Is the Yield Curve Inversion on the Jackson Hole Agenda?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is very light with reports on only three days. Existing and new home sales reports could be interesting and there are many fans of the leading economic indicators. The combination of empty airtime and some Fed news is like an aphrodisiac to the pundits, all of whom are self-affirmed experts on the Fed. The week includes the minutes from the recent FOMC meeting as well as the annual Jackson Hole Symposium. The theme, Challenges for Monetary Policy, could include nearly anything. The full agenda is announced on Thursday and we know that Chairman Powell will speak on Friday morning. Since market commentators believe that the Fed should focus on the most recent market concerns, I expect the question:

Will the yield curve inversion be part of the Jackson Hole Agenda?

Last Week Recap

In last week’s installment of WTWA, I focused on investor reaction to the recent volatility, asking if you should get out, hide out, or ride it out. That was a good guess for the topic of the week, with market action continuing to drive daily headlines and red “alert” notices on financial television. Trade news was largely responsible for the Monday and Tuesday action, proving that the market continues to treat a tweet and a planned phone call as news. Wednesday’s trading came as a reaction to the temporary inversion of another part of the yield curve, the 2-10 segment.

Those who considered the question with us last weekend were better prepared to deal with another roller coaster week. It helps to have a plan, and that comes from thinking about the week ahead.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, which combines a lot of information in one picture. The full article also includes several other interesting takes on price movement.

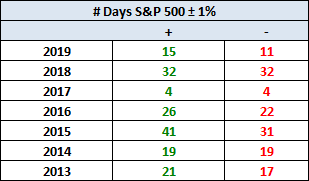

The market lost 1.0% for the week, and the ride was a wild one. The trading range was 4.1% including 3.0% in a single day. My weekly Quant Corner translates this into a volatility calculation which you can compare both to VIX and to past readings. Among the many other helpful charts in this post is the record of +/- 1% trading days over the last few years.

Personal Note

Mrs. OldProf and I are making another try at the vacation we canceled a couple of weeks ago. There may not be a WTWA edition for the next two weekends, but I’ll keep an eye on events. I’ll try to post an update on indicators, especially if something significant seems to be happening. And thanks, once again, to those sending us ideas and recommendations about where we should move.

Noteworthy

The Visual Capitalist asks, Which Countries Have the Most Wealth Per Capita?

You may be surprised by the list, and even more so by the difference between the mean and median results. Here is an image of the static chart, but I cannot do justice to the wonderful, animated chart in the post. There is plenty of information packed into the clever animation.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. The results are now positive in all three of the time frames. The long-term indicators are especially positive; the more volatile short-term indicators have turned positive. NDD remains cautious about the remainder of 2019, noting revisions in some of the quarterly data.

The Good

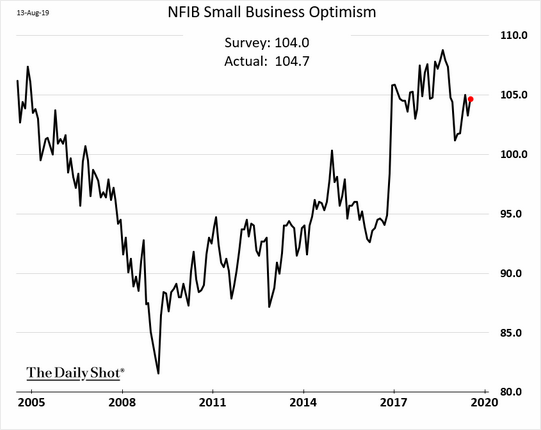

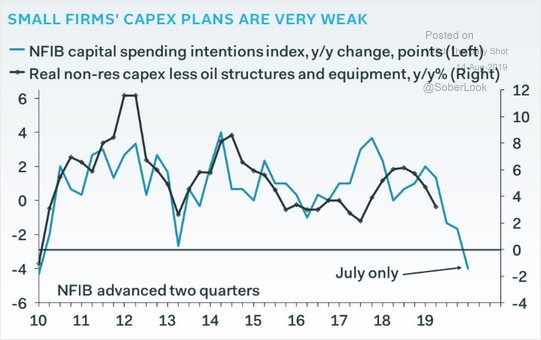

- The NFIB Small Business Optimism Index increased from 103.3 in June to 104.7 in July. The chart below is from The Daily Shot. Gene Epstein (Barron’s) comments on the reasons behind the distinctive Trump-era improvement. Beyond the headline number is weakness in planned capex.

