Why are investors incentivized to hold cash? We believe this is partly a result of today’s higher CD rates and high yield savings accounts— making investors now consider how much cash they should hold. In addition, market volatility and greater geopolitical risk have made cash look even more attractive to some investors.

So, what’s the problem?

To see the underlying problem, let’s take a step back and look at the net of inflation return on cash. Once you do, the siren call of cash begins to fade. For many, cash equals certainty. But the comfort of having this certainty in return may come at a cost. There are hidden drags that can have a significant impact on the amount of wealth investors ultimately accumulate.

Hidden costs: Inflation versus purchasing power

One cost is inflation, it represents the increase in an item’s purchasing price. When we make an investment, our hope is for our money to grow so we wind up with more money, so we can buy more things down the road. This second factor is known as an increase in purchasing power. But they are two sides of one coin—how much extra purchasing power we end up with (i.e. how much more we can buy) depends on the role that inflation plays along the way.

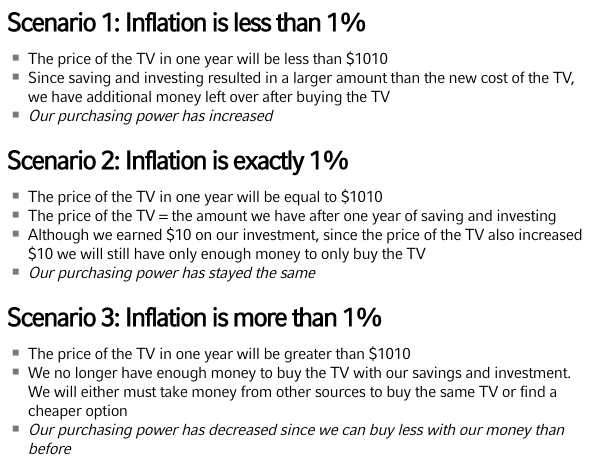

Here’s a simple example to illustrate the impact inflation can have: say we’re looking to purchase a new flat screen TV. After shopping around, we decide on a beautiful, 76’’ LED TV that costs $1000. Being a prudent investor, we consider 2 potential options:

- A. Buy the TV today for $1000

- B. Wait 1 year to buy the TV and invest the $1000 in a CD to earn 1% over the next year

Since we don’t need the TV today, we decide to go with option B and wait until next year to purchase the TV while making some extra money. After investing $1000 in a CD earning 1%, we earn $10 over the next year and our investment grows to $1010. Are we better off? That depends on the impact that inflation has had over the year.

Here’s what could happen:

The real return on an investment

The idea of evaluating investment results after the effects of inflation is known as looking at the real returnon our investment.This is the return that is most meaningful for investors since this tells you how much your purchasing power has gone up or down.

If our real return on an investment is zero, we are keeping up with inflation, but our purchasing power remains the same. If our real return is positive, we are earning more than inflation and we can buy more goods down the road. Obviously, this is the desired result for investors since we are increasing our purchasing power.

Purchasing power risk

But scenario 3 can happen, real returns are negative when inflation is larger than the returns on our investments and purchasing power decreases. This can have significant consequences for investors at or near retirement. This is known as purchasing power riskand represents the risk that prices go up by more than the amount you’ve earned while saving or investing.

Although we may have technically made money by investing, we have lost the ability to purchase the item we originally wanted to buy. It may be easy to live without a brand new 76’’ flat screen TV, but what if you’re simply looking to keep up with the lifestyle you’ve grown accustom to when you are retired?

Beware of the corrosive nature of inflation

We believe most investors need to be aware of inflation and the impact it can have.

It is an important thought to keep in mind when considering cash-like investments. Often, attractive stated rates of return are significantly reduced—or even result in negative real returns—after taking inflation into account.

