Weighing the Week Ahead: Is it Time to Worry about Crowded Trades?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe economic calendar is normal with an emphasis on the consumer. Both PPI and CPI data will be reported, but little change is expected. Central bank fans will have to make do with the ECB Thursday announcement. Democrats will have another debate on Thursday (now down to only ten on stage!) but it is too early to think about policy effects.

In the last two weeks the market rebound has included a change in tone. Thinking about this during my recent travels it seemed a bit like a puzzle. There are pieces of evidence that we have been monitoring for many months. A broader discussion has emerged in the financial media, leading pundits to wonder:

Is it time to worry about crowded trades?

Last Week Recap

In last week’s installment of WTWA, I discussed whether Presidential politics might change the course of economic policy. Usually it is the other way around, but economic success is crucial to the Trump campaign. With trade policy now subtracting a full percentage point from GDP, a deal would improve the economic case. By the end of the week there was some speculation about the political impact of the jobs report, but I have yet to see anyone drawing inferences about possible policy changes. Stay tuned.

The Story in One Chart

I always start my personal review of the week by looking at a great chart. This week I am featuring Jill Mislinski’s version, which combines a lot of information in one picture. The full article also includes several other interesting takes on price movement.

The market gained 1.8% for the week with significant opening gaps for breaking news. The trading range was 3.3% for the week, but pretty small after Thursday’s gap opening. My weekly Quant Corner translates this into a volatility calculation which you can compare both to VIX and to past readings. Among the many other helpful charts in Jill’s post is this perspective on drawdowns.

News You Can Use

Dr. Brett Steenbarger’s new book is now available! Radical Renewal: Tools for Leading a Meaningful Life is innovative in both form and content. While he emphasizes traders, his work has implications for everyone. The format makes it especially user-friendly. When I finish reading, I’ll do a more complete review, but what I have seen so far is great.

You have a chance to help research on an important issue and possibly win a cash prize. Just by joining in a fifteen-minute survey you can help determine the value of things that are not easily priced in the market – parks, free speech, and police protection for example.

Act quickly since the deadline to participate is Monday, September 9. Just go to https://www.hoover.org/KaneStudy and answer the 50 questions.

Noteworthy

The Visual Capitalist has a stunning depiction of global regime changes, illustrating the growth of democracy.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

New Deal Democrat’s high frequency indicators are an important part of our regular research. The results remain positive in all three of the time frames, although the short term remains volatile.

The Good

- Factory orders for July grew 1.4%, beating expectations of 1.0% and June’s 0.5%.

- Framing lumber prices are down 20% year-over-year. This is good news for home builders, my current favorite group. (Calculated Risk).

- ISM Non-Manufacturing for August improved to 56.4 from July’s 53.7. Expectations were only 54.0.

- ADP private employment for August grew 195K versus expectations of only 150K and July’s (downwardly revised from 156K) 142K.

- The Beige Book described continued modest economic expansion. There is some labor market tightness and some reported effects from slowing global demand and trade tensions. Home sales remain constrained due to low inventories. (Calculated Risk).

The Bad

-

Construction spending rebounded from the June decline (upwardly revised from 1.3% to 0.7%) but failed to meet expectations of a 0.3% gain. This is another case where considering the revision along with the new data makes sense.

-

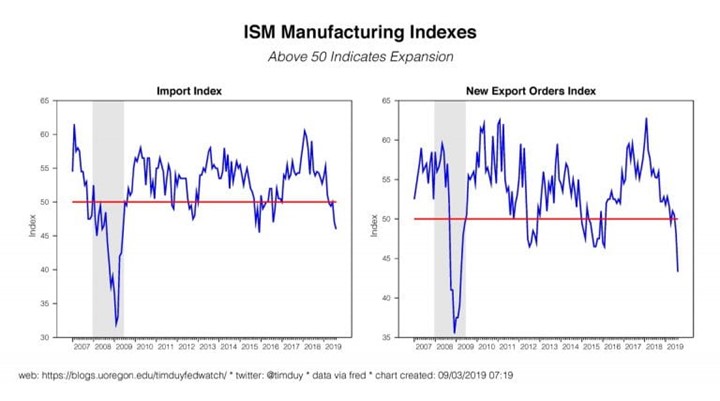

ISM Manufacturing for August registered 49.1. This missed expectations of 51.3 and was a decrease from July’s 51.2.

-

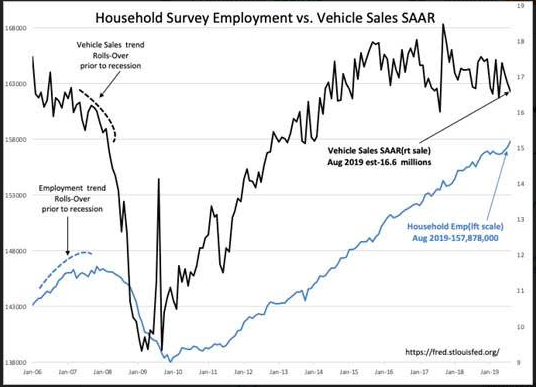

Non-farm payrolls for August showed net growth of only 130K versus expectations of 171K. Prior months were also revised lower. I scored this as “bad” because the popular perception described it as a big miss. There was little market effect, and no one mentioned the 120K margin of error on results. “Davidson” (via Todd Sullivan) took note of strength in the Household survey numbers which he finds to be related to other key indicators.

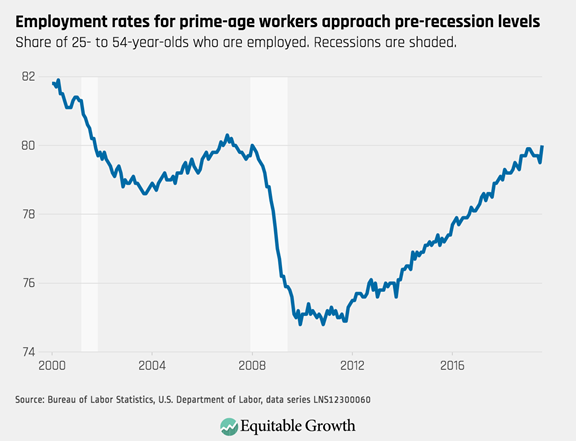

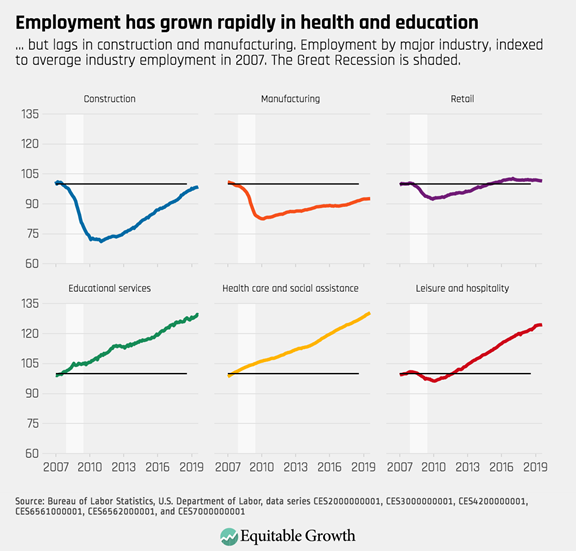

A bright spot was labor participation, but growth remains weak in manufacturing.

The Ugly

Dorian, the latest storm to leave a trail of death and destruction.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

The Calendar

After last week’s avalanche of economic data, the calendar has returned to normal. Retail sales is probably most important, given the current importance of consumers. JOLTS will provide evidence about labor market structure (but not job growth as many seem to think). Inflation is expected to remain tame in both the PPI and CPI versions. Business investment and small business activity have become more important, so I’ll be watching the NFIB Index. Michigan sentiment is also interesting, especially in a world filled with worries.

The ECB will announce its interest rate decision on Thursday, but we don’t have any FedSpeak. The Democrats will make up for it with another debate on Thursday evening.

Briefing.com has a good U.S. economic calendar for the week. Here are the main U.S. releases.

Next Week’s Theme

There has been a change in the tone of the economic discussion over the last two weeks. Some widespread beliefs are getting more of a challenge. Surprising to many markets have rebounded even though the underlying data has not really changed. Behind some of this thinking is a growing concern which has some pundits asking:

Is it time to worry about the crowded trades?

Background

Some analysts overuse the term “bubble.” I find it to be imprecise and subjective. Often, we identify bubbles only in retrospect. We can more readily spot “crowded trades.” These are characterized by massive and continuing inflows of buyers, pushing valuations well beyond normal levels. There is often a popular argument that seems compelling.

Most of the current crowded trades are the result of post-2008 fear, exacerbated by those more interested in ratings and commissions than sound analysis. Here are some candidates:

- Cash.

- Bonds.

- Products designed for high-yield – BDCs, MLPs, REITs.

- Structured products with complex payoff calculations.

- Annuities.

These share perceived safety with a stated return. Often the emphasis is on a stream of payments without much attention to underlying risk. In the case of non-traded REITs and BDCs the buyer may not even know what the asset is worth.

Adding to this list – The Big Short’s Michael Burry Sees a Bubble in Passive Investing. The push into passive investing has skewed valuations, with more opportunities in small caps. Here is some support.

In today’s post I am interested in identifying strongly held market perceptions, possible crowded trades, and the emerging recognition. Once we have the facts, we can think about how to use this to our investment advantage. I will include brief takes on a variety of relevant topics, emphasizing some key charts. I am thinking out loud, and I hope you enjoy the process of considering this evidence.

The Fed

The market continues to react as if it is all about the Fed. This fits a popular meme that stock market gains since the great recession have nothing to do with the economy and corporate earnings, but only the intervention of central banks.

Jim Bianco provides this useful summary via The Daily Shot.

Meanwhile, the Fed has been more optimistic about overall economic strength and less concerned about the chances of a recession. Tim Duy expects a 25bp rate reduction this month, mostly as insurance. And President Trump encourages this viewpoint, attempting to lay all economic issues at the doorstep of the Fed.

Many people do not realize the significance of an independent Fed. In an objective and apolitical fashion, Prof. Marty Finkler in Low Interest Rates: The Addictive Policy Drug of Choice, reviews the drawbacks to sustained periods of low interest rates. [Jeff – And this is what we would see without Fed independence]. He draws upon work by the influential former Australian banker, Satyajit Das, to identify and discuss the negative side effects. Some will be familiar to readers, but the entire post is worth reading.

The Trade War

From the outset I have described this as a real-time economics lesson for those who did not take the class. The lesson is becoming clear.

- The market recognizes and reacts to actual hikes.

- Manufacturing is showing the effects.

- In addition to the first-order effects, the controversy creates a climate of uncertainty.

- This is starting to affect corporate earnings.