- Mortgage applications increased 21.7% for the week ending 8/10. The prior week change was 5.3%.

- Mortgage delinquencies remain at the lowest level in over 20 years. (CoreLogic)

- Rail traffic is still in contraction for Steven Hansen’s (GEI) economically intuitive sectors, but there are signs of improvement.

- The NAHB Housing Market Index increased to 66 in August from July’s 65.

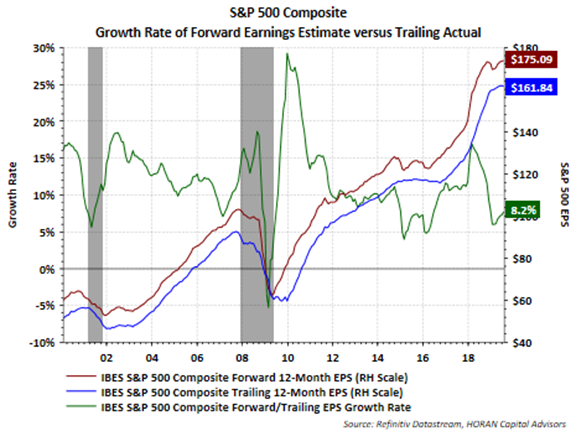

- Forward earnings estimates remain solid. David Templeton (HORAN) explains the effect of past one-off spikes and more favorable comparisons.

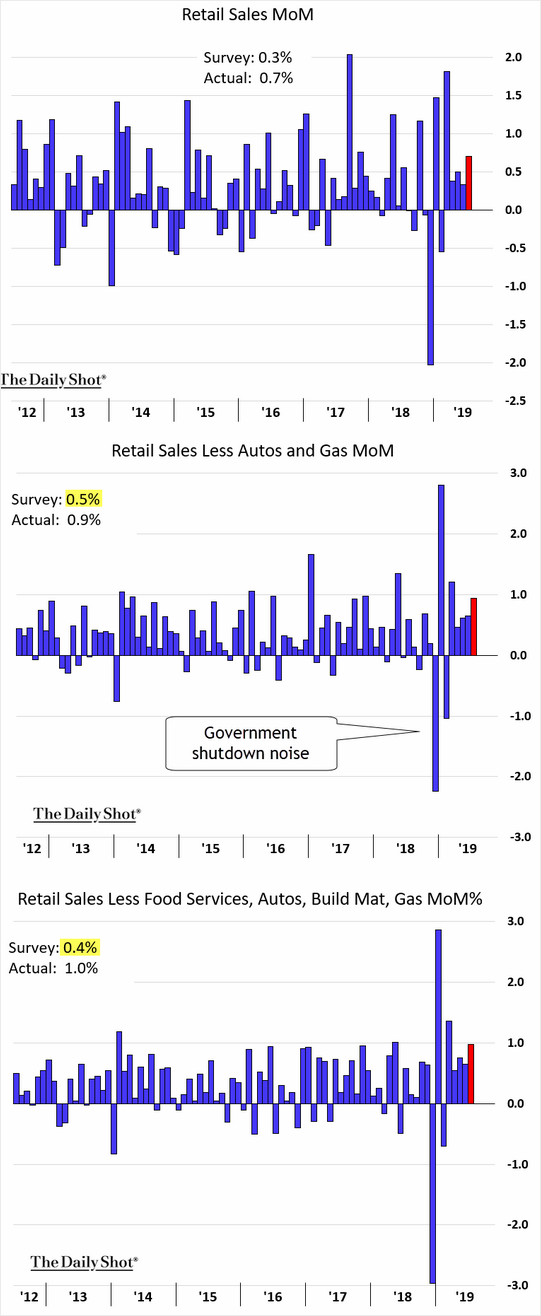

- Retail sales for July grew 0.7%, much better than expectations of 0.3% and June’s 0.3%.

- Building permits for July posted a SAAR of 1336K, better than the expected 1260K and June’s (upwardly revised) 1232K.

The Bad

-

CPI increased 0.3% in July, above June’s 0.1% and expectations of 0.2%. Core CPI also increased 0.3%, higher than the expected 0.2%.