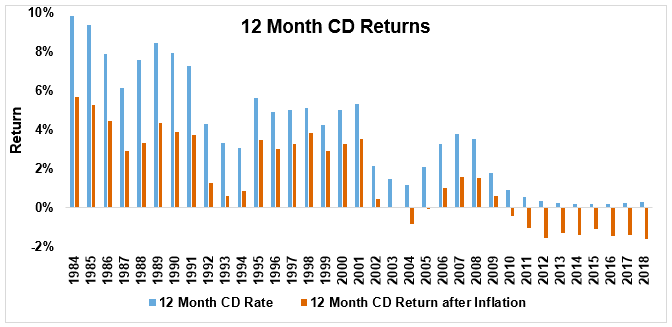

Looking back to 1984, the chart below shows that 12-month CD returns have been reduced by 33% to 75% on average after adjusting for inflation. More recently, due to low interest rates since the Global Financial Crisis, CDs have delivered negative real rates of return since 2010.

Source: CD Rates: Bankrate from 1984-2009; Federal Reserve Economic Data (FRED) 2010-2018. Inflation: FactSet Financial Data.

These potential scenarios can create a real dilemma for investors who desire the certainty that a cash-like investment with a pre-stated rate of return can offer. They don’t like the idea of taking risk in the market yet run the risk of losing their purchasing power by owning cash due to inflation.

What’s the solution?

We believe a potential solution for those investors with longer term time horizons could be a diversified portfolio consisting of historically lower risk investments such as fixed income and asset classes that have done well in periods of rising inflation environments such as stocks and real estate.

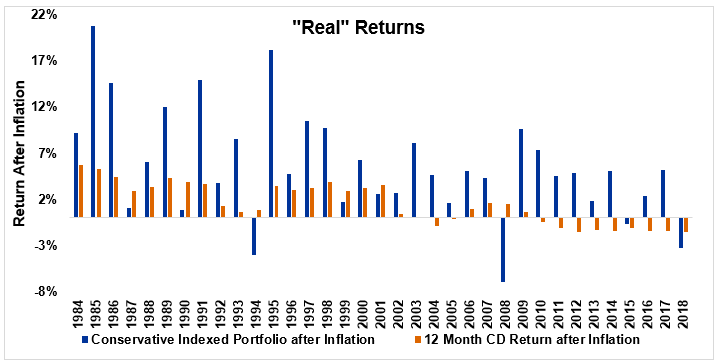

The chart below shows how a portfolio consisting of 80% fixed income, 18% stocks and 2% real assets has performed annually compared to returns from 12-month CDs after accounting for inflation.

Source: Conservative Index Portfolio: Morningstar. Components: 80% Bloomberg Barclays US Aggregate Bond Index; 13% Russell 3000; 5% MSCI EAFE; 2% FTSE NAREIT All Equity REITs. Inflation: Factset Financial Data.

The chart demonstrates that by willing to accept a higher level of risk, the conservative portfolio typically has delivered returns far superior to CDs on an annual basis. In addition, although the conservative portfolio experienced more volatility in certain years, after inflation, CDs have shown more instances of negative real returns – and therefore a loss of purchasing power – than a diversified portfolio.This idea introduces a more important concept for investors to think about when making investment decisions: The risk of possibly losing money vs. the risk of running out of money.

Bottom line

We recommend investors work with a financial advisor to determine their cash needs for the immediate future and for developing a plan to invest in a globally diversified, multi-assetportfolio for their long-term investment needs.

For advisors, sometimes we forget about we can control—or least help control—is investor behavior. We’ve previously written about how addressing the investment behavior of your clients may be the greatest value you provide. And when it comes to delivering value, avoiding behavioral mistakes is a significant contributor to total value while helping your clients reach their desired outcomes.

Disclosures

Bloomberg Barclays U.S. Aggregate Bond Index: An index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities, and mortgage-backed securities. (specifically: Barclays Government/Corporate Bond Index, the Asset-Backed Securities Index, and the Mortgage-Backed Securities Index).

FTSE NAREIT All Equity REITs Index: A free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

MSCI EAFE (Europe, Australasia, Far East) Index: A free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

MSCI Emerging Markets Index: A float-adjusted market capitalization index that consists of indices in 24 emerging economies.

The Russell 3000® Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market.

Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

Diversification does not assure a profit and does not protect against loss in declining markets.

Past performance does not guarantee future performance

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

Copyright © 2019. Russell Investments Group, LLC. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

Russell Investments Financial Services, LLC, member FINRA (www.finra.org), part of Russell Investments.

RIFIS: 21899