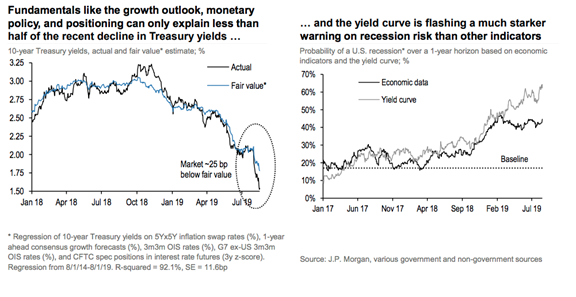

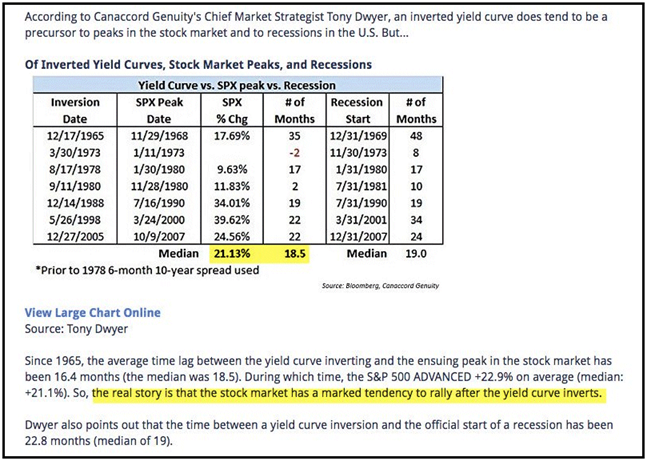

Recession Concerns

The knee-jerk reaction to the inverted yield curve has abated. Most now realize that the signal is not an instant indicator. It is about probability, not certainty.

The decline in the ten-year note is not all about economic weakness, especially in the US.

Markets frequently respond positively in the immediate aftermath.

Investment ideas

This will be an ongoing project, but the evidence for the housing sector continues to build. It is unpopular, so it is hiding in plain sight.

Despite recent strength, pundit criticism keeps the P/E ratios low. There is strong demographic support for this group.

But that is just an example. Seeking out the sectors in line to benefit from crowded trade exits will take plenty of work.

I’ll have my own observations in today’s Final Thought.

Quant Corner and Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update, featuring the Indicator Snapshot.

Short-term technicals have stabilized but remain bearish. Long-term technicals have also stabilized at neutral. Recession risk is still in the “watchful” area with the odds up a notch. We are seeing little confirmation for the risk signals, which we have been monitoring since May.

Considering all factors, my overall outlook for investors remains bullish.

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score”.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

RecessionAlert: Strong quantitative indicators for both economic and market analysis

Georg Vrba: Business cycle indicator and market timing tools. The most recent update of Georg’s business cycle index does not signal recession nor does his unemployment method.

Doug Short and Jill Mislinski: Regular updating of an array of indicators. Great charts and analysis. It is time for an update of their famous Big Four chart.

Recessions are defined as the period between a business cycle peak and a trough. The NBER looks for a substantial decline from a peak, especially in these four indicators. Only industrial production has made a peak, and there has been a small rebound.

Guest Sources

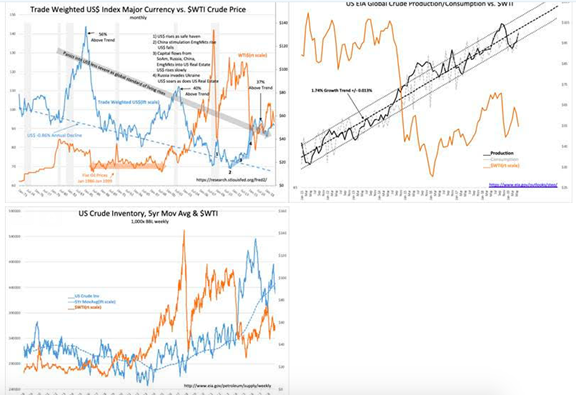

“Davidson” (via Todd Sullivan) describes the factors behind oil trading and the impact on overall market psychology.

Highlights: US Crude Inventories 25.7mil BBL below 5yr mov avg. Tied to algorithms and believed to be a sign of economic strength/weakness, current trend suggest a marked shift to positive market psychology. Economic strength has continued on trend since 2009 with the past 20mos of pessimism unjustified.

And elaborating….

The past 24mos (beginning Oct 2018) has seen a dramatic rise of investor pessimism well out of sync with underlying economics. This has been due to algorithms reliance on certain measures which in turn has exacerbated other measures. It began with capital shifting to the US$ which drove 10yr Treasury rates low enough to invert the yield curve, a major signal for algorithms. Algorithms then sold oil prices lower to offset expected recession related declines in equities. The belief that oil Supply/Demand swings wildly during economic ebbs and flows is what drives oil prices-

The volatility in oil prices is not related to Supply/Demand which has grown consistently with the ten-year trend, a rate of about 1.74%. His conclusion is that a rapid change in psychology is possible because of inventory reductions. This is an important analysis, worth reading carefully.