-

Initial jobless claims increased to

220K, up from last week’s 211K and worse than expectations of 215K. -

Industrial production for July declined. The change of -0.2% was worse than the expected gain of 0.1%. The June report, however, was upwardly revised, from 0.0% to 0.2%.

-

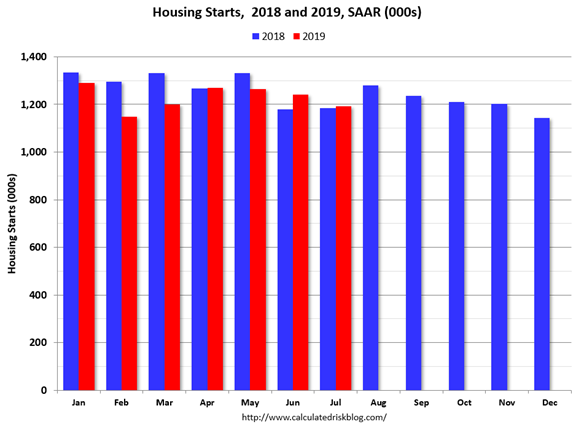

Housing starts for July

My guess was starts would be down slightly year-over-year in 2019 compared to 2018, but nothing like the YoY declines we saw in February and March. Now it is possible starts will be up slightly in 2019 compared to 2018.

-

The July Sea Container Count still shows economic weakness. (Steven Hansen, GEI).

-

Michigan Consumer Sentiment declined to 92.1 on the August preliminary reading. July’s final read was 98.4 and expectations were for a smaller decline to 97.7.

- Hong Kong protests and the response both grew in intensity.

- The trade war got even worse

Trump Ties Trade Deal to China Action in Hong Kong, Suggests Meeting With Xi

China vows to take ‘necessary countermeasures’ against US tariffs

The Ugly

The GE allegations. Investors need accurate information. Blowing the whistle is a career danger and often not rewarding. The result is the combination of whistle blowers like Harry Markopolos (of Bernie Madoff Ponzi fame) and hedge funds that can front run the news. In this case, Markopolos provided the report to “an unidentified hedge fund before its release and will share in the profits, if any.” (WSJ and Barron’s). The allegations have implications for other companies dealing in long-term care insurance.

As is often the case with things that strike me as “ugly,” I do not have a clear solution in mind. Or maybe no “solution” is needed. Like other market veterans, my reaction is that this just doesn’t feel right.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

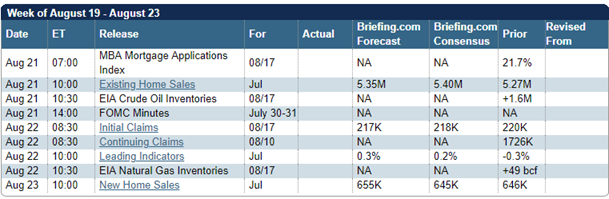

The Calendar

The economic calendar is light, and many market participants are on vacation. The key economic reports will relate to housing, but the focus will be on the Fed. We have both the minutes from the July FOMC meeting and the start of the Jackson Hole Symposium.

And of course, we can expect tweets and retweets and hope for no major international incidents.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

With a small economic calendar and Fed news on the calendar, the punditry has an easy method for filling news space. Since they are already issuing recession warnings based upon the loud “message” from the bond market, they know what is important. The question for them is whether the Fed will recognize the danger. Even though the Jackson Hole meeting is not intended for current policy announcements, pundits will be asking:

Is the yield curve inversion on the Jackson Hole agenda?

Background

The 2/10 yield curve inversion and Wednesday’s market decline moved the recession prospects to the front page for mainstream media.

Markets are braced for a global downturn proclaims the Economist. And that is one of the more moderate sources.

A recession will come. How bad will it be? asks the Washington Post.

Bloomberg is more nuanced, noting expert commentary on other factors influencing the market expectation.

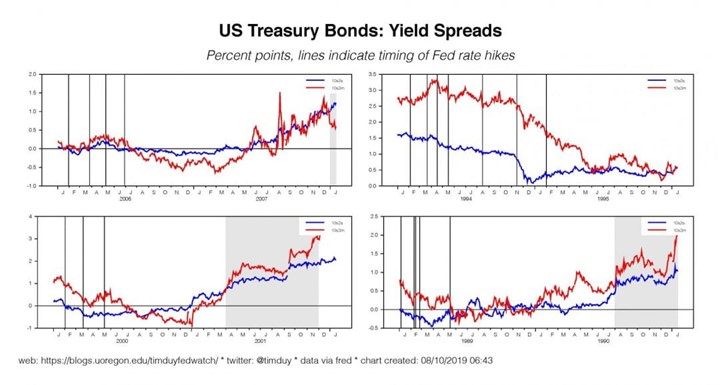

The Bond Market Message

James Picerno writes that the bond market is “all-in” on a near-term economic contraction. He notes that this ignores recent strength in economic data like retail sales. More analysis here.

Tim Duy’s analysis, Don’t Panic. Yet., takes a deeper look. He notes that risks have increased, but the Fed is likely to be more aggressive in its response. That said, “..they will not be inclined to be as reactive to the yield curve as perhaps market participants desire. Remember, an inverted yield curve is a long leading indicator:

And some on Wall Street see it as a red herring. (Kate Rooney, CNBC)

Dr. Ed Yardeni’s study of the subject showed that “An inverted yield curve has predicted 10 of the last 7 recessions.” He suggests that the causal relationship is that an inverted yield curve implies a credit crunch, which is nowhere in sight.

When will a recession come?

Eddy Elfenbein has a simple but accurate description:

With the 2/10, we gain a rare example of a forward indicator with a decent track record, but it comes at the expense of timing. Simply put, the world doesn’t automatically explode once the 2/10 gets inverted. It’s more of a dimmer switch than a toggle.

The key is that the 2/10 isn’t bad news itself. The world of finance loves to fetishize numbers. Instead, we should focus on what those numbers represent. An inverted 2/10 spread is basically like all the fire trucks being down at Arby’s having lunch. When trouble does come—and it will—the response will be more difficult.

Bloomberg analyzes past inversions, showing the wide variation in lead times.

Prof. Duy notes that “we can pretty much guarantee that we are not yet at the peak of this cycle….The upshot is that an inverted yield curve does not mean a recession is right on top of us.” He cites a variety of recent economic data in support of this point.

How bad will it be?

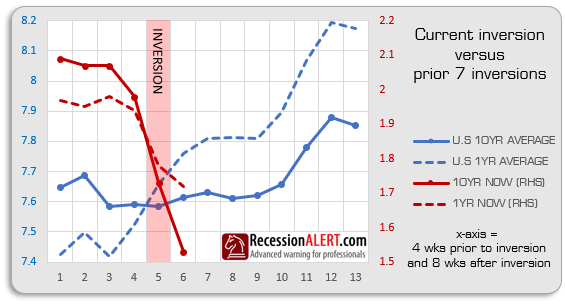

Some experts see the data as suggesting a mild recession. RecessionAlert, one of our regular sources, notes that the “current inversion process is very different from the past.” The key is that both long and short rates have been falling rapidly. In general, past inversions have included both rising. The full article is well worth a read.

In his reports to clients, business cycle expert Dr. Robert Dieli has made a similar point.

The stock reaction might be counterintuitive.

Can policy changes improve the recession odds?

The Federal Reserve Can Conquer the Yield Curve because this time it is reacting immediately by reducing rates. In the past, it has increased rates after the inversion.

Or by ending the trade war, which most see as the source of the concern about weak global growth.

Business Insider cites an August study from the New York Fed. This supplement to the regular Empire State release includes supplemental questions. Among other conclusions, they report:

According to the survey, 79% of manufacturers and 60% of service firms said that recent increases in tariffs have raised input costs at least slightly. An additional 14% of manufacturers and 12% of service firms said that the increases were substantial. All numbers represented a marked increase from the August 2018 survey.

What are the biggest recession risks?

- Declining business confidence because of policy uncertainty.

- A fight between Chairman Powell and the President.

Implications

For all of these reasons, we should not expect a dramatic Fed announcement at Jackson Hole, nor should we panic over this indicator. Careful watching of other indicators, as I have been doing for months, is the order of the day.

I’ll have my own observations in today’s Final Thought.

