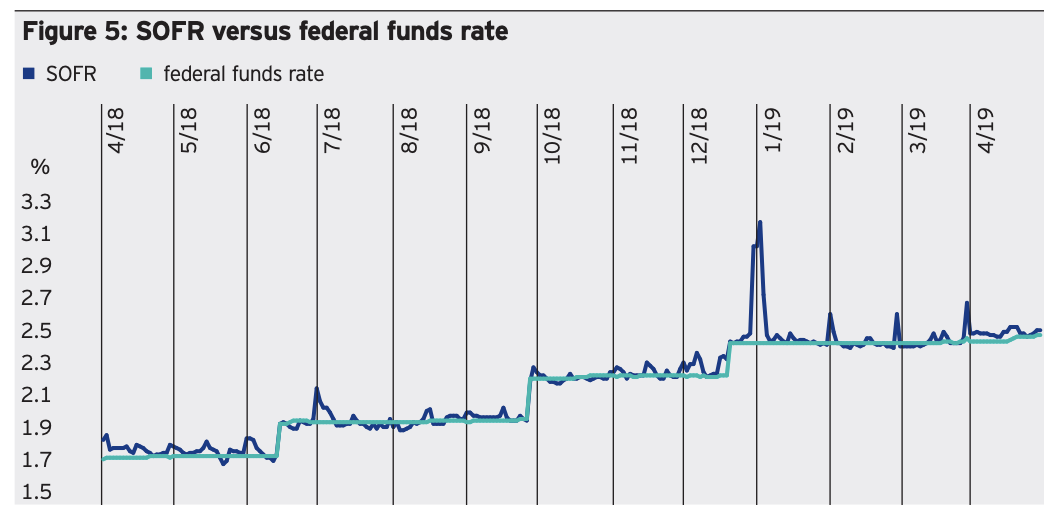

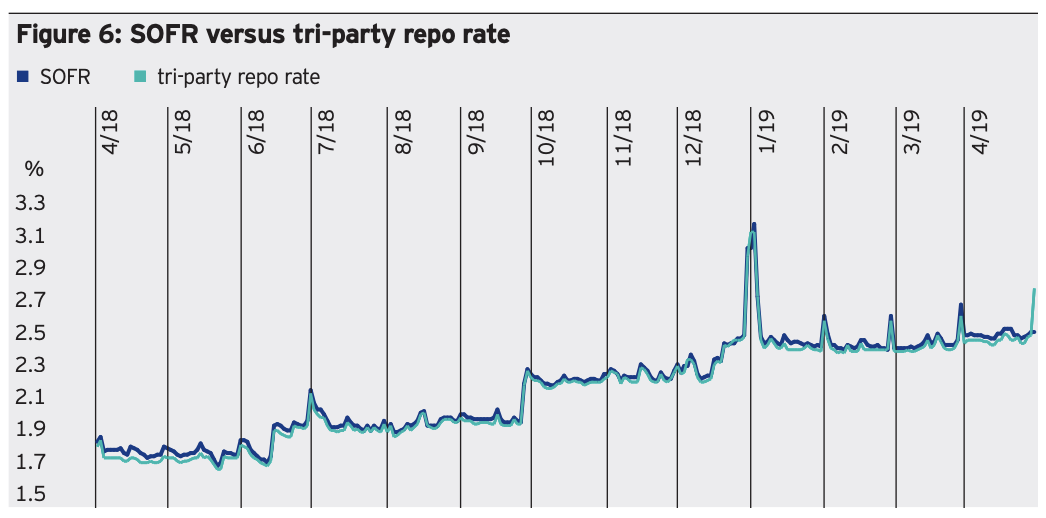

Q: What might be holding back demand for SOFR-based loans and securities? The volatility of SOFR is a concern for many financial institutions and other market participants. SOFR tends to rise at month and quarter-end due to dealer balance sheet constraints. European regulators, especially, have expressed interest in using daily observations of leverage ratios of European banks who participate in US repo markets (a standard currently followed by US financial institutions) and dispensing with month-end data points that have led to window dressing (reduction of repo positions at month-end to reduce the appearance of leverage on bank balance sheets). This practice has contributed to in a spike in repo rates at month-end which has been reflected in similar spikes in SOFR rates.

Q: Do you think SOFR will ultimately gain widespread adoption? We believe a few factors will likely lead to increased activity in SOFR-based instruments and improve liquidity in the new benchmark:

• The impending risk of LIBOR’s cessation should incentivize banks and other financial institutions to transfer liability hedges currently pegged to LIBOR to SOFR.

• The risk of increased volatility in LIBOR as the phase-out date approaches, leading to increased demand for SOFR.

• The migration of new and existing deals to SOFR should increase overall SOFR exposure on the asset side of dealer balance sheets.

• Volatility in repo rates, and therefore SOFR, will likely be dampened by impending changes to European banks’ month-end practice of window dressing, helping to boost comfort levels with SOFR.

Source: Bloomberg L.P., data from April 2, 2018 to April 30, 2019. Past performance is not a guide to future returns.

Source: Bloomberg L.P., data from April 2, 2018 to April 30, 2019. Past performance is not a guide to future returns.

Source: Bloomberg L.P., data from April 2, 2018 to April 30, 2019. Past performance is not a guide to future returns.

Source: Bloomberg L.P., data from April 2, 2018 to April 30, 2019. Past performance is not a guide to future returns.

1 Source: ARRC, Transition from LIBOR, https://www.newyorkfed.org/arrc/sofr-transition ARRC, May 2019. 2 Source: Bloomberg L.P., as of April 29, 2019 3 Source: ICE Benchmark Administration, “US Dollar ICE Bank Yield Index”, Jan 2019. 4 Source: ARRC, April 2019. 5 Forward spread is the price difference between the spot price of a security and the forward price of the same security taken at a specified interval. The forward spread is usually calculated using the forward price one month after the spot price. 6 Spot spread is the price differential of the market price between two securities. 7 Source: ARRC, Transition from LIBOR, May 2019. 8 Source: ARRC, Transition from LIBOR, May 2019. 9 Source: Invesco, April 30, 2019. GSEs are quasi-government entities chartered by the federal government to provide stability in and increase liquidity in the mortgage markets. 10 Source: Invesco, April 30, 2019. 11 Source: Bloomberg L.P., March 31,2019.

Investment risks

The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating. Derivatives may be more volatile and less liquid than traditional investments and are subject to market, interest rate, credit, leverage, counterparty and management risks. An investment in a derivative could lose more than the cash amount invested. Swaps are subject to credit risk and counterparty risk. A decision as to whether, when and how to use futures involves the exercise of skill and judgment and even a well conceived futures transaction may be unsuccessful because of market behavior or unexpected events. If the seller of a repurchase agreement defaults on its obligation or declares bankruptcy, delays in selling the securities underlying the repurchase agreement may be experienced, resulting in losses. Treasury securities are backed by the full faith and credit of the US government as to the timely payment of principal and interest. Obligations issued by US Government agencies and instrumentalities may receive varying levels of support from the government, which could affect the fund’s ability to recover should they default. There is a risk that the value of the collateral required on investments in senior secured floating rate loans and debt securities may not be sufficient to cover the amount owed, may be found invalid, may be used to pay other outstanding obligations of the borrower or may be difficult to liquidate. The risks of investing in securities of foreign issuers can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

Important information Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions, there can be no assurance that actual results will not differ materially from expectations. This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions. All information is sourced from Invesco, unless otherwise stated. All data as of May 31, 2019 unless otherwise stated. All data is USD, unless otherwise stated.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits