In the decade following the Global Financial Crisis, global fixed income yields have remained low by historical standards —and many investors have turned to dividend growth stocks for their combination of yield and capital appreciation potential. At Invesco Unit Trusts, we don’t see this trend abating anytime soon. In fact, we believe the current environment may be especially well-suited to investing in dividend growth strategies, due to four macro factors described below.

A history of higher returns and lower volatility

Before we discuss today’s environment, what’s the appeal of dividend growth stocks in general? Companies that are growing their dividends tend to be associated with advantageous business models, strong fundamentals, and good stewardship of shareholder capital. While these stocks can be eclipsed by non-dividend-paying momentum stocks in the short term, they have proven to be an effective strategy to generate attractive returns with lower volatility in the long term (Figures 1 and 2).

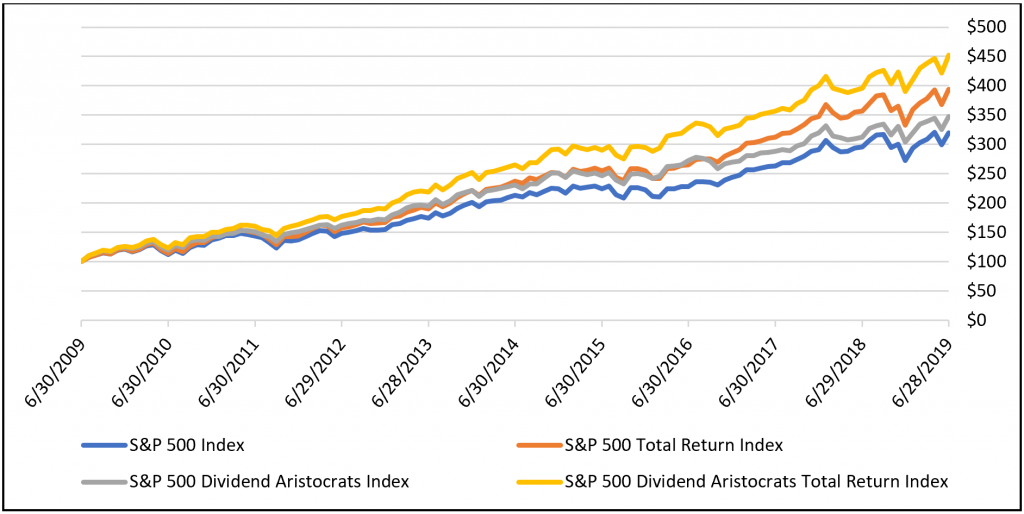

Figure 1: Dividend growth stocks have a history of higher returns Growth of $100 invested in the S&P 500 Index and the S&P 500 Dividend Aristocrats Index, with and without reinvesting dividends, over the past 10 years (6/30/2009 – 6/30/2019).

Source: Bloomberg, L.P. A total return index assumes that dividends are reinvested back into the index. Past performance does not guarantee future results. An investment cannot be made directly into an index.

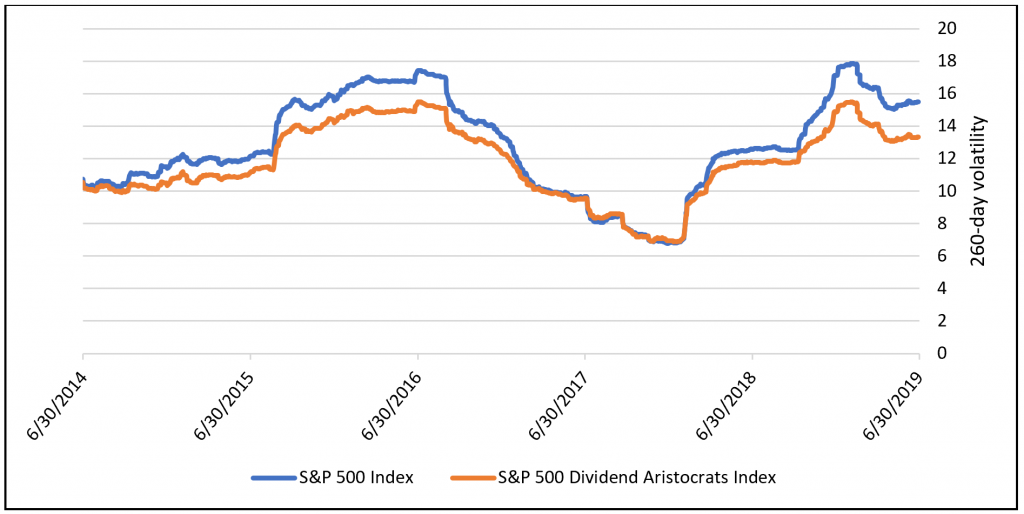

Figure 2: Dividend growth stocks have a history of lower volatility Historical 260-day annualized volatility of the S&P 500 Index and the S&P 500 Dividend Aristocrats Index, over the past five years (6/30/2014 – 6/30/2019).

Source: Bloomberg, L.P. The 260-day price volatility equals the annualized standard deviation of the relative price change for the 260 most recent trading days closing price, expressed as a percentage. Past performance does not guarantee future results. An investment cannot be made directly into an index.

Four macro factors supporting dividend growth investing

Macro factor 1: Lower expected equity market capital returns. From the market low on March 6, 2009, through June 30, 2019, the S&P 500 Index has returned over 17% annually, inclusive of dividend reinvestment.1 While bull markets don’t die of old age, we believe that historical market returns and current market valuations suggest that it’s unlikely the S&P 500 Index will repeat its stellar performance over the next decade.

Why does this matter to dividend growth investors? In a world of lower expected equity market capital returns, the importance of reliable and growing dividends increases. By way of hypothetical example, a 2% to 3% dividend yield has a much bigger impact on total return when performance is 7% versus 17%. Moreover, under a scenario of limited capital appreciation, dividend growth may help bolster long-term total return by potentially driving higher future dividend yields.

Macro factor 2: Stable-to-falling interest rate environment. From its recent November 2018 high through June 30, 2019, the 10-Year US Treasury yield has fallen 122 basis points to 2.01%.2 In March, the Federal Reserve (Fed) paused its rate hikes. Then in June, the Fed removed the word “patient” from its market commentary, cementing its dovish pivot and signaling the potential for future rate cuts.

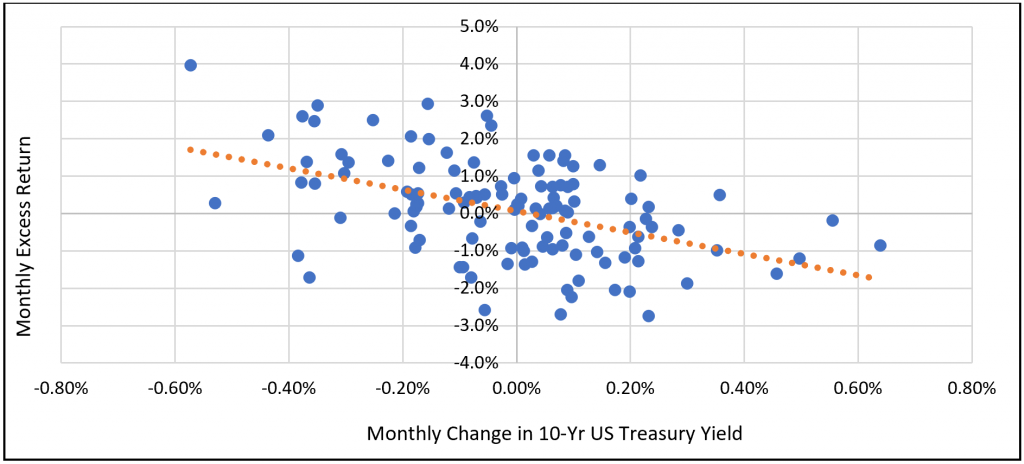

Why does this matter to dividend growth investors? In a falling interest rate environment, bond yields fall and the relative attractiveness of dividend growth equities increases. Most bonds typically only provide fixed nominal income, which doesn’t grow and gets eroded by rising inflation. Lower bond yields also theoretically limit potential future bond capital appreciation. Growing dividend payments provide an alternative to stagnant fixed income coupons while retaining the potential for higher capital appreciation. Versus the broader equity market, dividend growth equities have also historically performed well during falling interest rate regimes (Figure 3).

Figure 3: Dividend growth equities have outperformed the broader equity market when interest rates have fallen Monthly change in the 10-year US Treasury Yield, plotted against the monthly excess return of the S&P 500 Dividend Aristocrats Index versus the S&P 500 Index, over the past 10 years (6/30/2009 – 6/30/2019)

Source: Bloomberg, L.P. Past performance does not guarantee future results. An investment cannot be made directly into an index.

Macro Factor 3: Inflation uncertainty. While US inflation has been benign in recent years, that doesn’t mean that inflation will remain permanently subdued. Additionally, certain expenses, such as health care, have historically risen significantly faster than overall inflation.

Why does this matter to dividend growth investors? Dividend growth equities may provide a natural hedge against the potential impact of rising inflation. In the case of retirees relying on dividends for income, growing dividend payments may help keep pace with monthly expenses, which tend to rise at least in-line with inflation. And with rising life expectancies, retirement can last decades, so keeping up with inflation is essential to preserving one’s current lifestyle. Even at just 3% inflation, the purchasing power of $1 falls to $0.48 over 25 years.