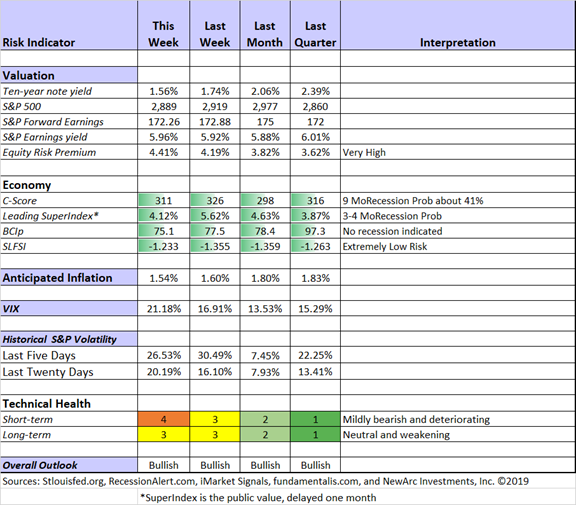

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term technicals have turned bearish and are trending worse. Long-term technicals deteriorated to neutral. Recession risk is still in the “watchful” area with the odds up a notch. We are seeing little confirmation for the risk signals, which we have been monitoring since May. The 2/10 temporary inversion is not the best measure, so it does not affect our estimate. It is also important to look for confirmation rather than blindly following a single indicator.

Considering all factors, my overall outlook for investors remains bullish.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis.

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession.

Guest Sources

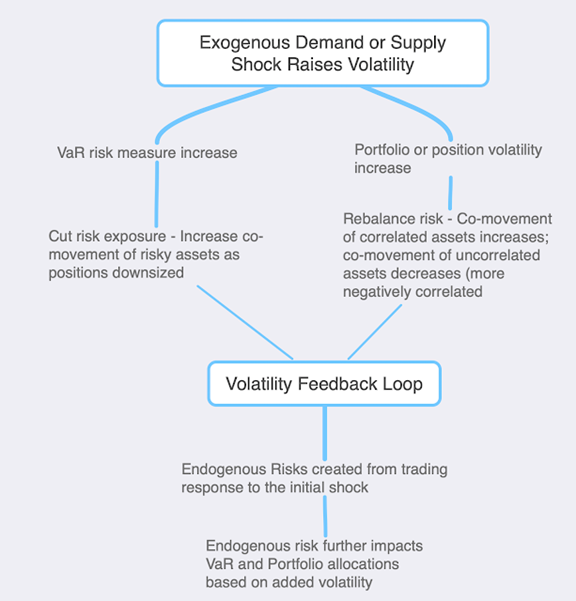

Mark Rzepczynski explains why exogenous supply and demand shocks are behind recent increases in volatility. This chart shows why the normal rebalancing procedures of many firms provide volatility feedback.

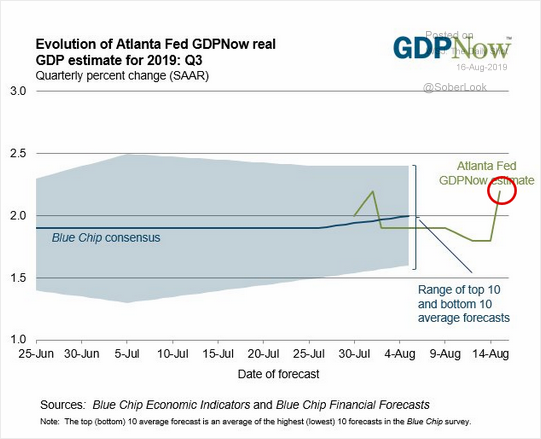

The Atlanta Fed GDP estimate is well out of recession range.

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I try to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades described are certainly not suitable for everyone.

This week’s edition discusses how traders react when there is a sharp selloff. As always, we include advice from top experts and share some picks from our trading models. Pulling it all together and providing counterpoint drawn from fundamental analysis is our regular series editor, Blue Harbinger.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Nick Maggiulli’s The Seduction of Above Average. He begins with familiar data showing that 80% of active managers fail to beat their benchmarks for periods of three years and longer. Then he writes:

However, I want to take the other side of this argument. If 80% of stock pickers won’t beat their benchmark net of fees, this implies that 20% of them will beat their benchmarks.

Now think about this from a stock picker’s perspective. They are likely intelligent, well-educated, and have competed their way to the top of the academic hierarchy throughout their lives.

He then provides a good explanation of how easy it is to think you are better than average in a given group. Just “being smart doesn’t imply that you will be a good stock picker…” Lots of smart people convince themselves otherwise.

His conclusion is excellent.

The only way to be above average as an investor is to invest differently from the masses. That’s it. Whether that means forgoing a market capitalization weighted index for individual stocks, or diversifying into assets that others shun, you cannot invest like the crowd and expect better-than-crowd performance. To re-imagine a famous Jerry Rice quote:

Today I will invest like others won’t, so tomorrow I can earn what others can’t.

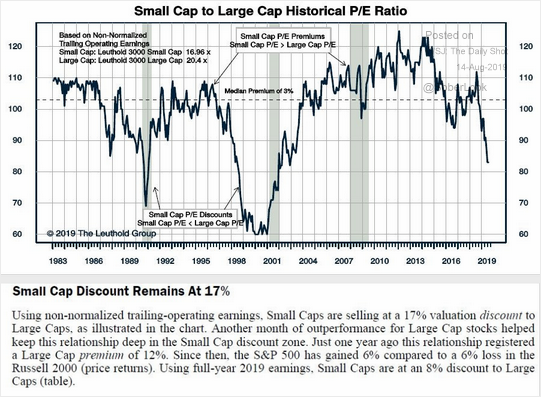

The implication for those of us who seek market-beating returns – certainly me and perhaps you – is that we must have an intelligent and disciplined approach. Then, because it is different, we need to remain confident when it is lagging a market average. (See the small cap returns below for an example).

Stock Ideas

Chuck Carnevale has another great post describing why your stock analysis should emphasize soundness, not rate of return. He illustrates the key principles of valuation and earnings growth, using four disparate but well-known examples. Take time to listen to the video lessons.

Blue Harbinger uses the selling (down 21%) in Monroe Capital (MRCC) as a platform for discussing risk and reward in business development companies (BDCs). The post does not make an immediate “buy” recommendation – just an expression of interest. It is a great lesson about the BDC investment space. Those who are tempted by this type of investment should look at what just happened as well as what might happen next. Those who own non-traded BDCs are merely blind to what might be happening.

Barron’s cover story, Wall Street Has Abandoned Oil and Gas Stocks. You Shouldn’t, is a comprehensive look at the possibility of a rebound. There are plenty of ideas in various subsectors. Those interested in this sector should take a look. Key quote:

What’s more, even if there is a global growth slowdown, near-term oil demand isn’t likely to fall much, if at all. Demand has risen steadily in recent decades, showing resiliency even during deep recessions such as the one that accompanied the financial crisis.

Kirk Spano explains the factors which might drive oil prices higher.

Double Dividend Stocks suggests two REITs that have held up during recent market declines.

Another argument for small caps: a 17% discount. Please note that these stocks have been “out of favor” for about four years. Is that a trend, or is the long-term median a better indicator?

How about Cisco (CSCO)? D.M. Martins makes the case that the recent decline is an opportunity.

William Stamm explains why ADP meets his tests – a dividend aristocrat with good total return and reasonable prospects.

Personal Finance

Abnormal Returns is the go-to source for anyone serious about the investment business. The Wednesday edition has a special focus on personal finance, with plenty of ideas for the individual investor. As always there are many good links. My favorite this week is The White Coat Investor’s Ownership Has Its Privileges. Starting with the difference between paying interest and collecting interest, he suggests six ways to become an owner. Some of the points (controlling expenses) apply to everyone while others (controlling your work) are ideas that many people have not considered.

The sixth point emphasizes entrepreneurship, which can be rewarding but is certainly not for everyone. Be sure you have a supportive life partner who can ride through the inevitable tough times. (Yes, Mrs. OldProf was pretty good at that.)

Watch out for…

Bank stocks, where the yield is not as safe as it is for utilities. (Barron’s)

Bonds Are Frickin’ Expensive, writes Cliff Asness. He uses a clever combination of yield and slope of the curve, analyzes the correlations, and produces an analysis I have not seen before.

REITs as an alternative to stocks. Daniel Sotiroff (Morningstar) makes the case that some are “just stocks that look a little different.”