Timothy Taylor, drawing upon a McKinsey Global Institute Study, explains how China and India have developed domestic supply chains. This change is relevant when evaluating the US leverage in the trade war with China. From the study: “As consumption rises, more of what gets made in these countries is now sold locally instead of being exported to the West. Over the decade from 2007 to 2017, China almost tripled its production of labor-intensive goods, from US$3.1 trillion to US$8.8 trillion. At the same time, the share of gross output China exports has dramatically decreased, from 15.5 percent to 8.3 percent.”

Insight for Traders

Our weekly “Stock Exchange” series is written for traders. I try to separate this from the regular investor advice in WTWA. There is often something interesting for investors, but keep in mind that the trades described are certainly not suitable for everyone.

This week’s edition discusses volatility, which provides both challenges and opportunities for traders. We combine expert advice with a discussion of how our trading models handle volatility. As always we share some picks including ideas from our new member, Emerald Bay. Pulling it all together and providing counterpoint drawn from fundamental analysis is our regular series editor, Blue Harbinger.

Insight for Investors

Investors should understand and embrace volatility. They should join my delight in a well-documented list of worries. As the worries are addressed or even resolved, the investor who looks beyond the obvious can collect handsomely.

Best of the Week

If I had to recommend a single, must-read article for this week, it would be Chuck Carnevale’s Time in the Market and Value Investing is Not Market Timing. He explains the importance of thinking long term and why using valuation reduces your risk:

The reason the risk is lower is because a company that is trading at fair value or undervalued levels is less likely to fall as much in a bad market as an overvalued company. Moreover, in the long run a company’s stock price will align with fair value. Consequently, if fundamentals remain solid, it is virtually an inevitability that stock price will recover and most likely advance to new highs. However, this is not market timing because it is not an attempt to forecast short-term price movements.

He explains why most people cannot stick with this program:

…there are those that simply cannot or will not embrace or accept the notion of long term. However, to be fair, there is a reason why many investors cannot embrace or maintain the patience to trust that fair valuation will inevitably manifest. Unfortunately, most investors are quick to judge their holdings over a time frame that is too short. Therefore, in his 1996 Berkshire Hathaway annual report, Warren Buffett provided this sage advice: “If you aren’t willing to own a stock for 10 years, don’t even think about owning it for 10 minutes.”

Nevertheless, the real problem is that although the reversion to the mean, as statisticians would call it, is virtually an inevitability, the time it takes the reversion to occur is not precise. Once again, Warren Buffett explains it quite succinctly with the following quote: “The fact that people will be full of greed, fear or folly is predictable. The sequence is not predictable.”

He then provides several examples of well-known stocks that he highlighted in past articles. As you consider them, ask yourself whether you would have the patience and commitment to your method to ride out the stretch of “underperformance.” Some readers will be surprised by the examples.

Stock Ideas

Blue Harbinger likes Saratoga Investment Corp. (SAR), describing in detail both the strengths and the risk factors. This is a good article for anyone considering a BDC investment since you will learn what to look for.

Want a growth sector? How about Robots? Barron’s reviews the most appealing sectors as well as some specific names.

Peter F. Way draws upon the actions of “experienced investment professionals who may be better informed than you” to explain why he likes Adobe, Inc. (ADBE) for a near-term capital gain.

It is time for another update of the Rose Portfolio. The results are good, and the process is transparent. It is loaded with ideas.

Ray Merola likes the value proposition at CVS Health (CVS). Investors will learn from his helpful list of the questions guiding his analysis.

Personal Finance

Abnormal Returns is the go-to source for anyone serious about the investment business. The Wednesday edition has a special focus on personal finance, with plenty of ideas for the individual investor. As always there are many good links. My favorite this week is Tony Isola’s retirement advice, Get Busy Living, Or Get Busy Dying.

Yes, it is of special interest for Mrs. OldProf and me, and a good description of the choices everyone faces. It starts long before retirement.