Macro Factor 4: Aging demographics. Globally, the massive baby boomer generation is retiring and entering the de-accumulation phase of their lives. In the US alone, 10,000 people turn 65 each day.3

Why does this matter to dividend growth investors? Since dividend growth equities have historically provided an attractive mix of income growth, capital appreciation, and downside volatility mitigation, they are a popular investment choice with retirees. With stock prices partially influenced by supply and demand dynamics, the swelling population of retirees could provide a demographic tailwind to the demand for dividend growth equities.

Talk to your advisor: Invesco Dividend Sustainability Trusts Interested in the total return opportunities that dividend growth equities can provide? Talk to your financial advisor and explore the Dividend Sustainability Portfolios from Invesco Unit Trusts, a suite of portfolios of common stocks and American Depositary Receipts professionally selected based on company fundamentals from a pool of securities demonstrating consistent dividend growth historically.

1 Source: Bloomberg, L.P. 2 Source: Bloomberg, L.P. 3 Source: Forbes, “Social Security feels pinch as baby boomers clock out for good,” June 21, 2018

Important information Blog header image: Ryoji Iwata / Unsplash.com The S&P 500® Index is an unmanaged index considered representative of the US stock market. The S&P 500® Dividend Aristocrats® Index includes companies that are currently members of the S&P 500® Index, have increased dividend payments each year for at least 25 years, and meet certain market capitalization and liquidity requirements. Common stocks do not assure dividend payments. Dividends are paid only when declared by an issuer’s board of directors and the amount of any dividend may vary over time. Standard deviation measures a portfolio’s or index’s range of total returns in comparison to the mean. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc. and broker dealers including Invesco Distributors, Inc. Both firms are indirect, wholly owned subsidiaries of Invesco Ltd. There is no assurance the trust will achieve its investment objective. An investment in this unit investment trust is subject to market risk, which is the possibility that the market values of securities owned by the trust will decline and that the value of trust units may therefore be less than what you paid for them. This trust is unmanaged and its portfolio is not intended to change during the trust’s life except in limited circumstances. Accordingly, you can lose money investing in this trust. The trust should be considered as part of a long-term investment strategy and you should consider your ability to pursue it by investing in successive trusts, if available. You will realize tax consequences associated with investing from one series to the next. Before investing, investors should carefully read the prospectus and consider the investment objectives, risks, charges and expenses. For this and more complete information about the trust(s), investors should ask their advisers for a prospectus or download one at invesco.com/unittrust. The S&P 500 Dividend Aristocrats Index consists of stocks of those companies in the Standard & Poor’s 500 Index that have increased their actual dividend payments in each of the last 25 years. STANDARD & POOR’S, S&P, S&P 500 and DIVIDEND ARISTOCRATS are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a wholly owned subsidiary of S&P Global. Standard & Poor’s Investment Advisory Services LLC (“SPIAS”) is a registered investment advisor and a wholly owned subsidiary of S&P Global, and a part of S&P Global Market Intelligence. SPIAS reviews the Invesco Capital Markets, Inc.’s investment selections for the S&P Dividend Sustainability Portfolio. SPIAS does not provide advice to underlying clients of the firms to which it provides services. SPIAS does not act as a “fiduciary” or as an “investment manager,” as defined under ERISA, to any investor. SPIAS is not responsible for client suitability. Past performance is not indicative of future returns. SPIAS, S&P and their affiliates do not sponsor, endorse, sell, promote or manage any investment fund or other vehicle that is offered by third parties and that seeks to provide an investment return based on a SPIAS investment strategy or the constituents or the returns of any index. SPIAS, S&P and their affiliates make no representation regarding the advisability of investing in any such investment fund or other vehicle. With respect to recommendations made by SPIAS, investors should realize that such information is provided only as a general guideline. SPIAS does not take into account any information about any investor or any investor’s assets when providing its services. There is no agreement or understanding whatsoever that SPIAS will provide individualized advice to any investor. SPIAS does not have any discretionary authority or control with respect to purchasing or selling securities or making other investments. Individual investors should ultimately rely on their own judgment and/or the judgment of a financial advisor in making their investment decisions. There is no assurance that future dividend payouts will equal or exceed past dividend payouts. Standard & Poor’s parent company, S&P Global, may be one of the constituents of the S&P 500 Dividend Aristocrats Index and may be included in the portfolio based solely on quantitative measurements.

For additional disclaimers and disclosures for SPIAS, please see http://www.standardandpoors.com/ regulatory-affairs/spias/en/us

Petra DeLeo is an Associate Equity Portfolio Manager on the Unit Investment Trust Equity Portfolio Management and Research team for Invesco.

Ms. DeLeo has been with the firm since 2017 and in the industry since 2006 in various roles including research, portfolio management and trading. Prior to joining Invesco, she served as an equity research analyst at Morningstar and Calamos.

Ms. DeLeo graduated magna cum laude with a BA degree in economics from Dartmouth. She is a Chartered Financial Analyst® (CFA) charterholder. She holds the Series 7 and 63 designations.