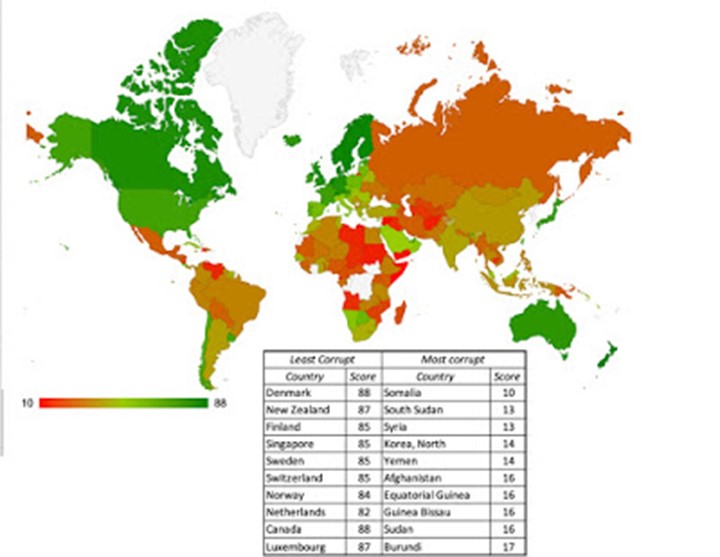

Country risk. Valuation guru Aswath Damodoran provides an update on the major sources of risk: Life cycle, Political (including corruption and violence), Legal, and Economic Structure. This is valuable information for anyone contemplating worldwide investments, including ETFs.

Final Thought

Investors should not expect much from the Jackson Hole news. If the early week hype suggests otherwise, it would be a cautionary sign.

CNBC reports what investors are hoping to get: An indication of “whether the Fed is at the beginning of a serious rate cutting cycle – or just intending to cut a few times, as insurance against a possible downturn”. No other alternative is mentioned.

MarketWatch tells us what they should really expect. The Fed is unlikely to give a clear signal about the future policy path, keeping options open for the next meeting.

As you join me in monitoring recession odds, here are some themes to keep in mind.

A “false positive” in a recession signal can be costly. Those following a widely publicized 2011 signal missed out on years of stock gains. My plan is to reduce equity exposure if there are signals confirming the early hints. I studied the topic carefully in 2010, finding the best sources and methods. This was crucial in dodging the false positive and will help in reducing risk as needed.

Economists are often criticized for an inability to forecast recessions. Non-economists with a quantitative bent use the limited available data to create indicators claiming uncanny precision. Consider these statements:

- An inverted yield curve has preceded each of the last six recessions.

- A low unemployment rate has preceded every recession

…Just about every major bottom in the unemployment rate has preceded a recession. Just look at recent history; the unemployment rate bottoms and a recession begins in 1970, it bottoms and a recession begins in the late 80s, the unemployment rate bottoms again around 1999, and the dotcom bubble explodes, it bottoms around 2007/2008 and the great recession begins. (Example here).

The first statement may be true, but dodges all of the issues about timing and false positives. It is often accompanied by a false assertion that stocks “usually” decline long before a recession.

The second statement may also be true, but it has no predictive value. By definition, recessions begin at business cycle peaks. In an improving economy one never knows whether a new high will become a peak, and you certainly can’t jump at the first downtick in a series. This effort to make good news sound bad is dangerously misleading

How can you tell this difference between the newbies and the experts?

- A logical and theoretically sound reason for the forecasting method.

- A real-time track record.

- An understanding that you cannot use hundreds of indicators to explain a handful of events.

There are many articles filled with attractive charts and persuasive sounding arguments. That is not a good test.

Economic data nearly always paint a mixed picture. Choose sources who see and balance the evidence. Avoid those that make one-sided laundry lists and change indicators whenever it suits.

Some other items on my radar

I’m more worried about:

- Iran confrontations. Drones and tanker seizures today, and what tomorrow? Direct engagement increases the chance for a conflict-starting incident. (BBC)

- A renewed arms race. The evidence of new Russian delivery systems and tests evokes memories of the (expensive) bad old days. (NYT)

I’m less worried about

- The Treasury “flooding the market with debt.” (MarketWatch). There is plenty of demand and a wisely managed adjustment to debt would increase the yield-curve slope at a time when long-term rates are attractive.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits