Recent economic data reports have continued to paint a mixed picture of the U.S. economy, with strength in consumer spending and a mild recession in manufacturing. On top of this, investors remain concerned about several issues, including global growth, geopolitical uncertainties, trade policy, and an inverted yield curve. However, stock market participants are generally hopeful that a trade deal will be worked out and that the Federal Reserve will come to the rescue. As summer comes to an end, we can expect investors to more seriously evaluate current conditions and the prospects for the remainder of the year.

The 2nd estimate of 2Q19 GDP growth was not much different than the advance estimate (a 2.0% annual rate, vs. 2.1% in the initial estimate). As in the advance estimate, growth was isolated in two sectors: consumer spending and government. Business fixed investment contracted at a 0.6% annual rate in 2Q19 (same as in the advance estimate), but weakness was pronounced in mining structures (which includes oil and gas exploration) and transportation equipment (likely reflecting transitional problems at Boeing). Corporate profits improved in the second quarter, but manufacturers’ profit margins are being compressed by tariffs (especially after the May 10 escalation). Residential homebuilding fell for the sixth consecutive quarter in 2Q19. Normally, that’s what you would see in a recession, but in this case, the problem is supply, not demand. The missing element in the housing recovery has been in start-up homes. Higher building costs (partly reflecting tariffs), a lack of skilled labor, and a scarcity of lots on which to build have constrained supply at the low end of the housing market, while strong demand has driven up prices, reducing affordability (despite a sharp drop in home mortgage rates). Residential fixed investment accounts for less than 4% of Gross Domestic Product, so the housing weakness isn’t critical to the outlook for overall growth, but it is a problem.

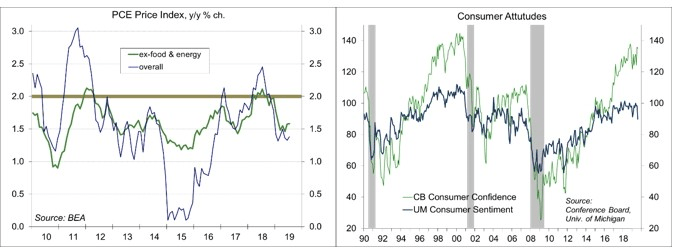

With personal consumption expenditures accounting for 68% of GDP, the strength of the household sector is key. The fundamentals appear sound. Job gains and wage growth should continue to support spending in the near term. The July data suggest that inflation-adjusted consumer spending is tracking at over a 3% annual rate in early 3Q19. Measures of consumer attitudes have been mixed. The Conference Board’s Consumer Confidence survey has a more direct measure of labor market perceptions, which have been robust. That’s missing (at least directly) from the University of Michigan’s Consumer Sentiment survey, where the August reported noted increased concerns about tariffs and trade policy. Press reports of the inverted yield curve, “recession,” and stock market volatility may have an impact on spending, but more at the high end.

On the global front, economic data have also been mixed, but generally soft. Canadian GDP growth for 2Q19 was reported stronger than expected (+3.7%), but much of that reflected a normalization in exports following earlier softness (GDP rose at a +0.5% in 1Q19). Many advanced economies reflect that same split as seen in the U.S. – that is, relative strength for consumer spending, but softness in manufacturing activity. New leadership is on the way in Europe (both for the European Union and the European Central Bank), but these are expected to be smooth transitions (note that both the ECB and the U.S. Fed will be led by lawyers, not economists). Brexit and Hong Kong are significant geopolitical risks. Japan and South Korea are fighting their own trade conflict. China’s current softness reflects more than trade tensions. Rising debt in that country has been a growing concern over the last decade. Trade tensions between the U.S. and China have spilled over to the rest of the world. Emerging economies appear unlikely to lead the global economy.

As with any economic shock, the impact of tariffs depends on the breadth, magnitude, and duration. With the September 1 increase in tariffs, more Chinese goods are subject to tariffs, and nearly all will be in mid-December. The May 10 increase in tariffs (from 10% to 25%) was a big deal, and it will be some time before we see the full impact. Finally, while stock market investors appear to be hopeful that we’ll see progress in trade talks in mid-September, it’s unclear whether those talks will happen. President Trump has tweet-ordered U.S. firms out of China, but it’s unclear whether that is a negotiating ploy. Supply chains have already been migrating away from China, but that is difficult (the one thing producing in China gets you is scale – massive scale, that can’t be replicated elsewhere). China appears to believe that it can wait it out and deal with a new U.S. president in 2021. However, a get-tough-with-China approach has been adopted by the leading Democratic contenders. The worse-case scenario is that the trade conflict won’t end and the U.S. and Chinese economies will permanently split (bashing China remains a popular election strategy, especially in the Midwest). Despite the market optimism, things are likely to get worse before they get better and there are still significant downside risks.

Investors expect that the Federal Open Market Committee will lower short-term interest rates again on September 18. Minutes of the July 30-31 policy meeting (when the FOMC lowered the federal funds target range by 25 basis points) showed some reluctance to cut rates at that time. While there is no playbook for running monetary policy in the midst of a major trade war, officials do not believe that the downside effects of a trade war can be offset by monetary policy. Last week, in a Bloomberg editorial, former New York Fed president William Dudley said that the Fed should not bail President Trump out. Trump has been vocal, of course, in his criticism of the Fed, which prizes its independence and still believes that the current stance of monetary policy is accommodative. Dudley’s comments were not helpful, playing into concerns that the Fed is political. One needs only to examine the detailed FOMC meeting transcripts to see that politics is never an issue in the Fed’s policy deliberations. Yet, public misperceptions continue. Chair Powell has refrained from criticizing the administration’s trade policies, just as past chairs have traditionally not taken sides on tax and spending issues.

Some Fed officials fear that further rate cuts may not do much to fuel growth and are worried that they may fuel a financial bubble, which will eventually unwind, generating adverse effects on the economy. So, contrary to market expectations, a September 18 cut is not a slam dunk. On the other hand, the Fed risks unsettling the financial markets if it runs counter to expectations. The New York Fed surveys financial institutions before the FOMC meetings, asking what it expected to happen if the central bank does x, y, or z. Hence, officials should actively jawbone the markets, if they think the markets have it wrong. The next couple of weeks should be fun.

Data Recap – Stock market participants were generally optimistic that a trade agreement will eventually be worked out between the U.S. and China, although that appears to be largely hope at this point. The economic data were not market-moving.

Real GDP rose at a 2.0% annual rate in the 2nd estimate for 2Q19 (vs. +2.1% in the advance estimate). Consumer spending growth was revised higher (a 4.7% annual rate, but that followed +1.1% in 1Q19). Business fixed investment fell 0.6%, same as in the advance estimate, reflecting a correction in energy exploration and problems at Boeing. Slower inventory growth subtracted 0.9 percentage point from GDP growth, while net exports (a wider trade deficit) subtracted 0.7 percentage point.

Personal Income rose 0.1% in July (+4.6%), with private-sector wages and salaries up 0.2% (+5.6% y/y). Personal Spending rose 0.6% (+4.1% y/y), up 0.4% (+2.7% y/y) adjusted for inflation. The PCE Price Index rose 0.2% (+1.4% y/y), up 0.2% ex-food & energy (1.6% y/y, vs. the Fed’s goal of 2%).

The Dallas Fed’s Trimmed Mean PCE Inflation Rate, which excludes the components with the largest price movements for the given month, rose 2.0% y/y.

Click here to enlarge

The Conference Board’s Consumer Confidence Index was little changed in the initial estimate for August (135.1, vs. 135.8 in July). Evaluations of the present situation rose to nearly a 19-year high, reflecting rosier job market perceptions. Expectations fell, reflecting reduced optimism about future business conditions. The report noted that “consumers have remained confident and are willing to spend.” However, increased tariffs and escalating trade tensions “could potentially dampen consumers’ optimism regarding the short-term economic outlook.”

The University of Michigan’s Consumer Sentiment Index fell to 89.9 in August, vs. 92.1 in the mid-month reading and 98.4 in July. The decline was “due to negative references to tariffs,” according to the report. Expectations fell from 90.5 to 79.9.

Durable Goods Orders jumped 2.1% in July, following a 1.8% gain in June, reflecting a further rebound in aircraft orders (civilian aircraft +47.8%, defense aircraft +34.4%). Ex-transportation, orders slipped 0.4%. Orders for nondefense capital goods ex-aircraft rose 0.4%, although June was revised to +0.9% (from +1.5%) and shipments for this category fell 0.7% (following no gain in June).

The Chicago Business Barometer rose to 50.4 in August, vs. 44.4 in July and 49.7 in June (50 is the breakeven level). New orders shifted back into expansion, but production remained muted (although better than in July).

The Chicago Fed National Activity Index fell to -0.36 in the initial estimate for July, vs. +0.03 in June and -010 in June. At -0.14, the three-month average, consistent with below-trend growth in the near term.

The Pending Home Sales Index fell 2.5% in July, following a 2.8% increase in June, down 0.3% y/y. Results were weaker across all four regions. The National Association of Realtors noted that “economic uncertainty is no doubt holding back some potential demand, but what is desperately needed is more supply of moderately priced homes.”

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© 2019 Raymond James Financial, Inc. All rights reserved.

© Raymond James

More Fixed Income Topics >