In his speech at the Kansas City Fed’s annual monetary policy symposium in Jackson Hole, Fed Chair Powell discussed the challenge of keeping the U.S. economy “in a favorable space” in the face of significant risks. Minutes of the July 30-31 Federal Open Market Committee meeting had shown that officials were split on the appropriate course of action at that time. There was no presumption the further rate cuts would be required. However, trade policy uncertainty and concerns about the global economic slowdown have increased since the FOMC meeting, and Powell signaled that the central bank “will act as appropriate to sustain the expansion.”

How does the Fed make its policy decisions? Powell:

“Informingjudgmentsabouttheappropriatestanceofpolicy, the Committeedigestsabroadrangeofdataandotherinformationtoassessthecurrent state of the economy, the most likely outlook for the future, and meaningful risks to that outlook. Because the most important effects of monetary policy are felt with uncertain lags of a year or more, the Committee must attempt to look through what may be passing developments and focus on things that seem likely to affect the outlook over time or that pose a material risk of doing so. Risk management enters our decision-making because of both the uncertainty about the effects of recent developments and the uncertainty we face regarding structural aspects of the economy, including the natural rate of unemployment and the neutral rate of interest. It will at times be appropriate for us to tilt policy one way or the other because of prominent risks.”

How does trade policy uncertainty fit into the Fed’s policy decisions?

“We have much experience in addressing typical macroeconomic developments under this framework. But fitting trade policy uncertainty into this framework is a new challenge. Setting trade policy is the business of Congress and the to use monetary policy to foster our statutory goals. In principle, anything that affects the outlook for employment and inflation could also affect the appropriate stance of monetary policy, and that could include uncertainty about trade policy. There are, however, no recent precedents to guide any policy response to the current situation. Moreover, while monetary policy is a powerful tool that works to support consumer spending, business investment, and public confidence, it cannot provide a settled rulebook for international trade. We can, however, try to look through what may be passing events, focus on how trade developments are affecting the outlook, and adjust policy to promote our objectives.”

Powell cites three factors (which were also noted in the FOMC minutes):

“ the year has progressed, we have been monitoring three factors that are weighing on this favorable outlook: slowing global growth, trade policy uncertainty, and muted inflation. The global growth outlook has been deteriorating since the middle of last year. Trade policy uncertainty seems to be playing a role in the global slowdown and in weak manufacturing and capital spending in the United States. Inflation fell below our objective at the start of the year. It appearstobemovingbackupclosertooursymmetric 2 percent objective, but there areconcernsaboutamoreprolongedshortfall.”

Powell notes that the developments over the last few weeks have boosted the downside risks:

“We are carefully watching developments as we assess their implications for the U.S. outlook and the path of monetary policy. The three weeks since our July FOMC meeting have been eventful, beginning with the announcement of new tariffs on imports from China. We have seen further evidence of a global slowdown, notably in Germany and China. Geopolitical events have been much in the news, including the growing possibility of a hard Brexit, rising tensions in Hong Kong, and the dissolution of the Italian government. Financial markets have reacted strongly to this complex, turbulent picture. Equity markets have been volatile. Long-term bond rates around the world have moved down sharply to near post-crisis lows. Meanwhile, the U.S. economy has continued to perform well overall, driven by consumer spending. Job creation has slowed from last year's pace but is still above overall labor force growth. Inflation seems to be moving up closer to 2 percent. Based on our assessment of the implications of these developments, we will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.”

As a consequence, the Fed “will act as appropriate” to keep the economy growing. The FOMC used this phrase in the July policy statement, but in his context it is a strong signal that the Fed will lower short-term interest rates in mid-September.

Data Recap – The focus was on the Fed. The FOMC Minutes showed no presumption that further rate cuts would be needed, but in his Jackson Hole speech, Chair Powell said noted that tariffs had been announced since the late July meeting and the global economic outlook had worsened. He said that the Fed “will act as appropriate” to ensure that the expansion continues.

The FOMC Minutes from the July 30-31 policy meeting showed that officials were divided, with “a couple” of meeting participants preferring a 50 bp move, while “several” favored no change. There was no presumption that further cuts would be needed.

In his Jackson Hole speech, Fed Chair Powell said that “three weeks since our July FOMC meeting have been eventful,” beginning with the announcement of another round of tariffs and “further evidence of a global slowdown.” In light of the implications of these developments, “we will act as appropriate to sustain the expansion.”

China announced retaliatory tariffs against U.S. goods. President Trump tweeted in response that he was “ordering” American firms “to immediately start looking for an alternative to China,” including bringing companies home and making products in the U.S.

The Bureau of Labor Statistics estimates that its annual benchmark revision (to be applied in February 2020) will reduce the March 2019 level of payrolls by 501,000. While that may sound like a lot, it’s a relatively small percentage (-0.3%). It may reduce the 2019 pace of job growth, +223,000 per month, to about +195,000.

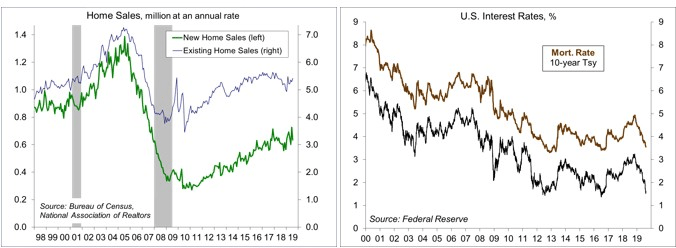

Existing Home Sales rose 2.5% in July, to a 5.42 million seasonally adjusted annual rate (+0.6% y/y).

Click here to enlarge

New Home Sales fell 12.8% (reported ±16.2%) in July to a 635,000 seasonally adjusted annual rate (+4.3% y/y). The figure for June was revised higher (to 728,000, from 646,000).

The Index of Leading Economic Indicators rose 0.5% in July, vs. +0.1% from September to June. Positive contributions were led by building permits, jobless claims, the stock market, financial conditions, and consumer expectations. Negative contributions were led by ISM New Orders, the factory workweek, and the yield curve.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James