There’s a huge difference between meaningful work and having a job.

Who knew? Working might be the best part of your retirement

Since I enjoy much of my work, continuing to write, analyze the market, and manage portfolios meets the criteria. I’ll also have more time to try some new things. I have a list!

Watch out for…

Treasury Bonds Are Now Riskier Than Stocks, writes Andrew Bary in Barron’s. The 30-year Treasury is now yielding about 2%, near the record low. An increase in yield to 3% implies a 20% decrease in the bond price. Most investors do not know this math, and therefore underestimate their risk.

Smaller shale drillers, now at a greater risk of bankruptcy (WSJ).

Final Thought

Investors are an impatient lot. Even when they do not plan to sell assets in the near future, they want the comfort of Mr. Market’s continuing endorsement of their current holdings. This natural human tendency is the basis for many decisions and the cause of poor investment results.

Background

Effective strategies– supported by logic, analysis, data, and the best methods – often seem to have lost their value. Even long-term evidence is discounted because “things are different now.”

- In 2000 there was a “new paradigm” which meant that getting a share of Internet eyeballs was as good as earnings. Ratios of 100 times sales were routine. Anyone could succeed in the market by throwing a dart at the technology listings. (That wouldn’t work anymore without damaging your screen, of course). Advisors who talked about gains of 15-20% a year drew laughs. Investors could do that in a week or two via an Internet IPO. The madness continued for years, crushing anyone in the way. And then it ended.

- In 2008 the heroes of the Big Short analyzed the flaw in the synthetic mortgage market. The big banks and ratings agencies profited from creating “AAA paper” that helped to satisfy worldwide demand for safety and yield. It is popular to say that everyone was too stupid to see what was happening. In fact, most economists focused on the total size of the subprime market with no knowledge of the market in synthetics. Since the latter was six times as large, the problem was much bigger than anyone understood. Except of course, Michael Burry and a few others. We remember that he was a hero and featured in a major motion picture. We forget the years that passed while he lost investors, paying regular premiums for an eventual big winner. Investors want smooth and regular gains.

- Now? The newest claim that things are different suggests that volatility undermines value investing. So much for decades of evidence on that subject! The claim is that bonds are safe, and stocks are risky, without regard to the comparative prices.

Will This Go on Forever?

Of course not, but the exact end of the current regime is elusive. It would have happened by now save for the launch and expansion of the trade war. Few guessed the market top in 2000 or 2008 either. Can we do any better?

I am watching the following:

- News on the trade war effects, both in the US and globally.

- Hints of policy softening from China.

- Signs of pressure on the Trump Administration from contributors, party leaders and economic news.

- Changes in the Administration lineup. It is possible to get the economic bounce from improved trade while continuing the negotiations on intellectual property.

- An increase in long-term interest rates. Investors in bonds and bond substitutes have grown accustomed to yield and capital appreciation. An account statement showing losses will be a surprise. Savvy traders will be first to the exits, but these are crowded trades.

What Can Investors Do?

- For starters, investors should not join the chase into bonds and bond substitutes. If you have large positions in these sectors, do a careful evaluation of your portfolio risk.

- Recognize that anything with high yield probably carries a higher level of risk, but it might not be obvious. If you are not sure of the risks of an investment, do not just believe a salesperson. Seek independent, objective advice from a fiduciary.

- Build positions in the under-valued sectors which will get the fund flows. Opinions vary on the best sector and stock choices. That is the subject of my current work.

- Channel your inner Michael Burry by using a little leverage in the cheap sectors. There are some attractive low-risk option strategies.

The biggest decisions are often the most challenging. This is such a time.

Some other items on my radar

I’m more worried about:

- Iran confrontations and the chance for an accident.

- Hong Kong protests and a possible reaction. This is an example of an unpredictable event with unknown financial impact and no good way to hedge.

I’m less worried about

- Technical market reactions. Our indicators have stabilized a bit and it would not take much to generate some breakouts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits