As expected, the Fed lowered short-term interest rates and officials remained divided about what to do next. The policy meeting came in a week that saw elevated funding pressures in money markets, which drove the effective federal funds rate above the top of the target range. On Friday, the New York Fed announced a series of overnight and term repurchase agreement (repo) operations to October 10, which should take care of things. However, the developments highlighted concerns about whether the Fed will need to embark, earlier than anticipated, on “organic” quantitative easing to ensure that there is an adequate amount of reserves in the system.

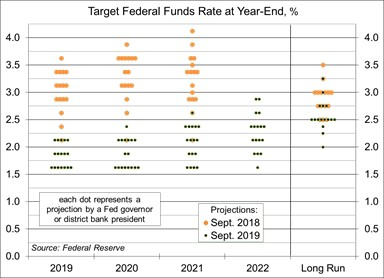

It is well known that Fed officials have been divided on the appropriate stance of monetary policy. In June, when the Fed left rates steady, officials fell evenly into two camps, those expecting no change in rates through the end of the year and those anticipating a half-point cut. The minutes from July 30-31 policy meeting, when the Fed cut by 25 basis point, showed that “several” officials favored leaving rates unchanged. At the September 17-18 meeting, two of the ten voting officials dissented in favor of no change, while one dissented in favor of a 50-bp cut. The revised dot plot (the forecasts of the appropriate year end federal funds target rate made by each of 17 senior Fed officials, not all of whom vote on policy) showed a three way split in the outlook through the end of the year. Five officials presumably did not want a cut at the September meeting, five officials anticipate no further rate cuts this year, and seven expect another 25-bp cut.

Click here to enlarge

It is also well known that officials are divided on the benefits of the dot plot. Some note the tendency of market participants to misinterpret the results as signaling a committed policy path. Others, including Chair Powell, believe it to be an important communications tool, but one that needs to be explained better. It’s useful to look at where the Fed has come over time. A year ago, when the federal funds target range was 2.00-2.50%, officials expected further rate increases. That was the case in December as well, when the target range was raised to 2.25-2.50%. The dots shifted toward neutral in March, down further in June. The dots merely reflect an assessment of where the economy is headed, and that will change.

This year, the household sector fundamentals have remained solid. Consumer spending, which account for 68% of Gross Domestic Product, should continue to propel the overall economy. In contrast, slower global growth and trade policy uncertainty have weighed against business fixed investment. Moreover, the impact of trade tensions on the economy are being felt increasingly. Businesses report that they can’t get price quotes for next year’s supplies. Fearing the tariffs on consumer goods set for December 15, some are stockpiling goods and materials in advance. Many doubt that they will be able to pass higher costs along. In his post-FOMC press conference, Chair Powell noted that “our business contacts around the country have been telling us that uncertainty about trade policy has discouraged them from investing in their businesses.”

While a complete trade agreement with China appears increasingly unlikely, there are prospects for a mini deal, which would halt a further escalation in trade tensions, perhaps even de-escalating a little (a small reduction in existing tariffs). That ought to be encouraging for the financial markets, although it’s difficult to say how much may be already factored in.

Still, the Fed will have a hard time in trying to gauge the impact of trade policy uncertainty as it looks to 2020. Powell noted that the latest cut was meant to offset the impact of slower global growth and trade policy uncertainty, to guard against the downside risks these factors posed, and to help push inflation toward the Fed’s 2% goal. These were the same reasons given for the cut in July.

Meanwhile, upward pressures in funding markets emerged last week. It was known well in advance that there would be a greater demand for funds related to corporate tax payments and Treasury auction settlements. However, demand was stronger than anticipated, and the Fed conducted overnight repurchase operations (repos) on Tuesday and Wednesday, to counter the pressure. There is some question as to why banks with excess cash failed to lend to the overnight money market.

The Fed had last intervened in the repo market during the financial crisis. When the Fed shifted to a target range for the federal funds rate, the Interest on Excess Reserves (IOER) was meant to define the top of the range and the overnight repo rate was meant to define the lower end of the range – and the Fed didn’t expect to intervene much to keep the federal funds rate within the range. The IOER has since been lowered from the top of the range (1.80% currently, 20 bps below the top of the range). The Fed ran some test trials in the repo market during the recovery, but eventually abandoned the idea of intervening on a regular basis. Last week’s surge in the (market) repo rate pushed the effective federal funds rate above the top of the target range. On Friday, the New York Fed announced a series of overnight and term repurchase agreement operations out to October 10, with the purpose of keeping the effective federal funds rate within the target range. That should take care of it.

The Fed downplayed the money market developments as being “technical” in nature. However, the issue added to concerns about whether the Fed will be able to deliver an adequate amount of reserve to the system. Reserves had fallen as the Fed reduced the size of its balance sheet. The unwinding of the balance sheet has ended, but the Fed had anticipated allowing it to grow “organically” in line with the overall economy (and the need for bank reserves) through quantitative easing (asset purchases) at some point in the future. In his press conference, Powell indicted mini QE could come sooner.

As Powell noted in his press conference “while these issues are important for market functioning and market participants, they have no implications for the economy or for the stance of monetary policy.”

Data Recap – As expected, the Federal Reserve cut interest rates even as officials remained divided. There were funding pressures in the money market, adding anxiety, but this appeared to be a temporary phenomenon and was addressed by the Fed. The attack on a Saudi oil production facility boosted oil prices, but did not have a broad impact on equities. The economic reports were positive, but financial market reaction to the data appeared limited.

Funding Pressures were elevated in the repo market, reflecting stronger-than-expected demand for short-term funds (related to tax payments and Treasury note auctions), pushing the effective federal funds rate above the top of its target range. At the end of the week, the New York Fed announced “a series of overnight and term repurchase agreement (repo) operations to help maintain the federal funds rate within the target range.”

The Federal Open Market Committee lowered the federal funds target range by 25 basis points, to 1.75-2.00%, “in light of the implications of global developments for the economic outlook as well as muted inflation pressures” (the same justification that it used in cutting rates in July). Kansas City Fed President Esther George and Boston Fed President Eric Rosengren dissented in favor of no change, while St. Louis Fed President James Bullard dissented in favor of a 50-bp cut. The FOMC lowered the Interest on Excess Reserves rate (IOER) to 1.8%, 20 bps below the top of the federal funds target range, and reduced the overnight repo rate by 30 bps, to 1.70%. The Fed’s Board of Governors approved a 25-bp cut in the primary credit rate (the discount rate) to 2.50%)

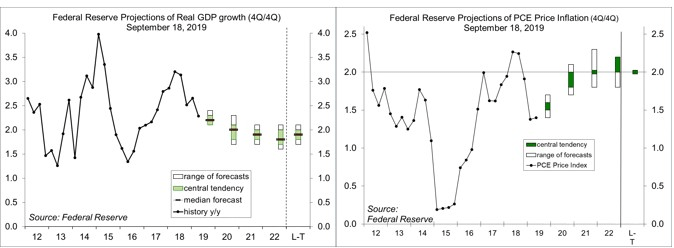

The Fed’s Summery of Economic Projections showed little difference from forecasts made in June. Officials generally expect GDP to grow 2.2% in 2019 (4Q/4Q) and 2.0% in 2020. The unemployment rate is expected to stay low (3.7% in 4Q19 and 4Q20). Inflation is expected to move toward the 2% goal next year. The dots in dot plot showed a three-way split, with five officials apparently wanting no change at the September meeting, five anticipating no further cuts following the September move, and seven looking for one more cut by year end.

Click here to enlarge

In his press conference, Fed Chair Powell said that the move was taken “to help keep the U.S. economy strong in the face of some notable developments and to provide insurance against ongoing risks.” Consumer spending, supported by solid fundamentals, “has been the key driver of growth.” However, “our business contacts around the country have been telling us that uncertainty about trade policy has discouraged them from investing in their businesses.” Asked whether this was still “a mid-cycle adjustment,” Powell demurred, noting that “if the economy does turn down, then a more extensive sequence of rate cuts could be appropriate.”

Industrial Production rose 0.6% in the initial estimate for August (+0.4% y/y). The output of utilities rose 0.6% (-0.7% y/y). Oil and gas well drilling fell 2.5% (-9.2% y/.y), while oil and gas extraction rose 2.2% (+8.4% y/y). Manufacturing output rose 0.5% (-0.4% y/y), up 0.6% (-0.5% y/y) ex-autos.

Building Permits jumped 7.7% (±1.2%) in August, to a 1.419 million seasonally adjusted annual rate (+12.0% y/y). Single-family permits rose 4.9% (+4.5% y/y), with gains concentrated in the South. Unadjusted single-family permits for June-August fell 2.9% y/y (+0.7% in the Northeast, -6.1% in the Midwest, -3.0% in the South, and -1.9% in the West). Housing Starts rose 12.3% (±11.6%), with single-family starts up 4.4% (±10.3%).

Homebuilder Sentiment edged up to 68 in September, vs. 67 in August (revised from 66). The National Association of Home Builders noted low mortgage rates and strong demand, but ongoing supply challenges (a shortage of lots and labor and increased uncertainty from trade policy).

Existing Home Sales rose 1.3% in August, to a 5.49 million seasonally adjusted annual rate (+0.6% y/y). Results varied by region. The National Association of Realtors attributed the increase to falling mortgage rates, but noted that a limited inventory of lower-priced homes for sale continued to constrain sales.

The Current Account Deficit narrowed to 127.8 billion (2.4% of GDP) in 2Q19, vs. $136.2 billion in 1Q19 (2.6% of GDP). The deficit in goods and services widened, but the balance on income rose more.

The Index of Leading Economic Indicators was unchanged in the initial estimate for August. Positive contributions were led by building permits, credit conditions, and the factory workweek. Negative contributions were led by ISM New Orders, stock prices, jobless claims, and the yield curve.

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.

© Raymond James

© Raymond James

Read more commentaries by Raymond James